The United States began a military blockade of Iran's ports on , targeting the roughly 1.7 million barrels per day of crude that Iran has kept flowing through the Strait of Hormuz during its war with the US and Israel. President Donald Trump ordered the blockade after a weekend round of peace talks in Islamabad failed to produce a deal, and the Pentagon's Central Command stated that six vessels were turned back during the first twenty-four hours of enforcement. Oil markets treated the news as close to a non-event, with Brent crude sliding back toward $93 a barrel before recovering to $95.75, and the S&P 500 approaching its late-January record. The complacency is the story. The economic math of the blockade says the risk is skewed to the downside, and the downside is bigger than the market is currently pricing.

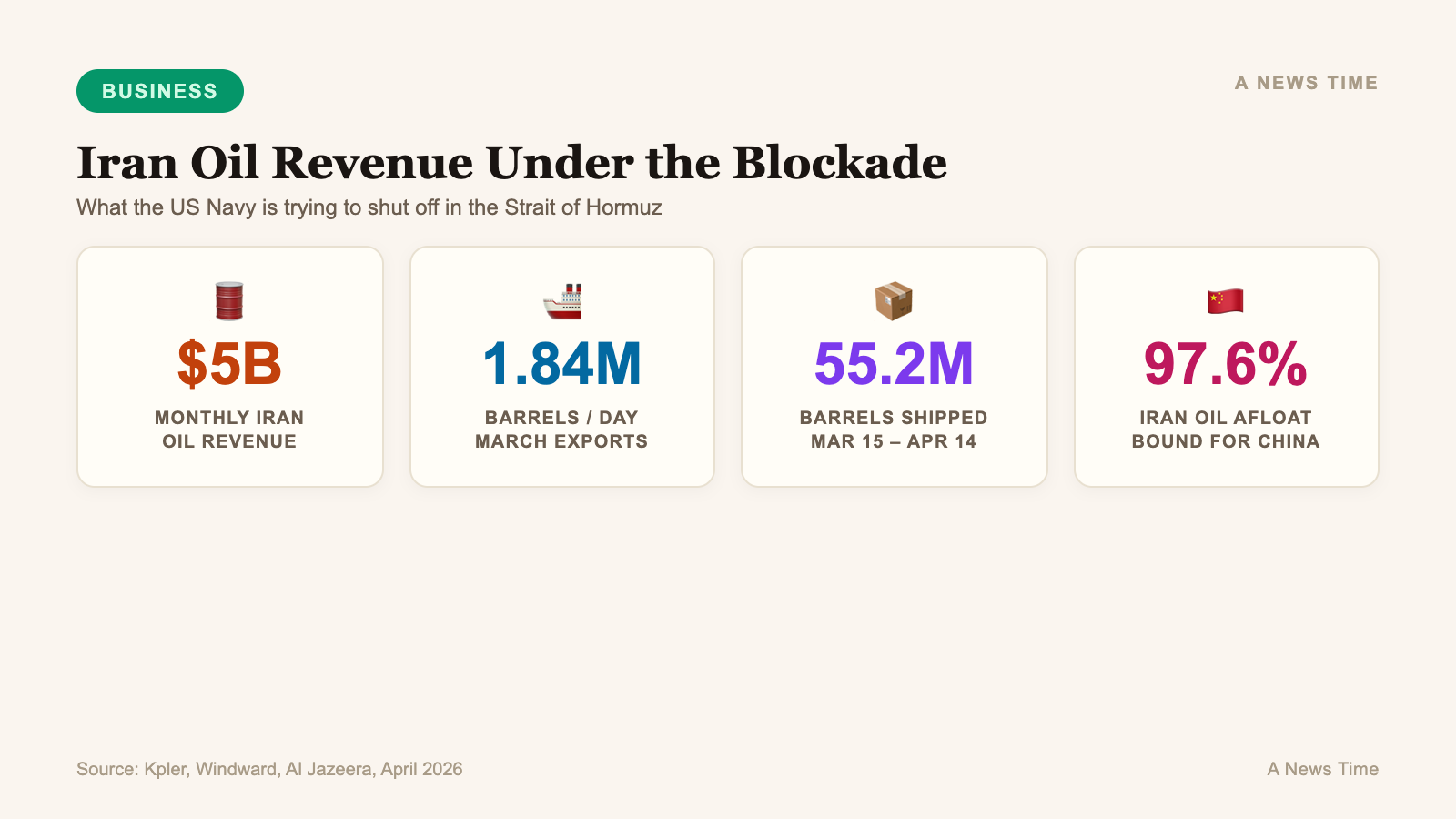

Iran has been the rare beneficiary of its own war on the global energy system. According to trade intelligence firm Kpler, Iran shipped 1.84 million barrels per day of crude in March and 1.71 million bpd so far in April, compared with a 2025 average of 1.68 million bpd. At a conservative $90 a barrel, that is roughly $4.97 billion in monthly oil revenue, a 40 percent increase over what Tehran was earning in the weeks before the war started on . The blockade is designed to take that revenue off the table. Whether it can is a different question.

Iran's oil revenue at risk

The numbers on what the blockade is actually targeting are the clearest part of this story. From to , Iran exported 55.22 million barrels of crude through the strait, according to Kpler data cited by Al Jazeera. Tehran's three main grades, Iranian light, Iranian heavy, and Forozan blend, did not fall below $90 a barrel over the past month and repeatedly traded above $100. For Iran's budget, that is the difference between wartime austerity and wartime solvency.

The maritime intelligence firm Windward estimated that as of , total Iranian oil afloat on tankers stood at 157.7 million barrels, and 97.6 percent of it was destined for China. All of that volume is now theoretically exposed to the blockade. Frederic Schneider, a nonresident senior fellow at the Middle East Council on Global Affairs, told Al Jazeera that Iran carries a buffer of roughly 127 million barrels in floating storage as of February, which provides a cushion but not an escape. The toll revenue that Iran has been collecting from non-Iranian vessels negotiating individual passage deals is also at risk.

