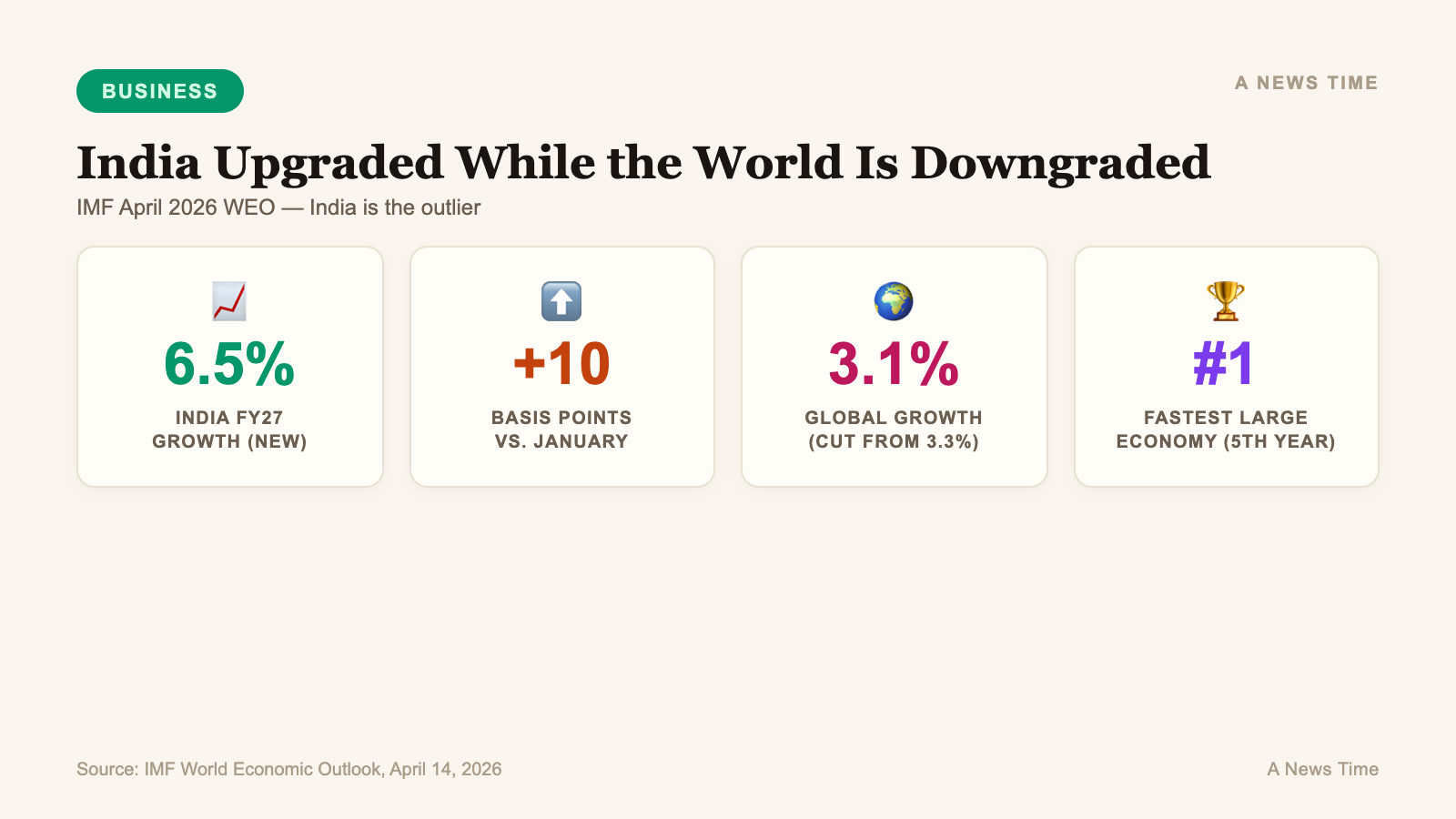

The International Monetary Fund on raised its growth forecast for India's financial year 2026-27 to 6.5 percent, a 10 basis point upgrade from its January projection, in a World Economic Outlook that otherwise cut the global growth outlook to 3.1 percent from 3.3 percent and downgraded nearly every other major economy on the Iran war's energy shock. India was one of the only large economies to receive an upward revision in the April report, and the IMF held its FY28 projection for India at 6.5 percent as well. The upgrade, disclosed in the WEO release at the IMF's spring meetings in Washington, keeps India on track to retain its status as the fastest-growing large economy in the world for a fifth consecutive year, and it arrives at a moment when global investors are actively searching for emerging market exposure that is not tightly coupled to Middle East oil price risk.

