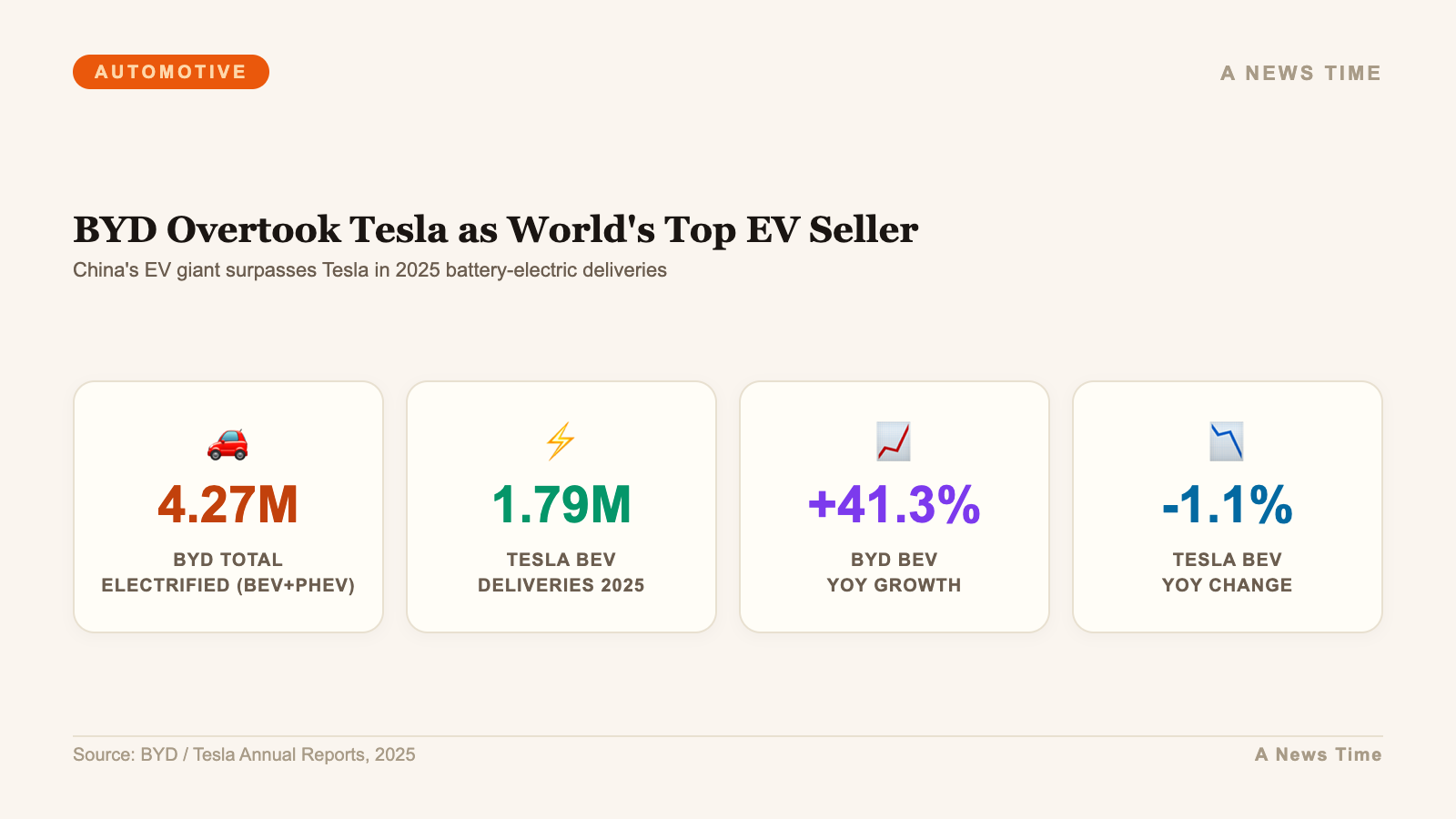

The number that defines the global automotive story of 2025 is straightforward: BYD, the Shenzhen-based automaker backed by Warren Buffett and built on decades of Chinese state support for domestic technology, sold more pure-electric vehicles than Tesla in calendar year 2025. The precise figures depend on counting methodology, but across multiple analyst interpretations, BYD's battery-electric vehicle deliveries crossed parity with and in some counts exceeded Tesla's. Including plug-in hybrids, the gap is not close: BYD sold approximately 4.27 million electrified vehicles to Tesla's 1.79 million pure EVs.

This is not a tactical pricing victory or a temporary aberration. It is the visible output of a strategic investment cycle that China began in the 1990s when it decided that electric vehicles were the domain where a domestic automaker could compete with and eventually surpass Western incumbents. BYD's 2025 result is the maturation of that strategy. Tesla's response, or lack of one at the entry-level price point, is the story of what happens when a company prioritizes margin and robotaxi ambitions over volume during a market inflection.

