The USS Spruance, a US Navy guided-missile destroyer, fired several rounds into the engine room of the Iranian-flagged cargo ship Touska in the Gulf of Oman on , after the 900-foot vessel spent six hours refusing to comply with a US maritime blockade. US Marines took custody of the ship later Sunday, the Pentagon and President Donald Trump said in separate statements. Within hours, Iran's joint military command vowed retaliation, Tehran confirmed the Strait of Hormuz would be shut for the second time since the US-Israeli war with Iran began on , and Iranian state media reported that a planned second round of face-to-face peace talks in Islamabad on would proceed without an Iranian delegation.

For energy markets, the sequence matters more than any single event inside it. A US Navy seizure of an Iranian-flagged merchant vessel combined with a reimposed chokepoint closure and a breakdown of the week's most important diplomatic track is the type of compounding disruption that oil traders price into forward curves immediately, not gradually.

What Happened in the Gulf of Oman

The Touska is a cargo vessel flagged to Iran and already under US Treasury sanctions for what Trump described as a "prior history of illegal activity." According to a US Central Command statement, the ship "failed to comply to repeated commands" over a six-hour period before the Spruance engaged its engine room to halt forward motion. The Pentagon described the vessel as nearly as heavy as an aircraft carrier. No casualty figures have been released by either side.

Trump announced the seizure on Truth Social Sunday evening, writing that US forces "blew a hole" in the Touska's engine room after repeated warnings and that Marines had "full custody of the ship." Iran's joint military command responded early on by calling the operation "piracy and armed aggression by the US military" and pledging that Iranian armed forces would "soon respond and retaliate."

Hours later, the Khatam al-Anbiya headquarters, Iran's joint operational command, issued a second statement saying Iranian forces had refrained from immediate action "due to the presence of some families of its crew" and that "necessary action will be taken after ensuring the safety of the families and crew of the ship." The United States has not confirmed the claim that crew families were aboard.

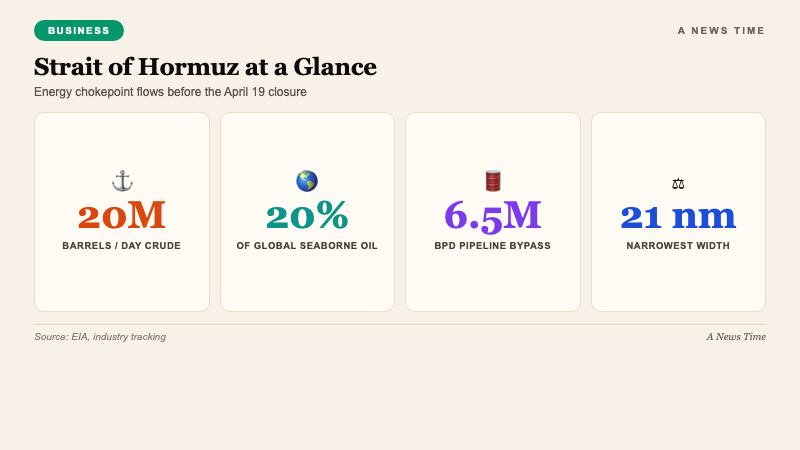

Why the Strait of Hormuz Matters to Oil Markets

The Strait of Hormuz is the single most important maritime chokepoint in global energy flows. The US Energy Information Administration has historically tracked between 17 and 21 million barrels per day of crude oil and condensate moving through the strait, depending on OPEC+ production levels. That is roughly 20% of total global petroleum liquids trade. For refined products and liquefied natural gas, the share is lower but still material.

| Metric | Value | Context |

|---|---|---|

| Crude and condensate flow (pre-war avg.) | ~20M barrels/day | EIA 2024 estimate |

| Share of global seaborne oil | ~20% | Largest single chokepoint |

| LNG flow (pre-war) | ~20% of global LNG trade | Primarily Qatar exports |

| Narrowest width | 21 nautical miles | Between Oman and Iran |

| Alternative pipeline capacity | ~6.5M barrels/day | Saudi East-West, UAE Fujairah |

A closure does not physically block every cargo. Some flows reroute through the Saudi East-West pipeline to the Red Sea or through UAE pipeline capacity to Fujairah, bypassing the strait entirely. But the pipeline alternatives have total capacity of roughly 6.5 million barrels per day, meaning any sustained closure still strands a majority of the regular volume or forces it through premium-risk insured shipping channels.

The first Hormuz closure of this war, declared by Iran in the second week of the conflict, was reopened in April after behind-the-scenes Gulf diplomacy and a brief US-Iran ceasefire. That reopening drove a relief rally in equities and a 12% single-session decline in Brent crude. The second closure removes that relief.

