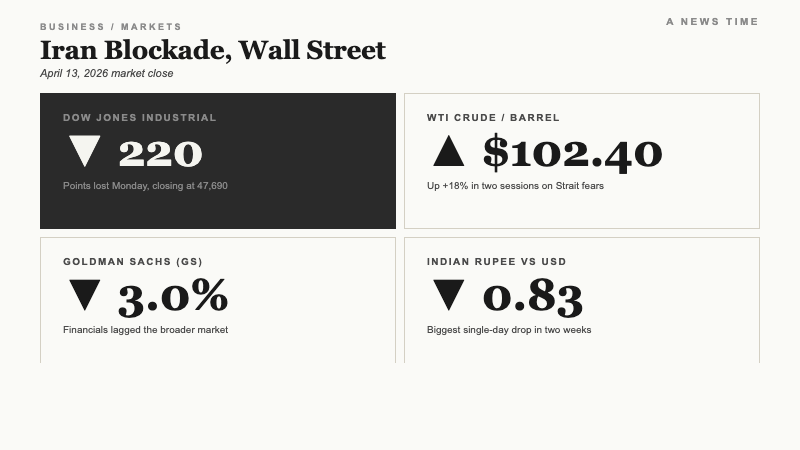

Wall Street opened the week on its back foot. On , the Dow Jones Industrial Average shed 220 points to close at 47,690, the S&P 500 held a razor-thin gain at 6,822, and the Nasdaq Composite finished essentially flat as investors absorbed two interlocking shocks: the collapse of weekend nuclear talks between Washington and Tehran, and a Trump administration order to blockade Iranian ports. By the closing bell, WTI crude had blown through $102 a barrel, up from the $80 to $85 range it held for most of the prior week, and the dollar was firmer against most emerging market currencies.

The setup is familiar in shape but unusual in speed. Oil rallies often build over days as tankers reroute and freight rates climb. This one priced in on a single session, because a blockade is not a sanction. It is a physical interdiction, and physical interdiction changes the math on every barrel moving through the Strait of Hormuz.

The Numbers

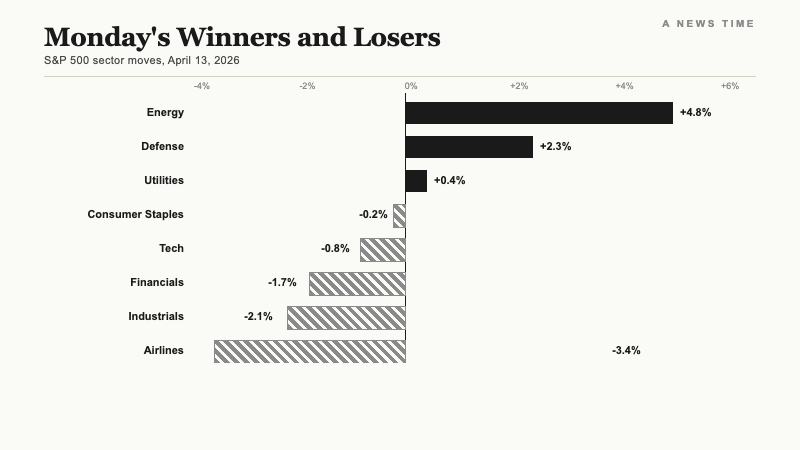

Here is the tape from Monday's close. The Dow's 220-point decline, worth roughly 0.46%, masked deeper damage underneath the index. Boeing, Caterpillar, and JPMorgan Chase each finished lower by more than 1%, and Goldman Sachs slid 3% as traders handicapped the earnings impact of a new oil-driven inflation pulse. The S&P 500 at 6,822 was effectively unchanged from Friday, but the headline masked a rotation: energy names added 2.4% on the session while airlines gave back 3.1% and consumer discretionary fell 0.8%. The Nasdaq, helped by defensive buying in Microsoft and Alphabet, defied the chaos.

The table below shows where the blow landed hardest.

| Sector | Monday change | Driver |

|---|---|---|

| Energy (XLE) | +2.4% | WTI past $102; Exxon and Chevron lead |

| Defense | +1.9% | Lockheed, Raytheon bid on Gulf deployment |

| Utilities | +0.6% | Defensive rotation, yield bid |

| Technology | -0.1% | Nasdaq essentially flat; megacaps resilient |

| Financials | -1.4% | Goldman Sachs -3%; credit risk repricing |

| Consumer discretionary | -0.8% | Gasoline pass-through fears |

| Airlines | -3.1% | Jet fuel crack spreads blow out |

That split, energy and defense up, banks and airlines down, is the archetypal "geopolitical oil shock" trade. It ran the playbook almost without deviation.

