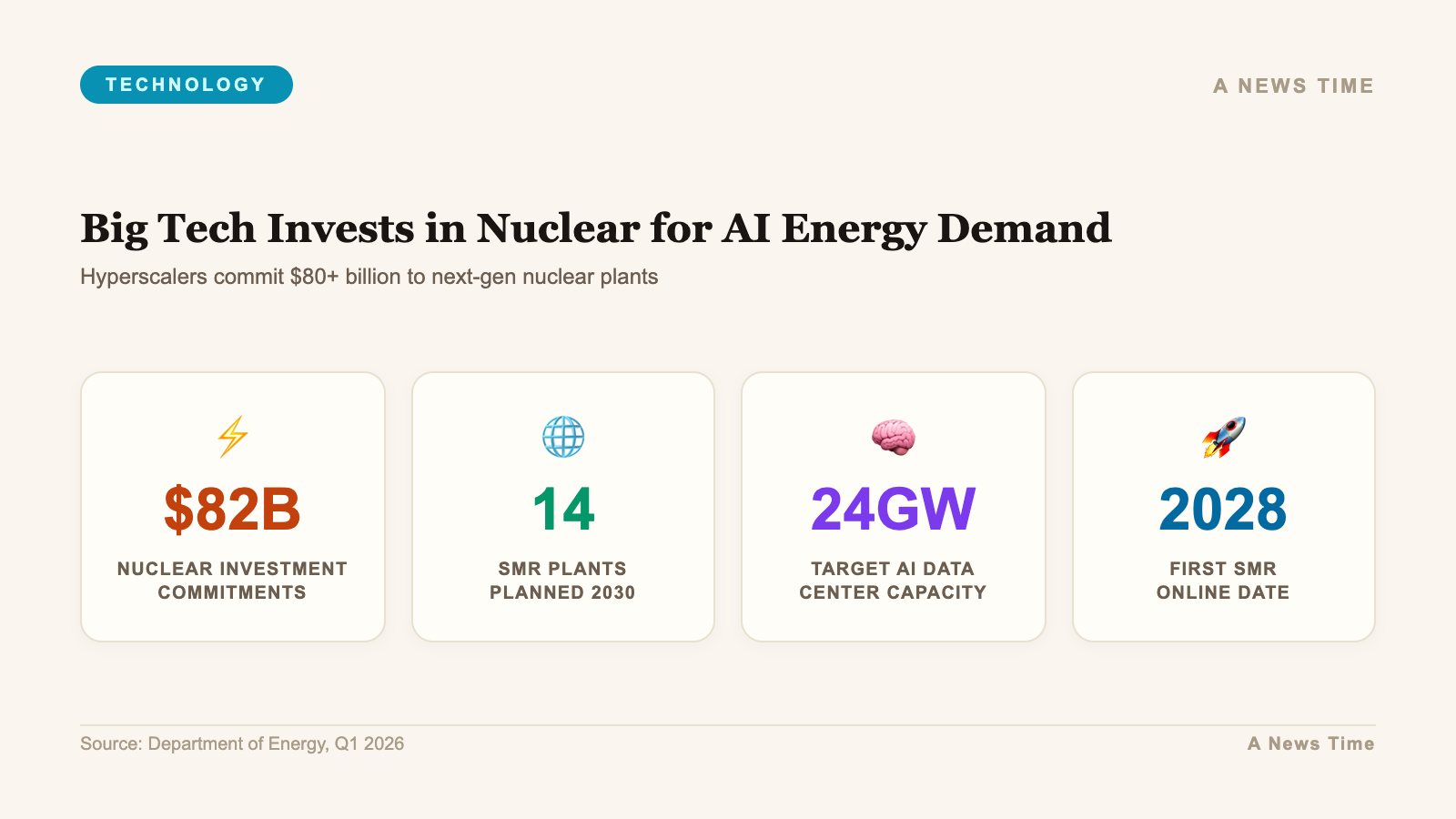

Big Tech's energy problem has become too large to solve with solar panels and wind contracts. The computational demands of training and running large language models are so substantial that the three largest AI infrastructure investors, Meta, Amazon, and Google, have all independently concluded that nuclear power is the only scalable source of firm, carbon-free electricity that can meet their needs over the next decade and a half. The deals signed in 2026 represent a fundamental shift in how the technology industry is thinking about energy, moving from purchasing electrons on the grid to funding the construction of power plants that exist specifically to meet corporate demand.