| Metric | Pre-war (Feb 2026) | War period (Mar-Apr 2026) | Post-blockade target |

|---|---|---|---|

| Daily crude exports (bpd) | ~1.68 million | 1.71 to 1.84 million | Near zero (US target) |

| Average price per barrel | Under $70 | $90 to $100+ | N/A |

| Estimated monthly revenue | ~$3.45 billion | ~$4.97 billion | N/A |

| Brent benchmark | $72 | $93 to $102 | $82 (IMF reference) |

A complete shutdown of Iranian crude exports would strip roughly $60 billion off an annualized revenue run rate. For an economy already under layered sanctions and fighting a war, that is a forcing function. It is also the reason Iran has a strong incentive to escalate rather than concede, because the alternative is watching its fiscal position collapse.

Why oil markets are not panicking

The market reaction on was a study in compartmentalization. Brent traded at $95.75 by the afternoon, having dipped as low as $93.93 after President Trump told Fox News the war was close to ending. The S&P 500 closed in on its record from late January. US Treasury yields held near 4.25 percent on the 10-year. The IEA said in its April Oil Market Report that global oil demand would contract by 80,000 barrels per day in 2026, reversing an earlier forecast of a 640,000 bpd increase, and called the strait closure "the largest disruption in history." Prices barely moved.

Three things explain the quiet. The first is that the blockade's operational footprint on day one was narrow. Reuters, citing LSEG and Kpler data, reported that at least eight ships including three Iran-linked tankers crossed the strait on the first full day. A US-sanctioned Chinese tanker, Rich Starry, loaded with methanol out of the UAE's Hamriyah port, became the first to clear the strait since the blockade began. US Central Command confirmed it had issued warnings to six vessels that complied and turned back, which is nowhere near a complete enforcement picture.

The second is that traders are pricing peace talk optionality. Trump said on Tuesday that US-Iran negotiations could resume within two days in Pakistan. The New York Times reported that Washington and Tehran had traded proposals on suspending Iran's nuclear program, with Iran offering five years against a US request for twenty. The market is treating the blockade as leverage in a negotiation rather than the opening act of a larger escalation.

