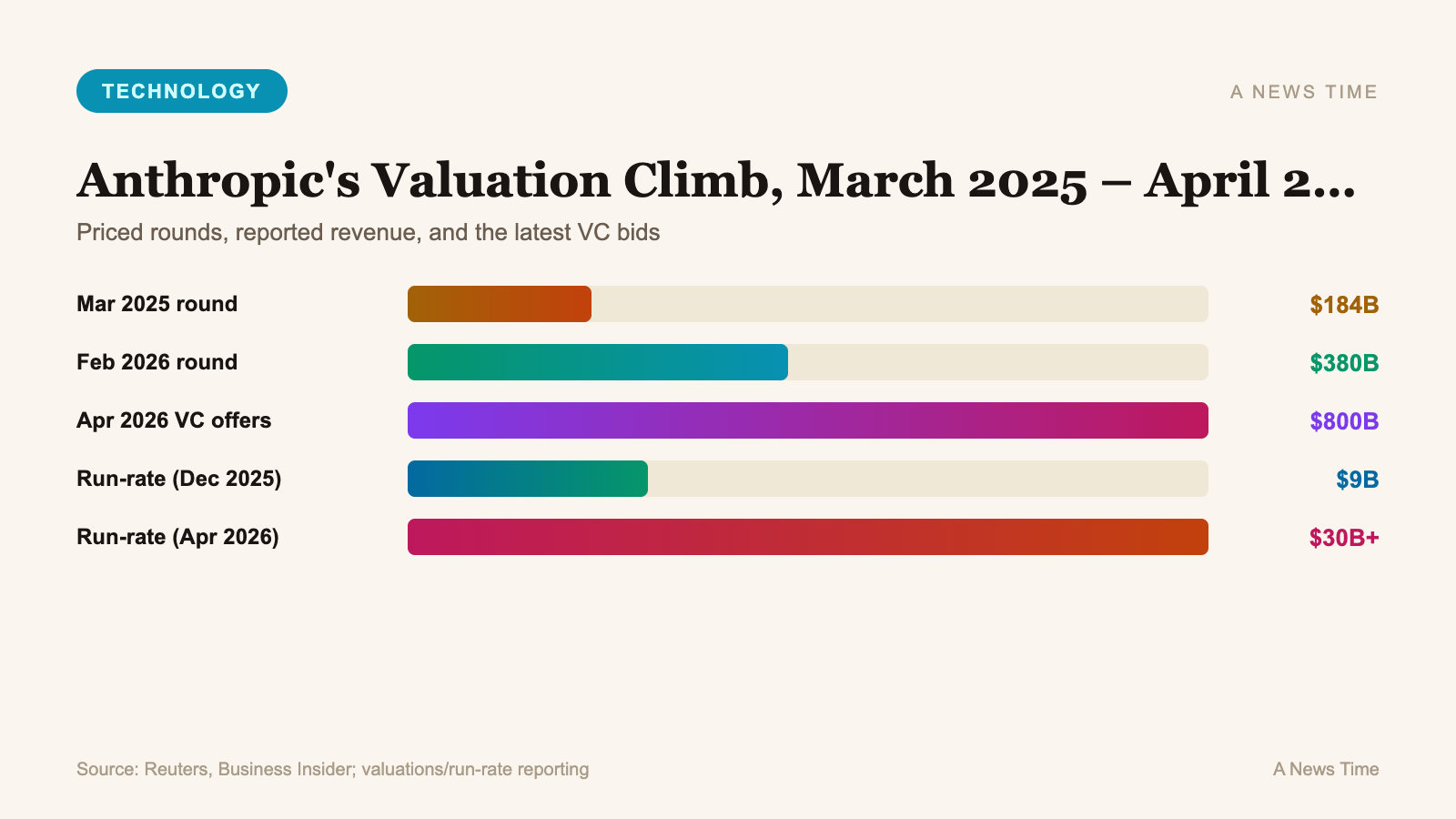

Venture capital firms have approached Anthropic in recent weeks with new investment offers that value the Claude maker at as much as $800 billion, more than double the $380 billion price tag set in its February funding round, Business Insider reported on , citing sources familiar with the conversations. Reuters confirmed the report the same day in a dispatch from reporter Anusha Shah in Bengaluru, and a separate Bloomberg News story added that Anthropic has so far resisted the overtures and is not actively running a new round.

The numbers, if they hold up through a future priced round, would mark one of the sharpest upward revaluations in private technology history. They also land in the middle of a week when the artificial intelligence funding cycle is being openly questioned, and when Anthropic itself is publicly floating a possible initial public offering that would move it out of the private markets for good.

