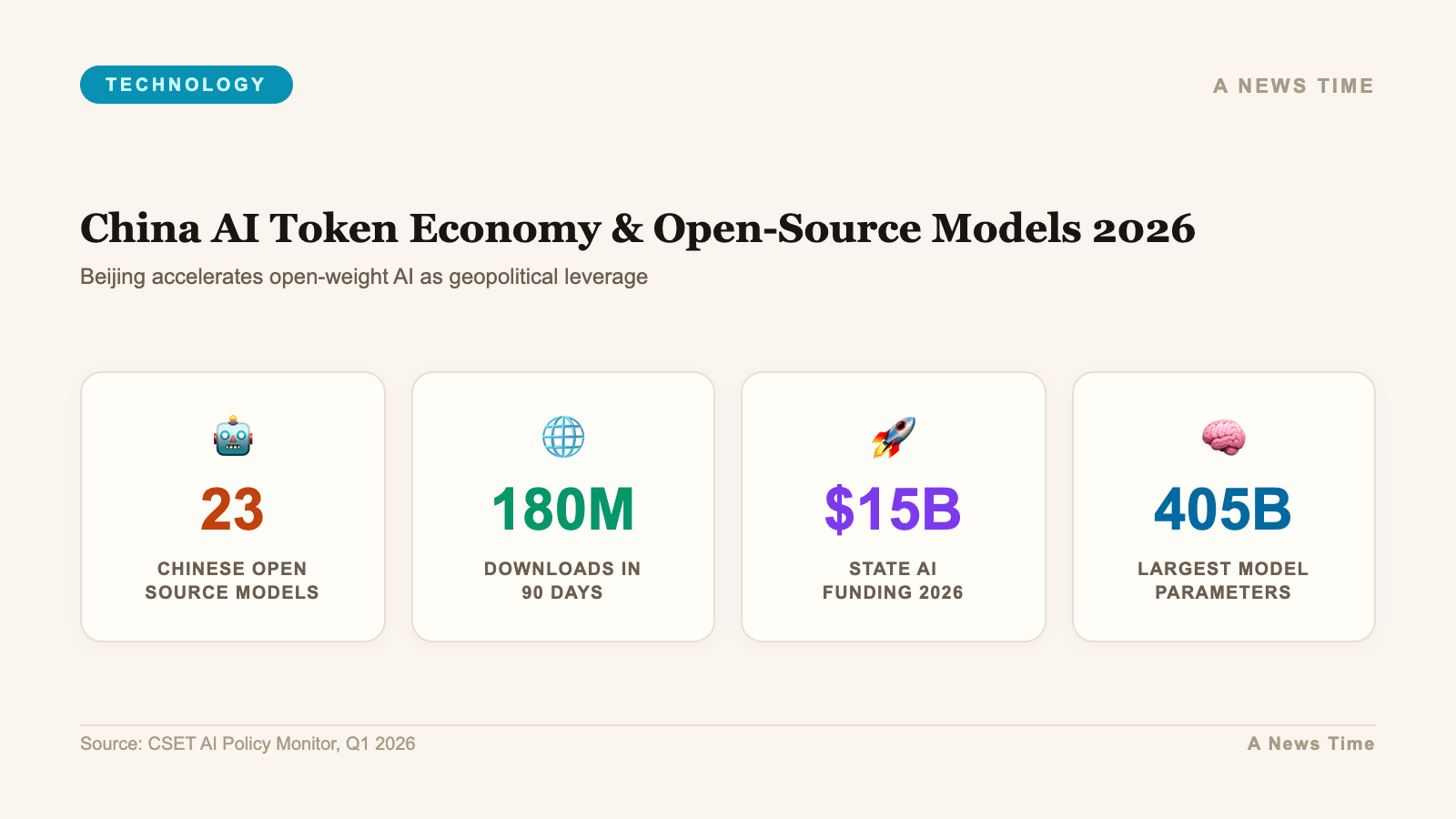

China now has a word for token: ciyuan. Liu Liehong, the administrator of China's National Data Administration, unveiled the term at a State Council press conference in , defining tokens as the "settlement unit linking technological supply with commercial demand." The announcement was not a marketing exercise. It was a policy signal: China has decided that AI tokens are to its digital economy what the yuan is to its physical one, a unit of account for an industrial transformation that the government intends to manage, measure, and expand.