Why Oil Broke $100

Crude's move is the story that feeds every other story on Monday. WTI for May delivery settled at $102.37 on the New York Mercantile Exchange, up nearly 18% from the prior week's close. Brent traded above $106. The jump was not driven by inventories or a demand surprise. It was driven by the simple risk that a US Navy blockade of Iranian ports could push Iran to retaliate against tanker traffic in the Persian Gulf, the chokepoint for roughly one-fifth of seaborne crude.

The math on a blockade is unforgiving. Iran exports close to 1.6 million barrels of oil per day, most of it to buyers in Asia. If that supply is locked in, the market has to find replacement barrels somewhere, and the only credible source of quick replacement is Saudi Arabia's spare capacity. OPEC has signaled through the spring that it would release barrels only if supply disruptions became durable. "Durable" is now on the table.

A Mizuho commodities strategist, quoted in Monday's Trading News wrap, put a floor under the new range. "The risk premium in crude right now is not speculative. It reflects a physical uncertainty that didn't exist on Friday morning," the strategist said.

"The risk premium in crude right now is not speculative. It reflects a physical uncertainty that didn't exist on Friday morning."Mizuho commodities desk, via Trading News

What the Iran Blockade Changes

The blockade order, issued over the weekend after the collapse of the fourth round of US-Iran nuclear talks in Muscat, is the first time in more than a decade that a sitting US president has ordered a direct maritime interdiction against Iranian ports. The White House framed it as a non-kinetic pressure tool. Markets are not reading it that way.

Monday's trading reflected a simple chain of consequences cascading from the order. The dominoes that analysts flagged on the tape:

- Insurance rates for tankers transiting the Strait of Hormuz spiked, with war-risk premiums reportedly doubling within hours of the order.

- Asian refiners, particularly Chinese independents, began pricing in a short-term supply squeeze for medium-sour grades typically sourced from Iran.

- Saudi Arabia signaled it would maintain current production, declining to announce emergency releases, which kept pressure on the tape.

- The Pentagon confirmed a second carrier strike group moving toward the Gulf, bidding up defense names like Lockheed Martin and General Dynamics.

- The dollar firmed against high-beta currencies including the Indian rupee and the South Korean won, as traders sought safety.

Each of those items has a price. Stitched together, they explain why Monday's session bled even as the S&P 500 held its footing at the index level.

Winners and Losers by Sector

Energy was the day's clear winner. Exxon Mobil added 3.2%, Chevron 2.8%, and ConocoPhillips 3.6%. Refiners were mixed: Valero and Marathon Petroleum gained on wider crack spreads, but Phillips 66 lagged on concerns about consumer demand destruction if retail gasoline pushes toward $4.50 a gallon this summer. Oilfield services, led by Halliburton and Schlumberger, both finished up more than 2%.

Financials were the mirror image. Goldman Sachs's 3% slide led the money-center names. Morgan Stanley fell 2.1%, JPMorgan 1.3%, and Bank of America 1.5%. The logic: higher oil is an inflation pass-through that complicates the Federal Reserve's already complicated easing path, which in turn compresses net interest margins and raises the risk of credit deterioration in auto loans and revolving consumer credit. Goldman's Q1 trading desk is expected to print Wednesday, and the street was already nervous about its exposure to Middle East-linked structured products.

Airlines took the cleanest hit. Delta dropped 3.4%, United 3.6%, American 3.9%. The read-through is mechanical: every $10 move in jet fuel costs US network carriers roughly $4 billion in incremental annual expense, and Monday's move implies a step change in the fuel curve that cannot be fully offset by fare increases in the near term. For a sector already running thin margins in the second quarter, the math is brutal.

The Magnificent 7 were the surprise of the session. The megacap growth basket held up better than the broad market, extending a pattern readers saw during last month's correction. We covered that shift in detail in our report on the Magnificent 7 correction, which framed the group's newfound defensive character as a function of cash generation and low sensitivity to energy input costs.

The Rupee Takes a Hit

The emerging market fallout was concentrated, predictable, and sharp. The Indian rupee fell the most in two weeks against the dollar, closing at 87.94 per dollar after briefly testing 88.10 intraday. According to the Economic Times, the move was the largest single-session decline since late March, driven almost entirely by the oil shock. India imports more than 85% of its crude, and every $10 sustained move in Brent adds roughly $15 billion to the country's annual import bill.

