China's CSI 300 Index on recovered all of the losses it had sustained since the US-Israeli war on Iran began on , becoming the latest major Asian gauge to close back above its pre-war level and the third mainland-linked Asian benchmark to do so after Taiwan and Singapore. Bloomberg reported the move in its Wednesday markets wrap, and the Shanghai Composite added 0.4 percent on the session while Hong Kong's Hang Seng rose 0.8 percent. The offshore yuan strengthened for an eighth consecutive day. The recovery puts Chinese equities in the same company as the S&P 500, which has been closing in on its late-January record, and it reframes a question investors have been asking for six weeks: whether the Iran war is a supply-side shock or a durable risk premium on global risk assets. The price action now says the former.

What led the recovery

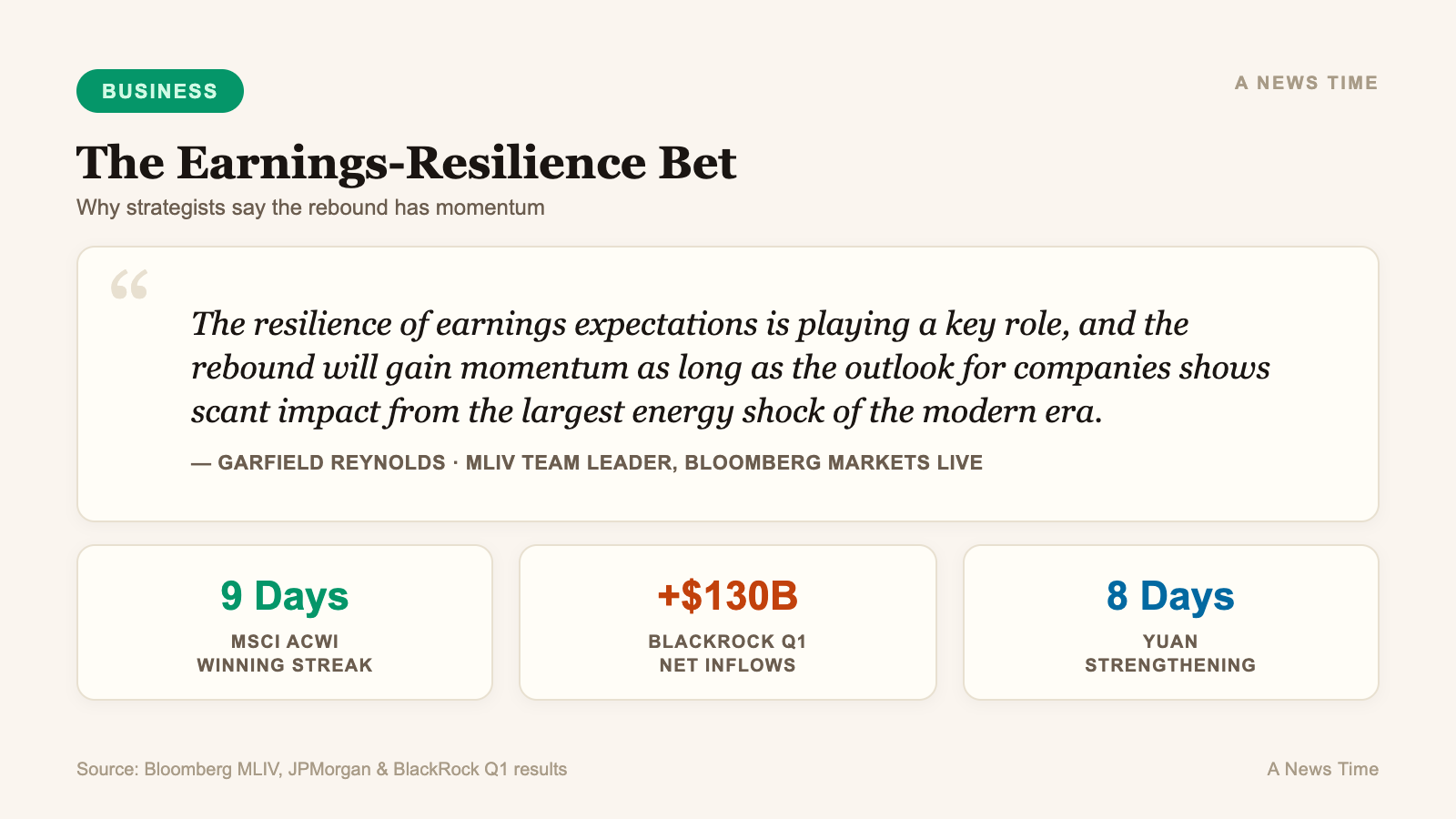

The CSI 300 had been down as much as 6 percent from its pre-war close in the days following , tracking the sharper slide in European and Japanese benchmarks. The recovery leadership on Wednesday was broad rather than concentrated, with financials and consumer-facing names outpacing commodities. South Korea's Kospi, the world's second-best performing benchmark year-to-date, jumped 2.9 percent in the same session, and Japan's Topix added 0.5 percent. MSCI's Asia Pacific equity index rose 1.1 percent, extending the MSCI All Country World Index's winning streak to nine sessions, which according to Bloomberg is the longest since September.