The Numbers: What BYD vs. Tesla Actually Looks Like

Parsing the BYD-versus-Tesla comparison requires care because BYD reports its numbers in ways that include plug-in hybrids (PHEVs) alongside pure battery electrics (BEVs). Tesla sells only pure EVs. Direct BEV-to-BEV comparison is the apples-to-apples metric.

| Metric | BYD | Tesla | BYD Advantage |

|---|---|---|---|

| Total electrified (BEV + PHEV) | 4,272,145 | 1,789,226 | +2.39x |

| Battery-electric only (BEV) | ~1,764,000 | 1,789,226 | Near parity (Tesla +1.4%) |

| Year-over-year BEV growth | +41.3% | -1.1% | BYD accelerating, Tesla declining |

| Revenue per vehicle (est.) | ~$21,000 | ~$42,500 | Tesla higher ASP |

| Primary markets | China (80%+), Europe, SE Asia | US, China, Europe | BYD more China-concentrated |

The trajectory is what makes the BEV comparison alarming for Tesla even in years where the raw count still marginally favors Elon Musk's company. BYD's pure BEV volume grew 41 percent year-over-year. Tesla's declined 1.1 percent. At these growth rates, BYD's BEV volume unambiguously surpasses Tesla's in 2026 unless Tesla launches new products or cuts prices enough to stimulate significantly higher demand.

China's Long Game: The Infrastructure That Built BYD

The conventional Western narrative about BYD's rise focuses on price competition. That framing is incomplete. BYD is not simply cheaper than Tesla; it is the product of an industrial policy that has been running for more than 30 years, across multiple Chinese government administrations, with consistent priority regardless of political cycle.

China's New Energy Vehicle policy framework dates to the 1990s, when the Ministry of Science and Technology identified EVs as a sector where Chinese domestic champions could build global competitive advantage before Western automakers had entrenched incumbent positions. The strategy included subsidized R&D grants for battery technology, preferential land allocation for factories, central-government purchase subsidies for consumers, and strict emissions regulations that effectively mandated EV adoption in major cities ahead of other markets.

BYD specifically benefited from early state support for battery research in the 2000s and from China's decision to allow domestic EV manufacturers to operate under rules that made it difficult for foreign automakers to fully own their Chinese EV joint ventures until 2018. By the time Western automakers had unrestricted access to the Chinese EV market, BYD had a decade-plus head start in manufacturing scale, supply chain relationships, and consumer brand recognition within China.

BYD's vertical integration is the tangible output of this investment. The company makes its own batteries (Blade Battery), its own semiconductors (IGBT chips for power electronics), its own electric motors, and its own vehicle bodies. This integration reduces exposure to supplier price fluctuations and gives BYD design freedom that parts-assembler automakers do not have. Tesla has moved toward similar vertical integration but has not matched BYD's depth, particularly in battery cell production at BYD's cost structure.

Tesla's Compounding Headwinds

Tesla's 1.1 percent volume decline in 2025 is not a single-cause problem. Multiple forces compressed demand simultaneously, and several are not easy to reverse quickly.

Brand sentiment deteriorated materially in key European markets, particularly Germany and Scandinavia, following political controversies associated with Elon Musk's public activities in 2024-2025. Tesla's European sales fell approximately 45 percent in 2025 versus 2024. That decline is not purely about the product; the Model Y remains a technically competitive vehicle. It reflects consumer choices in markets where brand values and corporate associations influence purchasing decisions more than in the United States.

The US federal EV tax credit expiration in 2025 removed the $7,500 subsidy that had made Tesla's least expensive configurations genuinely affordable for middle-income buyers. The Model Y Standard at $39,990 pre-credit was a $32,490 effective purchase for qualifying buyers. Post-credit, it is $39,990. That $7,500 reversion is concentrated entirely in the buyer segment Tesla needs to grow: first-time EV purchasers who are price-sensitive and were brought into range by the credit.

Tesla's product lineup has not received a meaningful entry-level expansion. The Model 3 and Model Y refreshes in 2023-2024 improved interior quality and technology but did not drop the price floor. The Cybercab is in production but is blocked from consumer sales by regulatory requirements for a driverless vehicle exemption that Tesla has not yet obtained. The Optimus robot remains a development-stage product. The compact SUV reported by Reuters is not coming before 2027 at the earliest.

For more on Tesla's declining US market dynamics: New EV Sales Drop 28% But Used EVs Surge to Record.