The numbers behind that declaration are striking. China processed 140 trillion tokens per day as of early . At the start of 2024, the figure was 100 billion. That is a roughly 1,400-fold increase in daily token throughput in about two years, a growth rate that reflects not just infrastructure expansion but a genuine shift in how Chinese businesses, developers, and consumers are using AI at scale.

Fortune's Asia editor Nicholas Gordon published a comprehensive survey of China's AI landscape in , drawing on IPO filings, earnings data, government announcements, and industry reporting to map where the country's AI industry stands and where it is heading. What follows is a structured analysis of the key dynamics his reporting surfaces.

The Token Economy: A New Framework for AI Value

The phrase "token economy" is doing real conceptual work in how China's policymakers are framing AI development. In technical terms, a token is the basic unit of text that language models process, roughly three to four characters in most languages. But Liu Liehong's formulation elevates the concept to the level of economic infrastructure: tokens are how AI capability translates into commercial output, and the National Data Administration's disclosure of daily token volumes signals that the government is tracking this metric the way other countries track GDP growth or industrial production.

Alibaba made this framing explicit when it reorganized its entire AI operation into the Alibaba Token Hub in early . CEO Eddie Wu's internal letter announcing the reorganization stated that the unit is "built around a single organising mission: create tokens, deliver tokens and apply tokens." This is not accidental language. It mirrors the government's framing and signals that China's largest e-commerce company sees its future primarily as an AI infrastructure provider measured in token throughput.

The institutional architecture supporting this vision is substantial. The National Data Administration functions as a cross-sectoral regulator for data and AI, with authority to set standards, define metrics, and coordinate policy across government ministries and state-owned enterprises. When that body introduces a new economic concept like ciyuan, it is signaling that the measurement and governance infrastructure will follow. This is how China operationalizes strategic technology priorities: define the unit, measure it, subsidize it, and build regulation around it.

Big Tech Pivots: Alibaba, ByteDance, and Tencent

China's three largest internet companies have each staked out a distinct position in the AI race, and the differences between their approaches reveal important structural dynamics in the market.