What the $800 billion figure actually represents

The number is not a closed deal. It is the top of a range of informal offers Anthropic has received from venture firms hoping to buy into a new priced round before the company files for an IPO. There is no term sheet, no confirmed lead, and no disclosure about which firms are at the highest end of the range. What the figure represents, instead, is the price VCs appear willing to pay to be on the Anthropic cap table at any size heading into a possible public listing.

To put $800 billion in context, it is roughly the market capitalization of the fifth largest public company in the S&P 500 in early 2026, somewhere near the range of companies like Berkshire Hathaway or Tesla on a given day. It is more than double the $380 billion valuation Anthropic achieved when it closed a $30 billion round in February, and it is more than four times the value the company was assigned in its previous priced round eleven months before that. The pace of markup is what makes the figure meaningful. Investors are willing to pay a roughly 110 percent premium to the last round that closed, which is the kind of inflation you usually see in secondary transactions before a major liquidity event, not in a primary round from a company that just raised.

The revenue curve behind the number

The valuation math only works if Anthropic's revenue curve is as steep as reported. According to the Reuters figures cited in the Business Insider story, Anthropic's run-rate revenue now exceeds $30 billion, up from about $9 billion at the end of 2025. That is a roughly 3.3x increase in four months on an annualized basis, which is unusual at any scale and essentially unheard of at this one.

Run-rate revenue, for readers who have not spent time in software finance, is a forward projection that takes the most recent month's revenue and multiplies it by twelve. It is not the same as annual recurring revenue booked against contracts, and it is not the same as trailing twelve-month revenue. It is a snapshot, and snapshots can move quickly in both directions. But at this scale, even accounting for the flattering math, Anthropic is now one of a very small number of software companies in history to cross $30 billion run-rate inside five years of shipping a product.

| Milestone | Date | Reported Figure | Source |

|---|---|---|---|

| Prior priced round valuation | March 2025 | ~$184 billion | Prior public reporting |

| Run-rate revenue, end of 2025 | December 2025 | ~$9 billion | Reuters, April 14, 2026 |

| February 2026 round closed | February 12, 2026 | $30B raised at $380B valuation | Reuters |

| Mythos model announced | April 7, 2026 | Flagship coding/agentic model | Anthropic |

| Current run-rate revenue | April 2026 | >$30 billion | Reuters / Business Insider |

| Informal VC offers (new) | April 2026 | Up to $800 billion | Business Insider, April 14, 2026 |

The implied revenue multiple at $800 billion is worth pausing on. At a $30 billion run-rate, eight hundred billion is a roughly 27x multiple on forward revenue. Public software comparisons are well below that number in 2026. Even NVIDIA, which has been the benchmark for AI-era valuation multiples, has generally traded in a lower range against its own annualized revenue. Anthropic's pricing, in other words, is not being set by comparison to traded assets. It is being set by the perceived scarcity of the underlying company.

Why VCs are chasing now, not later

There are two ways to read the recent approaches. The charitable read is that venture firms see Anthropic as the cleanest pure-play on frontier AI that is still private, and they want a position before a public listing repriced the risk for everyone. The less charitable read is that the firms are trying to deploy capital from vintages that need to be put to work, and Anthropic is the largest obvious destination for a big check.

"At this stage of the cycle, the bid for access is what drives the markup, not the underlying cash flow. Venture funds that missed the last two AI rounds are bidding for optionality, not ownership."

Jeffrey Emanuel, independent AI equity analyst and author of Doctor Emanuel's Notes

Both readings can be true at once. What matters for the company is whether taking the money changes anything about the business, and right now the public signal from Anthropic is that it does not want to. The Bloomberg report emphasized that the company has not run a process, has not hired a placement agent, and is not treating the inbound interest as a starting point for negotiation. That is the posture of a company that thinks its next major capital event is an IPO, not another private round.

The Mythos release and the revenue story

Part of the reason the revenue curve is moving the way it is has to do with a product announcement Anthropic made a week before the VC offers leaked. On , the company unveiled Mythos, a new flagship model it described as its most capable yet for coding and agentic tasks. Agentic, in this context, means the model can take multi-step actions with limited human oversight, rather than just answering a single prompt.

That positioning is important because coding and agentic work are the two highest-paying enterprise use cases for frontier models in 2026. Coding assistants are now a line item inside software development budgets at most large companies, and agentic systems are moving from pilot into production at companies that want to reduce the number of humans in analyst and operations seats. A model that is materially better than the prior generation on those two axes is a model that can directly raise what a customer is willing to pay per seat, which is the fastest way to move a run-rate number in enterprise software.

For more context on how that market is forming, see our earlier coverage of Big Tech's $470 billion 2026 AI infrastructure spend and the related Broadcom, Google, and Anthropic custom chip deal.