The immediate catalyst was not a piece of fundamental data. It was reporting from Bloomberg that US and Iranian delegates were preparing to return to Pakistan for a second round of peace talks within 48 hours, following an inconclusive weekend session in Islamabad. President Donald Trump told Fox News on Tuesday that he saw the war as close to ending, and Brent crude briefly traded below $94 a barrel on the comments before recovering to $95.75. The sequence was straightforward: oil softened, rate-hike bets eased, Asian risk assets rallied.

"Markets are turning up the risk appetite as US-Iran talk resumes. The sustainability of this risk-on rally may still need testing, given the volatile nature of peace talks."

Anna Wu, cross asset strategist, Van Eck Associates Corp.

Copper also advanced enough on Wednesday to erase its war-related losses, a more reliable industrial tell than any single equity index. Copper's full recovery suggests that the physical side of the commodity complex is pricing a faster normalization than US Treasuries are, with the 10-year yield still parked near 4.25 percent, roughly 30 basis points above its pre-war level.

The order in which Asian markets recovered

The sequence of recovery says something about what global investors are treating as the real vulnerability to the Iran war. Taiwan and Singapore recouped their war losses first, because both markets are heavily weighted toward technology exporters whose cash flows depend more on demand from US hyperscalers than on the price of oil. The CSI 300 followed because Chinese consumption and domestic financials are largely insulated from the Middle East supply shock as long as Iranian crude continues to find its way to refineries in Shandong. Japan's Topix and Australia's ASX 200 remain closer to pre-war levels but have not yet fully erased the drawdown, which reflects Japan's heavy gas import dependence and Australia's commodity sensitivity.

| Asian Benchmark | Status vs. Pre-War (Feb 28, 2026) | Key Sector Exposure |

|---|---|---|

| Taiwan TAIEX | Fully recovered (earliest) | Semiconductors, AI supply chain |

| Singapore STI | Fully recovered | Banks, regional trade |

| China CSI 300 | Fully recovered on April 15 | Financials, consumer, state-owned enterprises |

| Hong Kong Hang Seng | Less than 1% below | Tech, Chinese financials |

| Japan Topix | Within ~2% of pre-war close | Exporters, autos, gas-dependent utilities |

| Australia ASX 200 | Still below pre-war | Iron ore, energy, banks |

China's full recovery is particularly notable given how cautious the outlook on Chinese corporate earnings has been. Bloomberg reported on that the 90-day correlation between the CSI 300 and the Bloomberg China Treasury Total Return Index had turned positive, which is unusual and reflects a classic wartime haven bid. In normal conditions, Chinese stocks and Chinese government bonds move on different cycles. When they move together, investors are treating the combined Chinese asset complex as a single defensive allocation. That is the shape of the trade that held through the drawdown and is now unwinding into the rally.

Earnings resilience as the underlying bet

The durable argument behind the rebound is an earnings argument, and it is the one Bloomberg's strategists called out explicitly. Garfield Reynolds, the MLIV Team Leader in Bloomberg's Markets Live commentary team, wrote on Wednesday that "the resilience of earnings expectations is likely playing a key role, and the stocks rebound will gain momentum as long as the outlook for companies shows scant impact from the largest energy shock of the modern era." In other words: the reason the CSI 300 can recover is that consensus 2026 earnings estimates for constituent companies have not meaningfully fallen.

The US banking results released this week support that reading. JPMorgan Chase reported record quarterly trading revenue, although shares slipped on weaker commentary around net interest income. Citigroup posted its highest quarterly return on tangible common equity in five years, and shares rose. BlackRock took in a net $130 billion of client cash in the first quarter, with shares up 3 percent on Tuesday. For a war that was supposed to break markets, the marquee financial institutions are producing capital inflows, record desk revenue, and record returns on capital.

"Companies continue to show remarkable resilience in the face of supply chain, tariff, and now energy challenges. This should be reassuring for investors."

Scott Helfstein, head of investment strategy, Global X ETFs

The risk to that view is that Q1 2026 earnings captured only about four weeks of war impact, and the real test of whether earnings expectations hold comes with Q2 guidance. Eurozone utilities, Japanese refiners, and airlines everywhere are the three earnings-bucket categories where the Iran war shock should actually show up in reported numbers. If those companies guide down on Q2 calls, the earnings-resilience argument thins out fast. For now, analysts are holding their estimates, which is why the rally can exist.