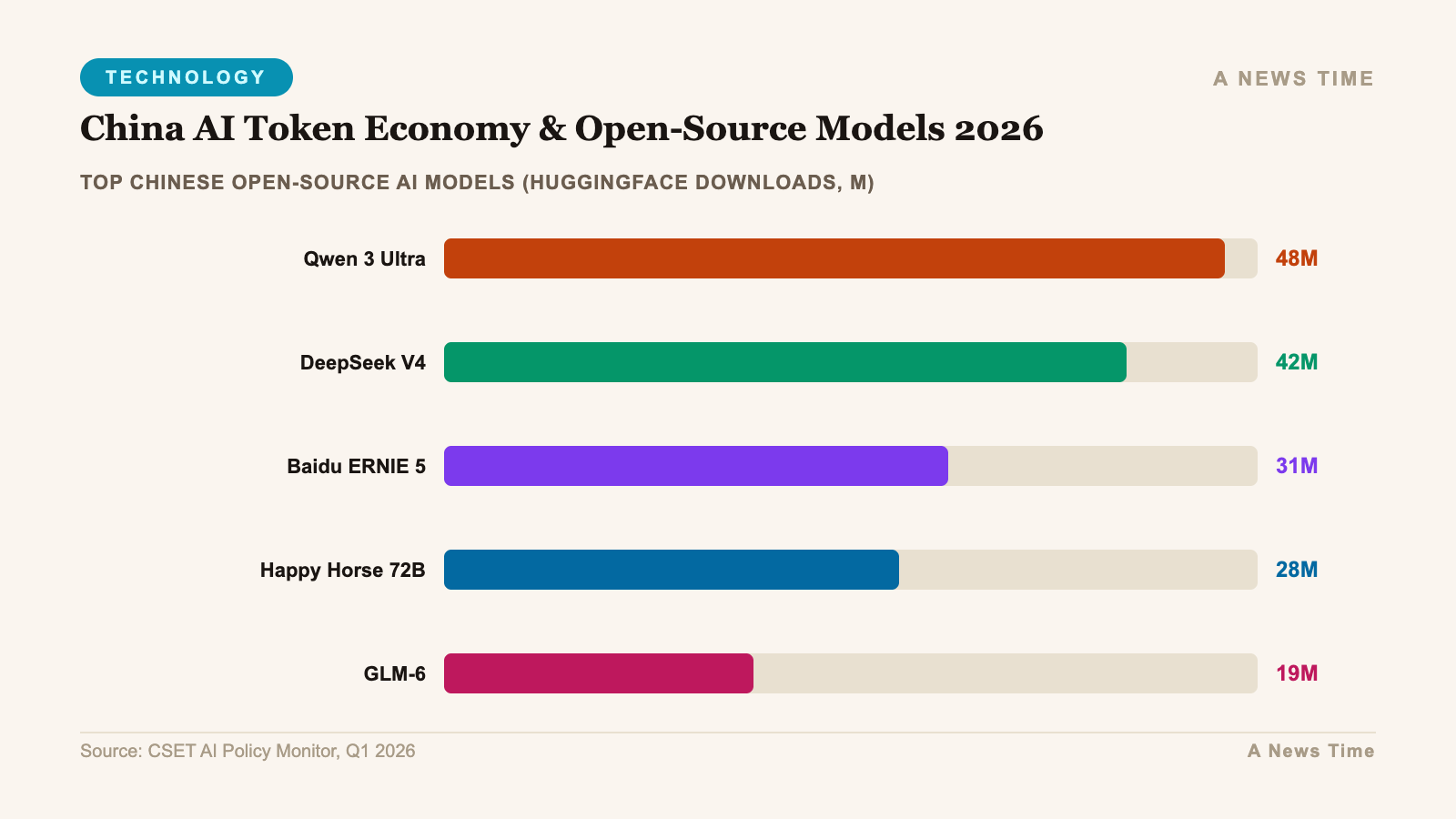

Alibaba has leaned hardest into open-source. Its Qwen model family is freely downloadable, finely tunable, and commercially permissive. That accessibility has driven adoption far outside China: Qwen has gained developers in Southeast Asia, the Middle East, and Western markets. Meta's most recent model, Muse Spark, was reportedly trained partly on Qwen outputs, a detail that received significant attention when it emerged in early April. The Alibaba Token Hub consolidation puts Qwen's development under the same roof as the company's foundational research, enterprise services, and consumer applications, creating a vertically integrated AI stack where open-source serves as the acquisition channel and proprietary services capture the revenue.

ByteDance has taken the opposite approach on models, keeping them largely proprietary, while competing on product design and consumer reach. Its Doubao chatbot reached 100 million daily active users over the Chinese New Year holiday in February 2026, making it China's most-used AI app by that metric. ByteDance's SeeDance video generation model held the top position on the Artificial Analysis text-to-video leaderboard until Alibaba's Happy Horse 1.0 displaced it in April. The company's advantage is its product and distribution infrastructure: TikTok and Douyin provide billions of user interactions that translate directly into training signal and product insight.

Tencent has been a step behind on model development but is catching up through platform leverage. Its March launch of ClawBot, integrated directly into WeChat, puts AI agent capabilities in front of more than one billion monthly active users without requiring them to download a new app. That distribution advantage is significant: while Alibaba and ByteDance compete on model quality, Tencent can win on ubiquity. A good-enough AI agent that is already inside the app everyone in China uses for payments, messaging, and social media has structural advantages that raw benchmark performance cannot overcome.

| Company | AI Strategy | Flagship Product | Key Metric |

|---|---|---|---|

| Alibaba | Open-source Qwen + Token Hub consolidation | Qwen models, Happy Horse video AI | 123B yuan capex in 2025 |

| ByteDance | Proprietary models + consumer product strength | Doubao chatbot, SeeDance video | 100M daily active users on Doubao |

| Tencent | Platform distribution via WeChat | ClawBot (WeChat-integrated) | 1B+ monthly active WeChat users |

The IPO Boom: Startups Going Public in Hong Kong

Hong Kong is experiencing its strongest IPO market in five years, driven by a wave of Chinese AI and technology startups taking the public route to liquidity. The companies going public include AI labs MiniMax and Zhipu AI, chip designer Biren, and humanoid robotics company Unitree, which has filed for a 4.2 billion yuan ($610 million) listing on Shanghai's STAR Market.