The Global EV Market Is Moving to Lower Price Points

The structural dynamic that favors BYD's continued growth is not political; it is economic. The majority of global auto sales growth over the next decade will come from markets where median household income makes a $35,000-$45,000 vehicle inaccessible without subsidies. Southeast Asia, India, Latin America, and Africa collectively represent billions of potential EV adopters, and the vehicles that will capture them will cost $12,000-$25,000, not $40,000.

| Price Segment | 2025 Volume Share | 2030 Projected Share | Key Players |

|---|---|---|---|

| Sub-$20,000 | 28% | 38% | BYD (Seagull), Wuling, SAIC |

| $20,000-$35,000 | 31% | 35% | BYD (Dolphin, Atto 3), Hyundai Kona EV |

| $35,000-$55,000 | 27% | 20% | Tesla Model 3/Y, VW ID.4, Ioniq 5 |

| $55,000+ | 14% | 7% | Tesla Model S/X, BMW iX, Rivian |

The two fastest-growing segments, sub-$20,000 and $20,000-$35,000, are dominated by Chinese brands domestically and BYD internationally. Tesla's core product lineup sits entirely in the $35,000-$55,000 segment, which is projected to contract as a share of global EV volume from 27 percent in 2025 to 20 percent by 2030. Tesla is strong in a segment that is proportionally shrinking.

BYD's strategy is the reverse. Its core volume is in the high-growth, lower-price segments, with premium models (Han, Tang, Seal U DM) moving it into the $35,000+ bracket as profitability has improved. BYD is climbing the value ladder from below while Tesla is trying to extend downward. Historically, climbing from below is harder to defend against than extending downward.

BYD's Global Expansion: Progress and Headwinds

BYD's geographic concentration remains its most significant structural vulnerability. In 2025, more than 80 percent of BYD's total EV volume was sold within China. The company is building factories in Hungary, Thailand, Brazil, and Mexico to reduce this concentration, but these facilities are not yet at scale.

The European Union's 2024 imposition of countervailing duties on Chinese-made EVs, ranging from 7.8 to 35.3 percent additional to the standard 10 percent import tariff, directly increased BYD's cost structure for China-to-Europe shipments. BYD's Hungarian factory, which broke ground in 2024 and is expected to begin production in 2025-2026, is a direct response to these tariffs. EU-manufactured BYD vehicles would be subject to the standard 10 percent rate only, removing the tariff disadvantage.

The United States remains effectively closed to BYD due to 100 percent tariffs on Chinese-made vehicles plus the Inflation Reduction Act's domestic content requirements for EV tax credits. BYD's Mexico factory is partly a hedge on a future U.S. market entry, though USMCA compliance requirements would still need to be met for the factory to qualify vehicles for US credits.

For deeper analysis of tariff impacts on automotive markets: Trump Tariffs Have Cost Automakers $35 Billion Since 2025.

What Chinese Innovation Actually Looks Like at This Scale

The BYD story is frequently framed in the West as a cost story. That framing misses what is arguably more significant: the pace of Chinese EV technology development has accelerated in ways that are not primarily explained by labor cost arbitrage.

BYD's Blade Battery, a lithium iron phosphate cell engineering innovation that dramatically improves thermal stability compared to conventional prismatic cells, was developed internally and deployed at scale before Western automakers had licensed the technology. BYD's fifth-generation DM (Dual Mode) plug-in hybrid system achieves a fuel consumption of 2.9 liters per 100 km in hybrid mode, which is better than any non-Chinese plug-in hybrid system available. BYD's 5C fast-charging battery, capable of charging from 10-80 percent in under 12 minutes when paired with a compatible charger, was announced in 2025 and is being deployed in multiple BYD and BYD-supplied models.

Huawei's AVATR collaboration, CATL's sodium-ion battery work, and the broader Chinese EV supplier ecosystem are producing innovations at a pace and scale that now constitutes genuine technical leadership in multiple EV subsystems, not just lower-cost replication of Western technology. This is the dimension of BYD's rise that Western automakers find most difficult to address with tariff policy: tariffs block the products but not the knowledge.

See our coverage of BYD's battery technology milestone: BYD's Super-Fast Charging Battery Is a Wake-Up Call.

What Happens Next

The 2026 trajectory is not favorable for Tesla's volume leadership, even on the BEV-only metric. BYD's 41 percent BEV growth rate in 2025, if sustained at even half that pace in 2026, will produce a BEV volume that exceeds Tesla's 1.79 million by a material margin. Tesla would need to grow its own deliveries meaningfully in 2026 to remain competitive on that specific metric, and the product and market conditions for that growth are not obvious.

Tesla's path to volume recovery runs through the compact SUV development confirmed by Reuters (likely 2027 at earliest), the FSD revenue stream as European approvals materialize (higher probability in the near term), and Cybercab commercial fleet deployment if regulatory approvals accelerate. None of these deliver 2025-to-2026 volume.

BYD's risks are also real: a Chinese economic slowdown that reduces domestic consumption, European tariff escalation that blocks international growth, geopolitical deterioration between China and its export markets, and the reputational complexity of being both a national champion and a global company. These are not trivial risks. But they do not change the underlying trajectory: BYD has the scale, supply chain, cost structure, and product lineup to sustain and extend its position as the world's dominant EV company.

The question for the rest of the global auto industry is whether the response involves genuine product and technology competition or primarily regulatory protection. The United States has chosen the latter so far. Europe is attempting both. The market data from 2025 suggests protection alone does not reverse the competitive dynamic; it just delays the consumer reckoning.