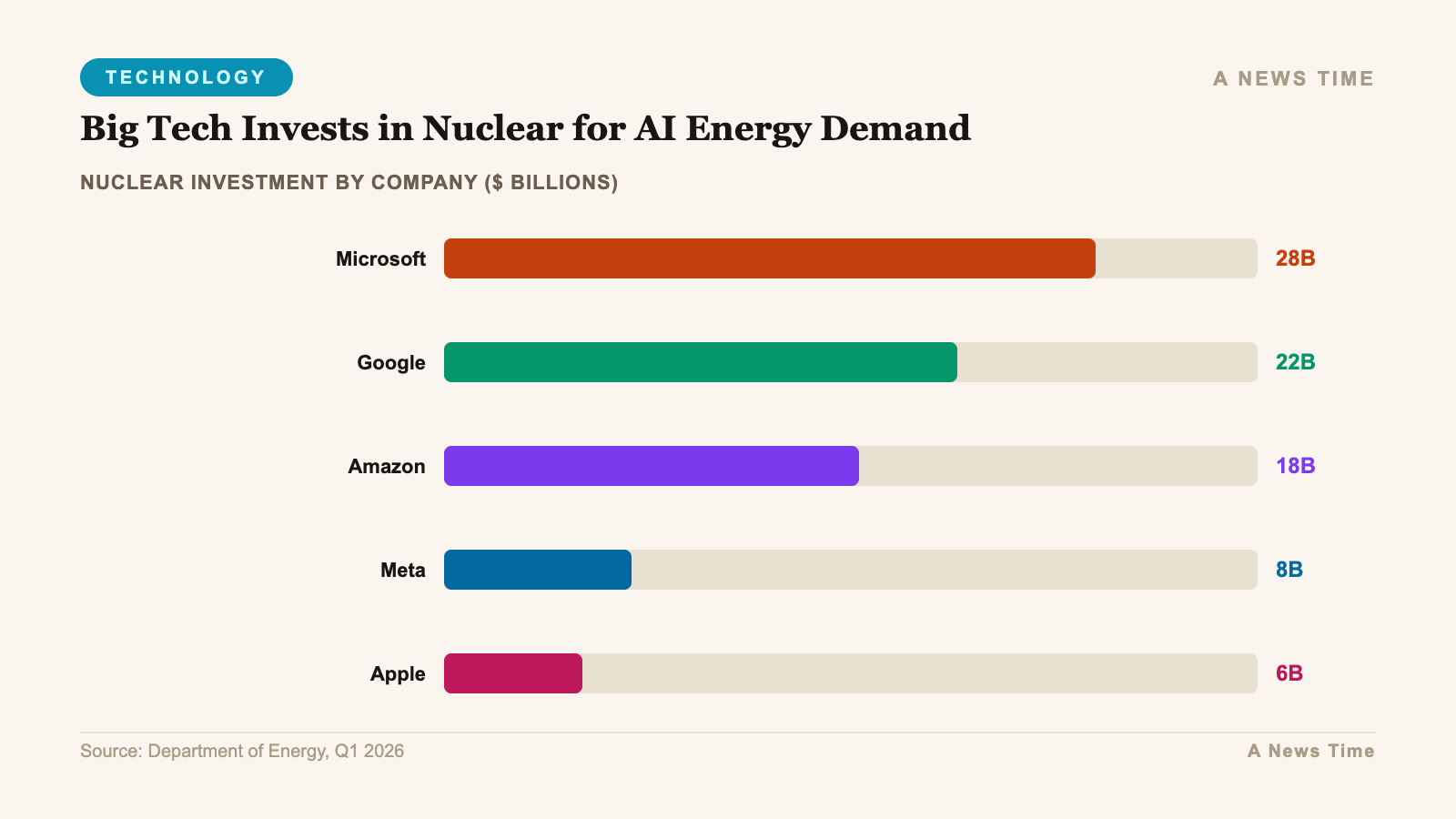

Meta announced agreements to fund two TerraPower nuclear reactor units with a combined capacity of 690 megawatts, alongside a separate deal with Oklo for a 1.2 gigawatt campus in Ohio. Amazon committed to co-development of 5 gigawatts of small modular reactors with X-energy, with capacity to come online through 2039. Google, through its partnership with Kairos Power, is targeting a first SMR unit by 2030. The scale of these commitments is significant. For context, one gigawatt of power generation capacity is roughly equivalent to the output of a large conventional power plant. Amazon's 5-gigawatt commitment alone represents substantial new generation capacity.

Why Nuclear: The AI Energy Problem in Numbers

The EIA projects that US electricity use will increase 1 percent in 2026 and 3 percent in 2027, a notable shift from the near-flat electricity consumption that characterized most of the 2010s. That increase is being driven primarily by data center growth, which in turn is being driven primarily by AI compute demand. Training runs for frontier models consume energy at a scale that would have been considered implausible a decade ago. Inference, the ongoing process of running models to serve user queries, scales with the user base and runs continuously. The combined effect is that large language model infrastructure represents a sustained, baseload electricity demand that grows as the models scale and the user base grows.

Solar and wind power address some of this demand but have a fundamental limitation: they are intermittent. A data center running AI inference cannot pause when the sun goes down or the wind drops. Batteries can buffer short-term fluctuations but are not economically viable for storing the quantities of energy needed to run a major data center complex through multi-day low-generation periods. Natural gas plants can provide firm power but produce carbon emissions that technology companies are committed to eliminating from their energy portfolios under various sustainability pledges. Nuclear power produces firm, dispatchable, carbon-free electricity continuously, which makes it the only currently available large-scale energy source that satisfies all three constraints simultaneously: reliable, clean, and scalable.