The financial details from the labs that have already listed are illuminating about the economics of the sector. MiniMax reported $79 million in 2025 revenue, up 159% year-over-year, with 70% of that coming from overseas markets. But it also posted an adjusted net loss of $250 million. Zhipu AI generated 724 million yuan ($104.8 million) in revenue, up 132%, while its total losses reached 4.7 billion yuan ($680 million), driven by research and development spending that jumped 45%.

Investors are apparently not deterred by these numbers. Zhipu AI's shares rose more than 570% from its IPO price; MiniMax climbed more than 470%, briefly exceeding Baidu's market cap. The valuation logic mirrors what drove American AI company valuations in 2025: the belief that frontier AI capabilities, once established, will translate into durable revenue streams that justify heavy upfront losses. Whether that thesis holds is the central unanswered question for the sector in both countries.

We believe that China is the big winner in this tech war for a number of reasons: valuation, wider adoption of AI, an advantage in power generation.

Mohit Kumar, Global Macro Strategist, Jefferies, speaking at Asia Forum in Hong Kong, March 2026

Moonshot AI, backed by Alibaba and HongShan and valued at $10 billion after a January 2026 funding round, is reportedly considering a Hong Kong IPO. Its Kimi K2.5 model attracted attention in April when Cursor, the vibe-coding startup, built its latest service on top of it, and co-founder Lee Robinson acknowledged it was "a miss to not mention the Kimi base…from the start."

Real-World Applications: Agents, Robots, and Short Dramas

The token economy framework is not just about chatbots and leaderboard rankings. China is seeing genuine adoption of AI across physical and creative industries in ways that Western markets have not yet matched at scale.

The short drama industry is the most vivid example. Chinese video platforms launched roughly 470 new dramas per day in January 2026, with AI tools cutting production costs from around 1 million yuan per drama to approximately 100,000 yuan, about 10% of conventional costs. The production window compressed from 15-30 days to under five. This is AI productivity gain at industrial scale: not a marginal improvement in how professionals work, but a structural reduction in the capital required to produce a category of content entirely.

AI agents are proliferating through a combination of corporate investment and government subsidy. The OpenClaw agent, Tencent's first major agentic product, attracted enough consumer interest that Tencent hosted workshops walking users through installation on personal devices. Local governments are amplifying adoption by offering subsidies to "one-person companies," solo entrepreneurs building agent-based businesses. The government is effectively seeding an ecosystem of small-scale AI businesses as a demand driver for the broader token economy.

In physical AI, China's robotics industry is advancing alongside its software capabilities. Unitree Robotics has achieved something rare in the humanoid robotics space: it makes money. The company posted an adjusted net profit of roughly 600 million yuan ($87 million), standing in sharp contrast to robotics peers in both China and the United States that are burning capital at scale. Other Chinese robotics startups, including Agibot and UBTech, are also active.

The autonomous vehicle sector shows a similar pattern of global ambition. Pony AI launched Europe's first commercial robotaxi service in Zagreb, Croatia in early April, in partnership with Uber and Croatian operator Verne. WeRide has launched fully commercial robotaxis in Dubai, also through an Uber partnership. China's autonomous vehicle companies are finding their first international deployments while their American counterparts are still navigating domestic regulatory environments.

The Export Controls Problem: What They Stop and What They Don't

U.S. export controls on advanced semiconductor technology remain the most significant structural constraint on Chinese AI development. The controls limit Chinese companies' ability to acquire Nvidia's H100 and H200 chips, the hardware that has powered most of the frontier model training at American AI labs over the past two years.

The impact is real. Chinese companies train models on Huawei's Ascend chips, which offer lower performance than Nvidia's current generation. They run some training workloads in overseas data centers. They access U.S. hardware through grey-market channels at significant premium. Alibaba's April 8 announcement of a data center built entirely on its own home-designed Zhenwu chips signals serious investment in chip sovereignty, but the company itself acknowledges that production yields and performance still trail the U.S. supply chain.

What the controls cannot stop is algorithmic progress. The advances in Chinese models over the past 18 months, from DeepSeek's V3 and R1 models that reset the efficiency conversation, to Qwen's global adoption, to Happy Horse's leaderboard win, reflect genuine research capability that does not simply scale with chip count. Better training algorithms, more efficient architectures, and more careful data curation can close capability gaps that raw compute cannot bridge.