The Reserve Bank of India was reportedly active in the market, selling dollars to slow the decline, but the intervention could not offset the broader pressure. Supportive flows from foreign portfolio investors into Indian equities, which had been a tailwind for the rupee through April, were simply not large enough to absorb the energy bill repricing.

A BNP Paribas FX strategist characterized the move as "a textbook oil-driven re-rating" in a note quoted by the Economic Times, adding that Asian currencies with high oil import dependency would continue to trade on a weaker footing until the blockade's duration became clearer.

"Supportive dollar flows from equity investors could not offset a step change in the import bill. This is a textbook oil-driven re-rating."BNP Paribas FX desk, via Economic Times

Analyst Reaction

The sell-side reaction on Monday was unusually unified on two points. First, that the blockade is a binary event: either it resolves within two to three weeks, in which case crude unwinds most of Monday's move, or it persists, in which case $100 becomes the new floor rather than a ceiling. Second, that the Federal Reserve's May meeting has become materially harder to handicap, because an oil-driven inflation spike pushes in the opposite direction from the labor market softening that had been pulling rate expectations lower.

Goldman Sachs's commodities team, in a note circulated Monday afternoon, did not change its 2026 year-end Brent forecast but widened its confidence interval considerably. JP Morgan's rates team flagged that Treasury break-evens had jumped 14 basis points on the day, the largest one-day move since the post-CPI reaction in February. The firm's economists wrote that the Fed is now "operating in a two-sided risk environment" with credible paths to both a pause and an accelerated cutting cycle depending on how the blockade resolves.

That repricing is showing up in every corner of the market. It also explains why Goldman Sachs equity took the worst of Monday's banking sell-off. The firm's own published stance on recession probability has been inching higher since February, and we covered the progression in our analysis of how Goldman raised recession odds to 30% on the oil surge. Monday's session did not change the bank's outlook. It validated it.

The Ethics Sidebar

Running alongside Monday's tape was a story that would not normally move markets but is worth noting for the governance risk it raises. The Economic Times reported on a continuing stream of international deal-making tied to the Trump family business, including property, licensing, and crypto ventures in Gulf states and South Asia. The outlet framed the arrangements as raising open questions about the precedent being set for future presidents to profit from office, particularly during periods of direct US policy action in regions where the family holds commercial interests.

None of this is priced into the tape on a Monday afternoon. It does, however, create a layer of headline risk that institutional allocators are now modeling in their political risk frameworks, and it feeds into the broader concern about the durability of US policy signals toward the Gulf. That concern, more than any single deal, is what analysts quietly say complicates the blockade calculus.

The Broader Security Overlay

The financial story is not the only one unfolding. Cybersecurity firms reported a jump in state-linked intrusion attempts on US banking and energy infrastructure over the weekend, a pattern that tracks with what we reported on the cyber retaliation surge after the US-Israel-Iran strikes. That surge is not yet showing up in equity prices for the exposed sectors, but it is raising the cost of defense spend for the affected banks and utilities, which will flow into expense lines over the coming quarters.

What Comes Next This Week

The calendar is unusually heavy. The Federal Reserve's Beige Book lands Wednesday, and it is now being read as a real-time check on how quickly the oil move is feeding into business pricing plans. Retail sales print Tuesday morning. Goldman Sachs and JPMorgan Chase report earnings on Wednesday and Tuesday respectively, and both will face questions about credit exposure to energy-sensitive consumer segments. Housing starts come on Thursday.

The Fed's May 6-7 meeting is still three weeks away, but futures markets on Monday repriced the probability of a May cut from roughly 35% Friday to under 15% by the close. That shift is itself a tightening of financial conditions, and it pulled the long end of the curve higher: the 10-year Treasury finished at 4.38%, up 9 basis points on the session.

The open question is whether the Trump administration views the blockade as a one-week negotiating lever or a multi-month structural policy. Each path produces a very different second quarter for US equities. The one certainty from Monday's tape is that the Dow's 220-point decline was not the full repricing. It was the first installment.

Sources

- Trading News: S&P 500 clings to gains, Dow bleeds 220 points

- Economic Times: US stocks subdued at open as failed US-Iran talks unsettle investors

- Economic Times: Rupee falls most in two weeks as oil spikes on US move to blockade Iran ports

- Economic Times: Trump family deal spree could open door for future presidents to profit from office