Meta's TerraPower and Oklo Deals: Two Bets on Different Technologies

Meta's dual commitment reflects a strategy of hedging across different nuclear technology approaches. TerraPower is developing a sodium-cooled fast reactor called the Natrium design, which uses molten salt as a thermal energy storage medium. The Natrium design is intended to pair well with variable renewable generation: the reactor runs continuously at full output, and excess energy goes into the molten salt storage system, which can then discharge electricity during periods of high demand or low renewable generation. For Meta's purposes, this means reliable baseload power with additional dispatch flexibility.

Oklo is pursuing a different approach with its Aurora compact fast reactor, a smaller design intended for industrial and commercial power customers. The 1.2 gigawatt Ohio campus commitment is substantial relative to Oklo's current stage of development. Oklo received its combined license application accepted by the NRC in 2020 and has been working through the regulatory approval process since. Meta's commitment provides the commercial backing that Oklo needs to accelerate deployment and gives Meta a potential near-campus power source rather than a remote generation facility connected via transmission infrastructure.

Oklo spokesperson Bonita Chester offered a calibrating note on the market dynamics: "demand alone is not the only factor." That observation points to the reality that nuclear power, even with committed corporate customers, still faces regulatory timelines, supply chain constraints, and skilled workforce requirements that create execution risk. The demand is clear. The question is whether the industrial infrastructure to meet that demand can be assembled quickly enough to satisfy AI data center timelines.