The third is that US equity markets specifically have absorbed the war-risk premium. As Reuters put it in a Tuesday analysis, higher oil prices, higher yields, and no more Fed rate cuts have become the baseline, and equity investors have stopped treating any of those conditions as disqualifying. Anna Wu, cross asset strategist at Van Eck Associates Corp., told Bloomberg the rally's sustainability still needs testing given the volatility of peace talks. That is the polite framing. The blunt one is that the market is taking the Pentagon's implicit confidence at face value.

The retaliation channel

The bigger risk is not whether Iran's oil gets out. It is what Iran does to everyone else's oil trying to get out. The strait carries roughly 20 percent of the world's oil and gas supplies in normal conditions, and Iran has already demonstrated during this war that it can throttle traffic at will. A wounded, cash-starved Tehran has more incentive to disrupt tanker flows broadly than it did when it was earning $5 billion a month threading its own ships through a half-shut waterway.

The first-round retaliation options are familiar. Mining the strait, targeting Gulf terminal infrastructure, striking tankers flagged to US-aligned states, and using proxy forces in Iraq or Yemen to hit refineries and pipelines are all on the menu. The IEA in its April report flagged that physical crude prices in spot markets reached as high as $150 a barrel in early April as buyers scrambled for replacement supply. That is the pricing environment a serious retaliation would slot into, not today's $96 Brent.

"Iran has some buffer in the form of crude oil reserves in floating tanks, basically parked tankers, which was estimated at about 127 million barrels in February. But that doesn't mean that the blockade wouldn't hurt Iran. It's very difficult to say how serious the US is about this blockade, how long it will last, how it will end and what is coming next."

Frederic Schneider, Middle East Council on Global Affairs

The second-round option is China. Chinese Defense Minister Dong Jun issued a statement on saying Beijing has trade and energy agreements with Iran and expects those to be honored. "The Strait of Hormuz is open to us," Dong said, in language quoted by Democracy Now and widely recirculated in Chinese state media. China's Foreign Ministry separately called the blockade "dangerous and irresponsible." Treasury Secretary Scott Bessent, speaking at the IMF spring meetings on Tuesday, accused Beijing of "hoarding oil supplies and limiting exports of certain goods" during the war and called China an "unreliable partner," while also emphasizing that he wanted to preserve stability in the relationship ahead of a planned Trump visit to Beijing at the end of April.

The question is whether the US Navy is willing to stop a Chinese-flagged or Chinese-owned tanker that Beijing has explicitly warned it is prepared to defend. Schneider's framing to Al Jazeera was direct: "Most of the Iranian tankers are headed for China, and I cannot see China giving in to this blockade. Secondly, I don't see the US Navy seizing or even sinking these ships." If the blockade leaks on the Chinese end, Iran's revenue damage is smaller than Washington is hoping, and the political cost of enforcement rises sharply.

What it means for US gas prices and the Fed

The downstream effects of a sustained blockade, even a leaky one, run through three channels into the US economy. The first is retail gasoline. US pump prices were already rising on the back of the strait closure, and the Trump administration suspended the Jones Act earlier in April to allow foreign-flagged tankers to move refined product between US ports. A retaliation-driven spike back toward $120 Brent would push national average gasoline toward levels the Energy Information Administration has historically associated with measurable consumer spending retrenchment.

The second channel is inflation expectations. The IMF's World Economic Outlook, released on , cut the 2026 global growth forecast to 3.1 percent from 3.3 percent in January. IMF chief economist Pierre-Olivier Gourinchas told Reuters that the world is drifting between the fund's reference scenario and its adverse scenario, which forecasts 2.5 percent growth if oil averages $100 this year. For a detailed breakdown of how the Iran war is feeding into the global growth picture, see our coverage of the OECD's war-driven growth downgrade and the Fed's compressed policy options.

