STMicroelectronics NYSE: STM reported first-quarter 2026 financial results on . Net revenues for the quarter were $3.10 billion on a U.S. GAAP basis. Gross margin was 33.8 percent. Operating income was $70 million. The EPS print missed the Wall Street consensus. The stock jumped roughly 6 percent in Thursday premarket trading anyway, as the company's Q2 revenue outlook beat analyst expectations and management explicitly guided AI data-center revenue above $500 million for 2026.

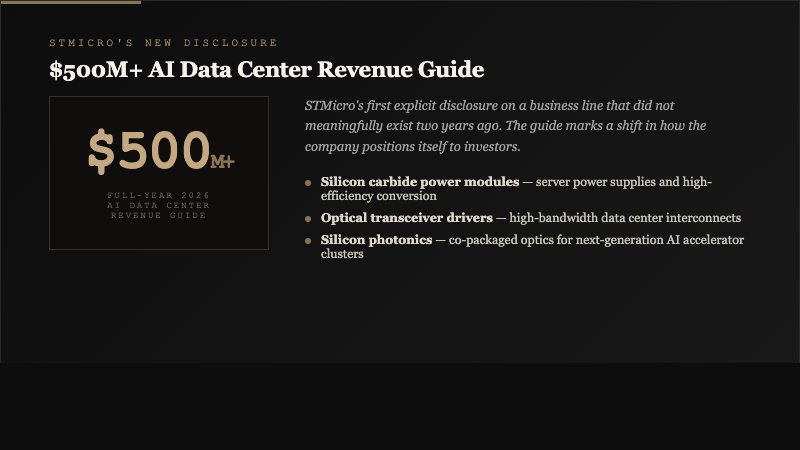

The divergence between the headline EPS miss and the share reaction is the story. Semiconductor investors in 2026 are not primarily pricing quarterly earnings volatility. They are pricing the trajectory of AI infrastructure spending and which chipmakers are capturing it. STMicro's AI data-center guidance, at more than $500 million for the year, is the company's first explicit disclosure of a business line that did not meaningfully exist two years ago.

The Actual Numbers

The Q1 2026 print breaks down as follows. Net revenues of $3.10 billion were down year over year from Q1 2025 as the automotive and industrial end markets worked through inventory corrections that have been running across the analog semiconductor sector for the past four quarters. Gross margin at 33.8 percent compressed from prior-year levels on the same mix pressure. Operating income of $70 million reflects the margin compression plus elevated research and development spending as the company extends its capacity footprint.

| Metric | Q1 2026 | Context |

|---|---|---|

| Net revenues (U.S. GAAP) | $3.10 billion | Down year over year on cyclical corrections |

| Gross margin | 33.8% | Compressed from prior-year levels |

| Operating income | $70 million | Impacted by elevated R&D |

| EPS | Missed analyst consensus | Shares still jumped on Q2 outlook beat |

| AI data-center guidance | >$500 million for 2026 | New disclosure, central to investor reaction |

| Premarket stock reaction | ~+6% | Q2 outlook beat estimates |

The Q2 outlook is where STMicro's disclosure did the real work. Management guided revenue above the analyst consensus range, signaling that the inventory correction in the broader analog semiconductor market is moving through its bottom and that orders are firming. That guidance is what moved the stock in premarket trading, not the Q1 print itself.

The AI Data Center Disclosure

The $500 million-plus AI data center revenue guide is the most commercially significant detail in the release. STMicro has historically been known for automotive analog chips, microcontrollers, power management components, and industrial sensors. The AI data center exposure is relatively recent and, until this release, unquantified in the company's public disclosures.

The specific products driving AI data-center revenue at STMicro include silicon carbide power modules used in high-efficiency server power supplies, optical transceiver drivers used in high-bandwidth interconnects, and a growing portfolio of silicon photonics components tied to the co-packaged optics transition that hyperscalers are pushing. None of those products is the marquee AI chip in a conventional sense. All of them are critical enabling technology for the AI accelerator ecosystem that NVIDIA, AMD, and the custom silicon designs from Google, Amazon, and Microsoft depend on.