The specific revision

The IMF's January 2026 WEO had pegged India's FY27 growth at 6.4 percent. The April revision lifts that to 6.5 percent, which is consistent with the reporting from NDTV Profit and the Times of India. The fund's FY28 forecast for India is also held at 6.5 percent, implying a two-year horizon of steady growth well above the emerging market average of 3.9 percent. The IMF simultaneously cut its 2026 growth forecast for emerging market and developing economies as a whole to 3.9 percent from 4.2 percent in January, which makes the India upgrade look even sharper by comparison.

Two other multilateral institutions released their own India forecasts earlier in April. The World Bank projected India's FY27 growth at 6.6 percent, and the Reserve Bank of India penciled in 6.9 percent. The RBI is the most optimistic of the three; both the World Bank and RBI flagged Middle East tensions as the primary downside risk. The IMF's 6.5 percent call sits in the middle of that range and is the one that carries the most weight internationally because of the fund's reach with sovereign debt investors and credit rating agencies.

| Forecaster | India FY27 Growth Forecast | Change vs. Prior | Key Driver Cited |

|---|---|---|---|

| IMF (April 2026 WEO) | 6.5% | +10 bps vs. January | Lower US tariffs, resilient consumption |

| World Bank (April 2026) | 6.6% | Held | Domestic demand, services exports |

| Reserve Bank of India | 6.9% | Held | Government capex, rural demand |

| S&P Global Ratings | 6.3% to 6.5% (range) | -80 bps oil-shock risk | Oil import dependence |

The IMF's broader global downgrade from 3.3 percent to 3.1 percent puts India's upgrade in sharper relief. Without the Iran war, the IMF said, it would have raised global growth to 3.4 percent on the back of the technology investment boom, lower interest rates, and softer US tariffs. For India to get an upgrade inside a report whose headline is a downgrade, the fund had to see specific offsets that were strong enough to absorb a higher oil import bill. That is the analytical question this report answers.

What the IMF cited as drivers

The offsets fall into three buckets, all of which are referenced directly in the IMF's April 2026 World Economic Outlook. The first is private consumption, which remained robust through Q1 2026 and held up better than the fund expected when it drafted its January numbers. India's household savings rates have been recovering from post-pandemic lows, rural demand has firmed on normal monsoon expectations for calendar 2026, and goods-and-services tax collections have continued to run above forecast, suggesting that domestic transactional activity is absorbing the war shock more cleanly than external-facing economies are.

The second driver, and the one that matters most for the India-versus-rest-of-emerging-markets comparison, is US tariff policy. The Trump administration's tariff framework released earlier in 2026 placed India at a lower effective rate than most Asian competitors, including China, Vietnam, and Thailand. For a country whose services exports to the United States have been a growth engine for four straight years, a relatively lower tariff schedule is a real marginal positive, and the IMF priced it in. Informist Media reported that the fund's analytical note explicitly cited lower US tariffs as an offset to the Iran war hit on India's outlook.

The third driver is government capex. India's union budget for FY26 kept capital expenditure at record levels, with infrastructure, railways, and defense spending continuing to drive fixed-investment growth. The IMF has historically discounted announced capex plans against actual delivery, but in India's case the execution ratio has improved for three consecutive years, which is enough for the fund to carry the capex assumption into forward-year estimates rather than haircutting it heavily.

"For India, the revision reflects relative resilience, even though the country remains exposed to higher crude prices due to its heavy dependence on imported oil."

NDTV Profit, reporting on the IMF's April 2026 World Economic Outlook

The oil dependency qualifier

India imports roughly 85 percent of the oil it consumes, which is the largest single qualifier on any growth upgrade in this environment. The IMF's own reference forecast assumes Brent crude averages $82 a barrel for 2026, which is well below the $96 benchmark on the day the WEO was released. The fund's chief economist, Pierre-Olivier Gourinchas, acknowledged in a press conference on Tuesday that the reference forecast was "not quite yet" irrelevant but that the global economy was drifting between the reference scenario and the IMF's adverse scenario, in which oil averages $100 and global growth slows to 2.5 percent. For India, that would mean a materially higher import bill and a larger current account deficit, though the fund did not publish an India-specific sensitivity.

S&P Global Ratings, in a separate analysis cited by NDTV Profit earlier in April, said India's growth could slow by up to 80 basis points in an extended oil-shock scenario, taking FY27 growth closer to 5.7 to 5.8 percent. That is still well above the emerging market average, but it would represent a meaningful downshift from the 6.5 percent IMF baseline. The gap between those two views is where the asymmetry lies. If the IMF's reference scenario holds, India continues to outgrow its peers. If it does not, India slows but still finishes near the top of the global growth league table, which is the structural reason sovereign debt investors have been adding to India exposure through the war.