Amazon's 5 GW Commitment: The Largest Corporate Nuclear Deal in History

Amazon's agreement with X-energy to develop 5 gigawatts of SMR capacity by 2039 is the most ambitious corporate nuclear commitment made to date by any technology company. X-energy is developing the Xe-100 high-temperature gas-cooled reactor, a design that uses helium as a coolant and TRISO fuel particles that are designed to be inherently safe: the fuel cannot melt down in the way that the core of a conventional light-water reactor can. The Xe-100 is designed to produce approximately 80 megawatts per unit, meaning that 5 gigawatts would require approximately 62 individual reactor units.

The 2039 timeline is ambitious but somewhat less aggressive than it might appear, given that it spans 13 years from the commitment date. Amazon Web Services, the company's cloud infrastructure division, has been committing to renewable energy at scale for years through power purchase agreements with wind and solar farms. The nuclear deals represent a shift from purchasing power from existing or near-term renewable projects to funding the construction of new generation infrastructure that does not yet exist.

The strategic logic for Amazon is clear. AWS is the dominant cloud infrastructure provider globally, and AI workloads represent the fastest-growing segment of cloud demand. A commitment to 5 gigawatts of dedicated nuclear power is, in part, a competitive signal: Amazon is investing in the energy infrastructure necessary to maintain AWS's capacity advantage as AI workloads scale. A hyperscaler that runs short of power cannot serve customers. Given the capital constraints that most electricity utilities face, technology companies that can bring their own balance sheets to nuclear financing have a meaningful advantage in securing future capacity.

Google and Kairos Power: First Commercial SMR by 2030

Google's partnership with Kairos Power targets a first commercial SMR unit by 2030, an aggressive timeline for nuclear construction. Kairos Power is developing the KP-FHR, a fluoride salt-cooled high-temperature reactor that uses TRISO fuel, similar in that respect to X-energy's design, but uses molten fluoride salt as the coolant rather than helium. The Kairos design is intended to operate at higher temperatures than conventional light-water reactors, which opens potential applications for industrial process heat in addition to electricity generation.

Google's commitment to Kairos Power follows the company's announcement in 2023 that it had signed agreements for 500 megawatts of Kairos capacity. The updated 2026 commitment represents an expansion and acceleration of that earlier deal. Google has been explicit that it sees nuclear power as necessary to achieve its carbon commitments while meeting growing electricity demand from AI. The company's 2024 environmental report showed that its carbon emissions had increased substantially due to data center energy demand, a disclosure that undercut earlier claims about carbon-free operations and created pressure to find a credible path to genuine decarbonization at scale.

The 2030 timeline for a first Kairos unit implies that site selection, regulatory approval, construction, and commissioning all need to proceed on a schedule that has few precedents in recent US nuclear construction history. The last major US nuclear project to start fresh construction, the Vogtle expansion in Georgia, experienced years of delays and massive cost overruns. The difference that proponents of SMR technology assert is that factory fabrication, standardized design, and modular assembly fundamentally change the construction economics. That argument has not yet been proven at commercial scale in the United States.

The Financial Angle: Tech Balance Sheets Solving the Nuclear Capital Problem

Shioly Dong, an analyst at BMI/Fitch, identified what may be the most significant structural shift in these deals: technology companies bring "top-rated corporate balance sheets" to nuclear financing. Traditional nuclear construction has been plagued by cost overruns that stretched capital requirements far beyond original estimates, deterred private investment, and in several cases bankrupted utilities that attempted construction. The companies that failed were utilities with regulated rate bases and limited balance sheet flexibility.

Meta, Amazon, and Google each have balance sheets characterized by enormous cash reserves, investment-grade credit ratings that are among the highest in the corporate universe, and the ability to absorb cost overruns that would be catastrophic for a regulated utility. Tess Carter at Rhodium Group noted that "banks are getting excited and interested in deal-making" around these corporate nuclear commitments, reflecting the financial sector's recognition that technology company backing changes the risk profile of nuclear projects in a fundamental way.