The power generation advantage that Jefferies flagged may ultimately matter more than chip access. Goldman Sachs estimates China will have approximately 400 gigawatts of spare power capacity by 2030, roughly three times projected global data center demand. Energy is increasingly the binding constraint on AI infrastructure expansion, and China's aggressive investment in power generation and transmission capacity over the past decade has created an advantage that chip export controls cannot offset.

Related reading: How neuro-symbolic AI could cut energy use 100-fold, OpenAI's $852B valuation and what it means for the AI race.

The Monetization Question: Turning Tokens Into Profits

The biggest unresolved question in Chinese AI is the same one facing American AI companies: profitability. The capital expenditure numbers are staggering. Alibaba spent 123 billion yuan ($17 billion) on capex in 2025, contributing to a 66% plunge in net income. Tencent spent 79 billion yuan ($11.6 billion). ByteDance, as a private company, is under less shareholder pressure, but the Financial Times reported it expects to spend $23 billion on AI infrastructure this year alone.

For context, those are substantial numbers but still smaller than what American giants are committing. Alphabet spent $94 billion on capital expenditures in the most recent year; Meta spent $75 billion. Both plan to increase that spending in 2026.

Monetization pressure is already producing strategic shifts. Both Alibaba and Z.ai (Knowledge Atlas) have released their most recent models in closed formats initially, rather than open-sourcing from day one. Multiple Chinese AI companies, including Baidu and Zhipu AI, have raised prices for their models and cloud services. The open-source-everything strategy that defined the sector through 2025 is giving way to a more nuanced approach where open-source serves specific strategic purposes and commercial products command premium pricing where the market will bear it.

The exit ban on two Manus AI co-founders who reincorporated the company as a Singapore entity before Meta acquired it for roughly $2 billion illustrates the political dimensions of monetization strategy. Founders who want to capture Western capital or consumer markets face a structural tension with Beijing's expectation that Chinese AI assets should remain under Chinese ownership and control. That tension will not resolve easily as Chinese AI companies pursue global distribution.

Consumer Trust and Adoption: A Structural Advantage

One data point from China's AI landscape deserves more attention than it typically gets: consumer trust. An Edelman survey from October 2025 found that 87% of Chinese respondents trust AI, against 32% in the United States. That 55-point gap is not just a cultural curiosity. It is a structural market advantage.

High consumer trust enables faster adoption cycles, more willingness to use AI in sensitive contexts (healthcare, finance, personal advice), and less friction in deploying AI agents for tasks that American consumers would scrutinize or resist. The short drama production boom, the 100 million daily Doubao users, the government workshops on installing OpenClaw on personal devices: these are all expressions of a consumer base that treats AI as a tool rather than a threat.

The government's role in shaping that trust is significant. Beijing has been simultaneously enthusiastic about AI adoption and proactive about managing specific risks, warning against security vulnerabilities in OpenClaw-based agents and proposing regulations for AI companion apps. The regulatory posture is one of managed acceleration rather than precautionary restriction, which differs substantially from the European approach and partially from the American one.

What the Token Economy Means for the Global AI Race

China's AI industry in early 2026 is not winning on every dimension. Frontier model capabilities still lag Anthropic and OpenAI on many benchmarks. Chip access remains constrained. The venture capital ecosystem is thinner than Silicon Valley's. Some of the most commercially successful Chinese AI ventures have chosen to operate outside China to access global capital markets.

But the picture is more complicated than a simple ranking of who is ahead. China processes 140 trillion tokens daily. It has a government framework for measuring and growing that number. It has consumer adoption rates nearly three times the U.S. level. It has power generation capacity that will materially exceed global data center demand by 2030. And it has algorithmic researchers who have already demonstrated, with DeepSeek, Qwen, and now Happy Horse, that capability gaps can close faster than chip supply chain advantages would suggest.

The token economy framing is not just naming. It is the articulation of a development strategy: measure the thing you want to grow, build infrastructure around it, subsidize adoption, and let the competitive pressure of an enormous domestic market drive innovation. That strategy has worked for China in manufacturing, in renewable energy, and in electric vehicles. Whether it works in AI at the frontier, where algorithmic research and not just production efficiency determines outcomes, is the central question the next 18 months will answer.

For reference: Anthropic Mythos and AI's cybersecurity implications, Google Gemma 4's Apache 2.0 open-source strategy.