The Iranian toll system on the Strait of Hormuz is a secondary concern, though the Indian government has said publicly that Iranian officials have exempted Indian vessels from the tolls as of . That exemption, first reported by NDTV Profit, is one of the quieter tail-risk offsets for India's import cost structure, and it reflects the long-running Iran-India trade relationship that has survived earlier sanctions cycles.

How India compares to the rest of the IMF outlook

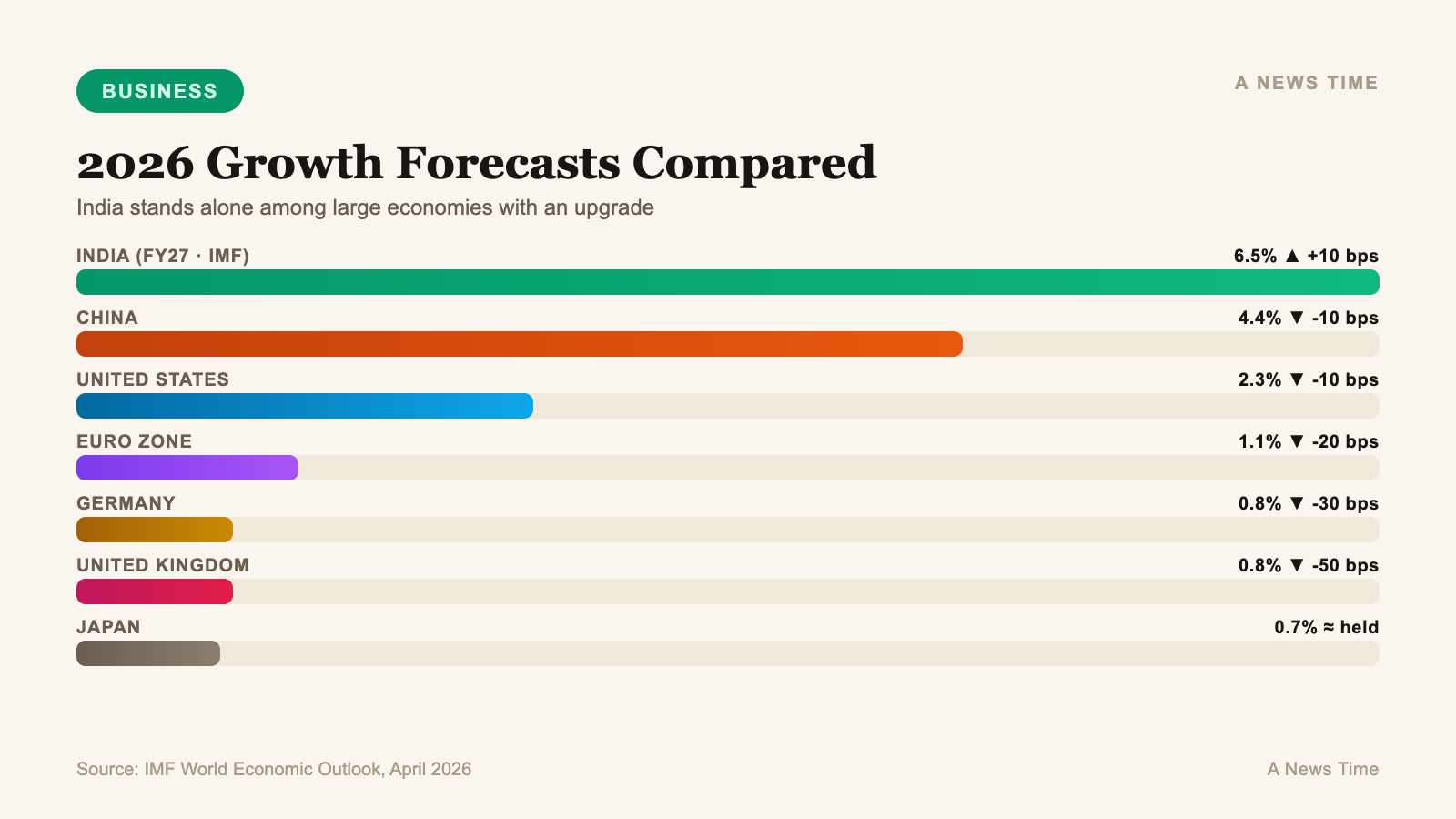

The comparison that matters for global investors is India versus the other large economies in the April WEO. The IMF kept US 2026 growth at 2.3 percent, only 10 basis points below its January projection, citing tax cuts, lagged interest rate cuts, and continued AI data center investment as offsets to higher energy costs. The euro zone was cut 20 basis points to 1.1 percent. Japan held at 0.7 percent for 2026. The United Kingdom took the sharpest G7 downgrade, falling to 0.8 percent from 1.3 percent, and Germany was cut by 30 basis points to 0.8 percent. China was cut 10 basis points to 4.4 percent on higher energy costs partially offset by softer US tariffs.