Gabelli Funds portfolio manager Tim Winter highlighted Oklo and NuScale as the companies to watch in the SMR space, reflecting the investment community's growing attention to how technology company demand translates into equity value for nuclear developers. NuScale had a setback when its first commercial project was cancelled in 2023 due to cost escalation, but the broader SMR sector has continued to attract both investment and regulatory attention. The Department of Energy's Loan Programs Office has been actively providing financing support for advanced nuclear projects, recognizing that federal backing is necessary to bridge the gap between project commitment and project operation.

The Workforce and Supply Chain Chokepoints

Technology company commitment and financial backing can solve the capital availability problem. They cannot, by themselves, solve the skilled workforce shortage or the supply chain constraints that represent the other major bottlenecks for rapid nuclear deployment. Oklo's Bonita Chester was pointing to exactly these constraints when she noted that demand alone is not the only factor.

Nuclear construction requires a specialized workforce that was substantially reduced during the decades of minimal new construction in the United States following the Three Mile Island and Chernobyl incidents in the 1970s and 1980s. The workers who built the most recent generation of US reactors, the Vogtle units and the Summer units in South Carolina (the latter cancelled mid-construction in 2017), are approaching or past retirement age. Training a new generation of nuclear construction workers, nuclear operators, and nuclear engineers takes years. Reactor construction programs that begin in 2026 will compete for the same limited pool of qualified workers as every other program that began in the same period.

The nuclear supply chain faces similar constraints. Key components, including reactor pressure vessels, steam generators, and specialized control systems, are manufactured by a limited number of suppliers globally. A surge in demand from SMR projects across multiple countries simultaneously strains that supply chain, with the predictable effect of extending lead times and potentially increasing component costs. The factory fabrication model that SMR developers are promoting is partly a response to this supply chain constraint: by manufacturing standardized modules in dedicated factories, developers aim to build sufficient production volume to justify supply chain investment and training of skilled assembly workers.

What This Means for the Energy Transition Broadly

The technology sector's pivot to nuclear power has implications that extend well beyond the data center industry. Large corporate offtake agreements that provide guaranteed revenue streams are exactly what capital-intensive infrastructure projects need to attract private financing. By committing to purchase large quantities of nuclear power over long contract periods, Meta, Amazon, and Google are providing the demand-side certainty that makes nuclear project financing viable in a way that merchant power market pricing has rarely achieved.

This dynamic has the potential to accelerate nuclear deployment broadly. If technology companies are willing to sign long-term power purchase agreements for nuclear energy at prices sufficient to support project financing, utilities and independent power producers that have been hesitant to pursue nuclear development due to financing risk may reconsider. The technology sector is, in effect, using its scale and balance sheet strength to create a market for nuclear power where none existed before.

The broader energy transition implication is that nuclear power, which had been in slow decline as a share of global electricity generation for decades, may be entering a period of genuine revival. Several EU member states have recently reversed course on nuclear phase-outs. Japan is restarting reactors that have been idle since Fukushima. The United Kingdom is pursuing new large reactor construction at Sizewell C. South Korea, which has one of the world's most efficient nuclear construction industries, is accelerating its domestic program and competing for export contracts. The technology sector's commitment to nuclear adds corporate demand to a picture that was already shifting in nuclear's direction on policy grounds.

For related coverage, see our reporting on Big Tech AI infrastructure spending under investor scrutiny, Nvidia's Vera Rubin and trillion-dollar chip backlog, and how AI is reshaping cybersecurity defense.

Sources

- Reuters: Big Tech signs nuclear power deals to meet AI energy demands (April 10, 2026)

- Axios: Meta funds TerraPower and Oklo; Amazon commits 5 GW with X-energy (April 10, 2026)

- Bloomberg: Google, Meta, Amazon sign nuclear deals as AI power demand surges (April 10, 2026)

- US Energy Information Administration: Short-Term Energy Outlook, Electricity Consumption Projections (2026)