What Chinese resilience says about the global risk premium

The Iran war has always sat at the intersection of two narratives. One narrative treats it as a classic oil-supply shock, comparable to the 1973 embargo or the 2022 Russia-Ukraine invasion, in which the correct response is to build a structural risk premium into every risk asset and leave it there until the supply situation is unambiguously resolved. The other narrative treats it as an event-driven spike, comparable to the 2019 Abqaiq attack on Saudi oil facilities or the 2020 Iran-US airstrike exchange, in which the premium fades within weeks once the situation fails to escalate to a worst case. The CSI 300 crossing back above its pre-war close is a vote for the second narrative.

The rally is not a vote that the war is over. It is a vote that the war is bounded. Brent fluctuating around $95 a barrel while peace talks slip and restart, with the strait blockaded but still leaking through Chinese carriers, is exactly the scenario where a bounded-risk framework works. For background on how that bounded scenario is being priced into Wall Street strategy, see our earlier coverage of Wall Street strategists' Iran-war outlook and the broader Wall Street rally on de-escalation hopes.

Two conditions have to hold for the CSI 300 to stay above its pre-war line. The first is that peace talks in Pakistan produce at least a framework for de-escalation within the next two weeks. The second is that Chinese Q1 earnings season, which begins in earnest next week, does not deliver the kind of negative surprises that Bloomberg flagged when the latest Chinese corporate results began coming in softer than expected. Both conditions are live questions, not foregone conclusions.

What to watch next

The immediate test is the Pakistan talks. If a date is locked for Islamabad round two and oil trades below $93 on the announcement, the recovery extends and European benchmarks that have not yet erased their drawdowns begin catching up. The UK's FTSE 100 and Germany's DAX both remain several percentage points below pre-war levels, reflecting the IMF's large growth downgrades for both economies. A full European recovery would be the signal that the bounded-risk framework has won the debate.

The second test is Q1 earnings guidance from Chinese banks and state-owned enterprises, which start reporting in the final week of April. Third is the path of the offshore yuan, which has now strengthened for eight consecutive days and has room to run further if Chinese risk assets continue normalizing. Currency strength on this pattern is the cleanest single-variable confirmation that foreign capital is re-engaging with mainland equities after the war-driven outflows.

For investors who have been underweight emerging markets since February on Iran-war risk, the CSI 300 recovery resets the base case. The question now is whether the rally is a mid-cycle pause point or the start of a durable reallocation back toward Asian equities, and the answer depends less on what oil does tomorrow than on whether the earnings resilience story holds through Q2. The next three weeks of reporting will settle it.

Frequently Asked Questions

When did the CSI 300 erase its Iran-war losses?

China's CSI 300 Index closed back above its pre-war level on April 15, 2026, roughly six and a half weeks after the US-Israeli war on Iran began on February 28. It was the third major Asian benchmark to do so, following Taiwan and Singapore.

Which other Asian markets have recovered?

Taiwan and Singapore recouped their losses first, driven by semiconductor and banking exposure that is relatively insulated from oil. Japan's Topix is within about 2 percent of its pre-war close, Hong Kong's Hang Seng is less than 1 percent below, and Australia's ASX 200 is still trading below pre-war levels due to commodity sensitivity.

What is driving the rally?

The immediate catalyst is reporting that US-Iran peace talks will resume in Pakistan within days, which softened Brent crude back below $95 a barrel. The deeper argument is that Q1 2026 corporate earnings, particularly at US banks, have shown resilience that supports unchanged forward consensus estimates.

Is Chinese risk exposure still elevated?

Yes. Bloomberg reported that the 90-day correlation between the CSI 300 and Chinese government bonds turned positive during the war, which is unusual and reflects haven-bid behavior. Chinese Q1 corporate earnings have also disappointed on the margin, which means the CSI 300's recovery leaves it vulnerable to downside surprises in earnings season.

What would break the recovery?

The two main risks are a breakdown in the upcoming Pakistan peace talks and a broad wave of Q2 guidance cuts from companies most exposed to the energy shock, including European utilities, Japanese refiners, and global airlines. Either could reprice Asian equities back toward their war lows.

Sources

- Stocks Are Erasing War Losses on Hopes Over Talks: Markets Wrap - Bloomberg via SWI swissinfo.ch

- Asia Markets Begin Clawing Back War Losses on Easing Tensions - Bloomberg

- China's Stocks, Bonds in Rare Sync as War Drives Haven Demand - Bloomberg

- IMF downgrades global growth outlook as Iran war hits prices - Reuters