Inside that table, India at 6.5 percent is the outlier on three dimensions. It has the highest growth rate of any large economy. It is one of the very few countries with an upward revision. And its drivers, consumption and government capex, are more domestic than the growth stories for most of the other emerging market economies that the IMF tracks. That combination is exactly the profile that global emerging-market allocators have been hunting for since the war began in late February.

For a detailed look at how the Iran war is shaping investor allocation decisions, see our coverage of the OECD's global growth downgrade and the broader picture of IMF warnings on supply-disruption inflation risk. Both pieces lay out the global backdrop against which the India upgrade is being read.

What it means for global investors

The practical question for portfolio managers is whether an India overweight is the right way to fade the Iran-war risk premium elsewhere. The capital flows data through the first half of April suggest that is already happening on the margin. Foreign institutional investors turned net buyers of Indian equities in the last week of March after seven consecutive weeks of outflows, and the INR has strengthened against a broadly softer US dollar. India's sovereign yield curve has been remarkably well-behaved through the war relative to other large emerging markets, with the 10-year GoI bond yield roughly flat since late February. That is the behavior of an asset class being treated as a relative haven within the emerging market complex, which is a change from the pre-war assumption that India would trade in lockstep with the broader EM risk basket.

Two earnings checkpoints over the next six weeks will test whether the IMF's upgrade holds at the corporate level. India's largest private banks begin reporting Q4 FY26 results in the back half of April. ICICI Prudential Life Insurance shares jumped 5.67 percent on after reporting a nearly 58 percent surge in fourth-quarter profit, which Reuters flagged as a positive read on the financials segment. If the rest of the large-cap results follow the same pattern, the consumption and financials drivers the IMF cited will have corporate-level confirmation.

The second checkpoint is the RBI's next monetary policy committee meeting. The central bank has been running a relatively cautious stance on rate cuts compared with where market participants expected it to be at the start of 2026, and the April IMF upgrade gives it cover to hold that position rather than ease aggressively into the oil shock. A hold-and-watch RBI is historically supportive of Indian equity multiples, because it implies the central bank sees enough domestic demand strength that it does not need to front-load stimulus.

What to watch next

Three things worth tracking. The first is whether the IMF's reference oil assumption of $82 Brent holds by the next quarterly update, because any meaningful move toward the adverse scenario would force the fund to revisit India's number along with everyone else's. The second is the RBI's mid-year rate decision, which will set the cost of capital assumption behind the IMF's FY27 estimate. The third is the shape of US tariff policy into the fall, because any escalation that narrows the tariff gap between India and its Asian competitors would compress one of the three drivers the fund cited.

For investors rotating emerging market exposure into India on the back of the upgrade, the base case is intact and the tail risks are identifiable. The more consequential point is the one that shows up between the lines of the April WEO: in a report that downgraded the world, India moved up. That does not happen often, and when it does, capital tends to follow.

Frequently Asked Questions

What is India's new growth forecast from the IMF?

The IMF raised India's growth forecast for fiscal year 2026-27 to 6.5 percent, a 10 basis point upgrade from its January projection of 6.4 percent. The fund also held its FY28 forecast for India at 6.5 percent in the April 14 World Economic Outlook.

Why did the IMF upgrade India while downgrading other economies?

The IMF cited three offsets: lower US tariff rates on Indian exports compared with most Asian competitors, resilient domestic consumption supported by rural demand and GST collections, and continued record-level government capital expenditure on infrastructure and defense. These were strong enough to absorb a higher oil import bill.

How does India compare to China in the April WEO?

The IMF projected China's 2026 growth at 4.4 percent, a 10 basis point cut from January, while lifting India's FY27 projection to 6.5 percent. India is now forecast to grow at roughly 2.1 percentage points faster than China in 2026, the widest gap since the pandemic recovery period.

What is the biggest risk to India's 6.5 percent forecast?

India imports roughly 85 percent of its oil, so a sustained Brent crude price above $100 per barrel under the IMF's "adverse scenario" would raise the import bill and pressure the current account. S&P Global Ratings estimated earlier in April that an extended oil shock could slow India's growth by up to 80 basis points.

How did other multilaterals forecast India compared to the IMF?

The World Bank projected India's FY27 growth at 6.6 percent, and the Reserve Bank of India penciled in 6.9 percent. The IMF's 6.5 percent call is the median of the three and carries the most weight with international sovereign debt investors and credit rating agencies.

Sources

- IMF Makes Upward Revision To India's FY27 Growth Forecast Despite West Asia War Jitters - NDTV Profit

- World Economic Outlook, April 2026 - International Monetary Fund

- IMF downgrades global growth outlook as Iran war hits prices - Reuters

- IMF raises India growth forecast as lower US tariffs to offset Iran war hit - Informist Media