The third channel is the Federal Reserve's reaction function. The Fed has been operating under a baseline assumption that energy-driven inflation is transitory and should be looked through. Gourinchas warned on Tuesday that "stepping on the brakes will be painful" in an environment where inflation expectations become unanchored, and said much stronger monetary tightening may be needed than was required after the 2022 Russia-Ukraine oil shock because today's economy has more slack. That is an unusually direct warning from the IMF's chief economist. It lines up with the growing market-implied probability of a Fed rate hike rather than a cut, which we covered in our piece on the 52 percent hike odds driven by oil inflation.

The complacency trade

The shape of the risk is asymmetric, and that asymmetry is what the market is mispricing. If the blockade succeeds cleanly, oil trends back toward the IMF's $82 reference-case barrel and global growth holds near 3.1 percent. If the blockade leaks through Chinese carriers and ghost tankers but does not escalate, oil stays in the $90 to $100 range, Iran's revenue damage is smaller than planned, and the US gains less leverage than it wanted, which weakens the case for pressing further. If the blockade provokes meaningful Iranian retaliation against Gulf infrastructure or third-country tankers, oil spikes above $120 and the Fed's decision tree collapses into choices no central banker wants to make. The first outcome is the priced scenario. The other two are not.

Ship broker BRS told Reuters that "a return to normality in the Middle East arguably now appears more distant than it did one week ago," and that commercial traffic in the strait is likely to remain minimal for the foreseeable future. War-risk insurance premiums, reviewed by underwriters every 48 hours, have held at hundreds of thousands of dollars in additional weekly costs per voyage, reflecting an industry that is not yet comfortable calling this a contained situation. When war-risk underwriters and equity markets disagree, the historical record favors the underwriters.

The next data points worth watching are whether a second round of Islamabad peace talks materializes before the end of the week, whether Chinese carriers continue to transit the strait unchallenged, whether the IEA's "demand destruction" forecast starts showing up in real consumption data out of Asia, and whether the Federal Reserve's next communication shifts its framing of energy-driven inflation from transitory to persistent. Any one of those is capable of repricing the blockade story. All four at once would reprice a lot more than that.

Frequently Asked Questions

How much oil revenue does the US blockade aim to cut off?

Iran earned roughly $5 billion from oil exports in the 30 days leading up to the blockade, based on 55.22 million barrels shipped at prices between $90 and $100 per barrel. A complete shutdown would strip about $60 billion from Iran's annualized oil revenue, though leakage through sanctioned and Chinese-linked tankers is already evident on day two.

Why did oil prices fall on the first day of the blockade?

Brent crude dropped to as low as $93.93 a barrel before recovering to $95.75 after President Trump said on Fox News that the war was close to ending, and after reports that US-Iran peace talks could resume within days. Traders are pricing the blockade as leverage in a negotiation rather than a sustained military escalation.

What did China say about the Hormuz blockade?

Chinese Defense Minister Dong Jun said on April 13 that China has trade and energy agreements with Iran and stated, "The Strait of Hormuz is open to us." China's Foreign Ministry called the blockade "dangerous and irresponsible," and at least one US-sanctioned Chinese-owned tanker transited the strait in the first 24 hours of enforcement.

How is this affecting the Federal Reserve's rate path?

The IMF's chief economist warned on April 14 that the global economy is drifting toward an adverse scenario where oil averages $100 in 2026, which would require more aggressive monetary tightening than the 2022 oil shock did. Market-implied odds of a Fed rate hike rather than a cut have been rising alongside oil prices.

What is the IMF's reference forecast for oil and global growth?

The IMF's April 2026 World Economic Outlook assumes a short-lived conflict with oil averaging $82 per barrel in 2026 and global growth of 3.1 percent. Its adverse scenario assumes $100 oil and 2.5 percent growth, and its severe scenario slashes growth to 2.0 percent, which the fund called "a close call for a global recession."

Sources

- How much will US Hormuz blockade hurt Iran, and does Tehran have an escape? - Al Jazeera

- Strait of Hormuz traffic barely affected on first day of US blockade, data shows - Reuters

- "The Strait of Hormuz Is Open to Us": China Warns U.S. Against Blockading Iranian Ports - Democracy Now!

- IMF downgrades global growth outlook as Iran war hits prices - Reuters