The IPO question

The most consequential piece of the story is the one the valuation talk is feeding into. Anthropic has been reported, since late 2025, to be exploring a public listing as early as this year. A company weighing an IPO does not typically want to close a large private round at a speculative valuation in the months beforehand, because that round will either set a soft ceiling the IPO has to clear or create an immediate down-round optic if the public price settles lower.

The $800 billion offers, from that angle, are a data point that sell-side bankers will absolutely use when pricing a public listing. Venture firms placing informal bids at twice the last priced round is the kind of signal underwriters look for when they build a range. It does not mean the IPO will price at $800 billion, but it means the conversation about where it could price just moved up.

"The IPO window for a company like this is going to be priced off forward revenue multiples that public investors will actually underwrite, not off the ceiling of private bids. There's often a significant gap between the two."

Angelo Zino, senior equity analyst at CFRA Research

There is also a structural consideration inside Anthropic's own cap table. Existing investors, including the large corporate holders, have a view on what a healthy pre-IPO mark looks like and what kind of lockup they want to clear before a public listing. A round that comes in above a round they just participated in can be positive for paper marks and negative for how a listing clears, depending on how it is structured. That is one of the reasons the company is reportedly slow-walking the approaches rather than accepting them.

What this says about the AI funding cycle

Zooming out, the Anthropic story is the clearest live signal about where the private AI funding cycle sits in April 2026. The number that matters is not whether Anthropic closes at $800 billion. The number that matters is that capital is still available at those prices for a very narrow list of companies, while funding for almost everyone else in the AI stack has either stagnated or compressed over the last two quarters.

That bifurcation is visible across the portfolio data. Frontier model developers, a handful of foundation infrastructure companies, and two or three vertical AI applications are absorbing most of the late-stage private capital flowing into the sector. Companies below that top tier are raising smaller rounds at flat or down valuations, and several are shifting toward debt financing instead, as Mistral did earlier this month with an $830 million debt facility tied to its Paris data center buildout. See also our February 2026 record startup funding recap for the earlier data on the concentration pattern.

What that concentration does to the broader venture market over the next two quarters will matter for founders and limited partners. A market where the top three companies absorb most of the capital is a market where the median founder has a harder time raising, even while headline numbers keep setting records. Those two things can be true at the same time, and the Anthropic story is the clearest recent example.

What to watch next

The next data points are going to arrive quickly. If Anthropic decides to take one of the offers, even a small one, it will confirm that the $800 billion range is a real number rather than a negotiating posture. If the company instead files for an IPO in the next eight weeks, the pricing conversation will move to the public markets and the VC range becomes a backstop reference rather than a ceiling. If neither happens, the story is that Anthropic is deliberately controlling its own cap table during the most active window for AI capital since the ChatGPT release.

There is also the question of whether any of the major corporate backers, notably Amazon and Google, reopen their own positions at the new implied price. Strategic capital at this valuation would have different optics than venture capital, and would say something different about where the largest tech companies think Anthropic sits in their own competitive stacks. For related context on the big tech positioning around Anthropic, see our earlier reporting on Big Tech's legal support for Anthropic in its fight with the Pentagon.

The valuation number is the headline. The IPO timing, the revenue durability past $30 billion, and the Mythos adoption curve are the things that will actually determine whether the number holds.

Frequently Asked Questions

Has Anthropic accepted any of the $800 billion offers?

No. According to both the Business Insider and Bloomberg reports, Anthropic has so far resisted overtures for a new round and has not formally engaged with the offers. The company has not run a process, has not hired a placement agent, and is not publicly treating the inbound interest as the start of a negotiation.

How does $800 billion compare to Anthropic's last official valuation?

The company's last confirmed priced round closed in February 2026, when it raised $30 billion at a $380 billion valuation. The $800 billion figure represents roughly a 110 percent markup over that round, which is unusually steep for a company that has not held another formal priced financing since.

What is Mythos and why does it matter to the valuation?

Mythos is Anthropic's flagship frontier model, announced on April 7, 2026, and described by the company as its most capable yet for coding and agentic tasks. Coding and agentic work are the two highest-paying enterprise AI use cases in 2026, and a material improvement on those axes can translate directly into higher enterprise seat pricing, which is the fastest way to move a revenue run rate.

Is Anthropic going public?

Anthropic has been reported, since late 2025, to be exploring an initial public offering as early as 2026. The company has not filed an S-1, and the timing has not been confirmed. The recent VC interest is widely seen as informal pricing signal ahead of a potential listing.

What is run-rate revenue and why is it not the same as ARR?

Run-rate revenue is an annualized projection derived from the most recent month's revenue multiplied by twelve. Annual recurring revenue, or ARR, is the contracted recurring portion of that revenue booked against customer agreements. The two figures can diverge, especially at companies with a large share of usage-based or consumption-based pricing, which is common in the frontier AI model business.