"STMicro sees AI data-center revenue above $500M in 2026."

Stock Titan earnings coverage, April 22, 2026

The Automotive Drag

STMicro's primary end market remains automotive semiconductors, and that market has been going through an uneven recovery. Auto OEMs in the West have pulled back their EV production timelines. European automakers in particular have drawn down inventory aggressively over the past year, which compresses order flow for the Tier 1 component suppliers that feed them. Chinese EV manufacturers have been the brighter spot, but pricing in China is tight and margins pass through more slowly to suppliers.

The combination is that STMicro's automotive segment is no longer growing at the mid-teen percentages that characterized 2022 and 2023, when the industry was still working through pandemic-era chip shortages. The segment is more or less flat in 2026, which drags total company revenue. That drag is part of why the Q1 top line was down year over year even as the AI exposure ramped.

How STMicro Compares to Peers

The Q1 release lands inside a full week of semiconductor earnings that have produced a consistent narrative split. Companies with direct AI infrastructure exposure are guiding upward and beating expectations. Companies with primarily automotive or industrial analog exposure are guiding cautiously and posting year-over-year declines. Texas Instruments, NXP Semiconductors, and Infineon have all landed on the cautious side of that split in recent quarters. Broadcom, Marvell, and TSMC have landed on the upbeat side.

STMicro is trying to straddle the divide. Its automotive exposure looks like TI and Infineon. Its AI data-center ramp looks like a scaled-down version of Broadcom. The investor question is whether the AI exposure is growing fast enough to offset the cyclical automotive weakness, and the Q2 outlook beat plus the $500 million-plus AI guide is STMicro management's first clear attempt to argue that it is.

"Shares of STMicroelectronics jumped about 6% premarket on Thursday after the second quarter revenue outlook surpassed estimates."

Seeking Alpha coverage, April 23, 2026

The Strategic Takeaway

STMicro's Q1 print is a useful data point for a broader industry shift that has been building for four quarters. The semiconductor companies that matter to capital markets are no longer the ones with the highest growth in traditional end markets. They are the ones with clear exposure to AI infrastructure capital spending, either directly through accelerator silicon or indirectly through the enabling components that accelerators depend on. STMicro is repositioning into the second of those categories faster than its historical business mix would suggest.

The execution risk is real. Silicon carbide is a competitive market with Chinese entrants driving pricing down. Silicon photonics is technologically differentiated but not yet at scale. The $500 million-plus AI data-center revenue number, while material, is less than 5 percent of STMicro's total company revenue. The narrative shift is real. The financial shift is just beginning.

What to Watch Going Forward

Two specific signals will determine whether STMicro's AI data-center disclosure represents a durable new revenue line or a one-time bump. The first is whether Q2 and Q3 releases see the AI guidance raised or narrowed. A raise indicates real order flow acceleration. A narrow or flat update indicates the $500 million-plus figure was the ceiling rather than the floor.

The second is the automotive recovery timing. If European and U.S. EV production rebounds in the second half of 2026, STMicro's historical strength will reassert itself and the AI exposure becomes an accelerant rather than a lifeline. If the automotive pullback extends into 2027, the AI line has to carry more weight than its current size supports.

For related coverage, see our reporting on TSMC's A13 node unveiled at the North America Technology Symposium, on NVIDIA's Vera Rubin roadmap and trillion-dollar backlog, and on Big Tech AI spending scrutiny entering the 2026 earnings cycle.

Sources

- STMicroelectronics Reports Q1 2026 Financial Results - GlobeNewswire

- STMicro sees AI data-center revenue above $500M in 2026 - Stock Titan

- STMicroelectronics rises after Q1 revenue soars, Q2 sales outlook beat - Seeking Alpha

- STMicroelectronics Reports Q1 2026 Results: Full Earnings Call Transcript - Benzinga