Oil Price Mechanics Heading Into the Week

Brent crude closed at roughly $94 per barrel on , the last full trading session before the seizure, down from wartime highs above $110 earlier in the conflict. The decline reflected the combination of the strait reopening, the tentative ceasefire, and OECD demand weakness flagged by the OECD's Iran-war growth downgrade in March.

The fundamental pricing question for the week ahead is whether the Touska seizure represents a contained escalation or the start of a broader kinetic phase. An isolated boarding incident with no follow-on military exchange tends to add a $3 to $6 per barrel risk premium that decays over several sessions. A sustained closure with confirmed Iranian retaliation moves the premium into the $12 to $20 per barrel range and stays there until diplomatic channels reopen.

The pricing complication is that gasoline futures respond to crude with a lag and are already elevated. US retail gasoline averaged $3.98 per gallon through the AAA tracker in late March, up roughly 34% from the conflict start. A renewed crude spike would push retail gasoline into the $4.20 to $4.40 range by the first week of May on normal pass-through timing.

The Diplomatic Track Just Collapsed

Iranian Foreign Ministry spokesman Esmail Baqaei said on that Iran has "no plans" to participate in a second round of Pakistani-hosted peace talks with the United States. Baqaei called the ship seizure "aggression" and said Iranian authorities were investigating the incident. Iranian state news agency IRNA went further, stating that Iran rejected participation because of "Washington's excessive demands, unrealistic expectations, constant shifts in stance, repeated contradictions, and the ongoing naval blockade, which it considers a breach of the ceasefire."

"Iran will make the appropriate decision on continuing the path of negotiations by prioritizing national interests and concerns."

Esmail Baqaei, Iranian Foreign Ministry spokesman, weekly press briefing, April 20, 2026

The White House had publicly committed to sending a US delegation to Islamabad for the talks. Pakistani Prime Minister Shahbaz Sharif confirmed a 45-minute call with Iranian President Masud Pezeshkian in which he said he reiterated Pakistan's role in regional stability, but no readout indicated when a substantive second round might resume.

Tehran also announced the execution of two more Iranians on on espionage and "connections with Israel" charges, the latest in what Iranian rights groups have called a sharp rise in wartime executions.

Where the Risk Flows

The market sectors most exposed to a sustained Hormuz closure are predictable from prior shocks. Energy majors with upstream Gulf exposure, including ExxonMobil, Chevron, and TotalEnergies, tend to track the crude premium with some lag. Shipping insurers and tanker operators, including Frontline and Teekay Tankers, benefit from rising day rates when the war-risk insurance premium repricing forces owners to renegotiate charters.

Airlines and logistics-heavy industrials are on the other side. Jet fuel is priced off crude with a narrow spread, and sustained energy inflation compresses airline margins fastest. Wall Street strategists have already flagged the Iran war's energy channel as the single largest macro risk factor for 2026 equity returns.

Currency markets also respond. The dollar tends to strengthen on Gulf tail risk as US Treasuries absorb safe-haven flows, which layers an additional headwind onto emerging market equities and commodity-linked currencies. The Canadian dollar and Norwegian krone are the usual outperformers in oil-spike episodes because their home economies are net energy exporters.

What to Watch This Week

Three catalysts determine whether this incident prices as a one-week disruption or a multi-month regime shift.

- Iranian retaliation signal. The joint military command's "soon" is doing significant work. A token missile launch on uninhabited coastal targets prices differently than a strike on US naval assets or Gulf partner infrastructure.

- Diplomatic reset window. If Tehran and Washington reconvene talks in a neutral venue, likely Doha or Muscat, within 7 to 10 days, the market treats April 19 as a managed escalation. Beyond that window, the closure starts pricing like a structural shift.

- Shipping-insurance response. Lloyd's war-risk premiums for Gulf transits are the cleanest real-time gauge of perceived closure duration. A return to war-peak pricing within 72 hours is the leading indicator that bulk of oil freight is rerouting.

The Reuters report citing an unnamed senior Iranian official captured the underlying dynamic cleanly. The gaps on nuclear program constraints, the official said, "have not narrowed." A naval incident that was supposed to be a contained enforcement action has now been elevated into the opening argument of the next negotiating round. Whether that round happens at all is the question markets are pricing this week.

Frequently Asked Questions

Is the Strait of Hormuz fully closed right now?

Iran's joint military command declared the strait closed on April 20, 2026, following the US seizure of the Touska. Tehran has declared closures before without fully physically blocking traffic. Commercial vessels have been diverting or accepting higher war-risk insurance premiums during previous declared closures.

What percentage of global oil passes through the Strait of Hormuz?

The US Energy Information Administration has tracked roughly 20% of global seaborne petroleum liquids, or around 20 million barrels per day of crude and condensate, transiting the strait in recent years. The share is comparable for global LNG trade, primarily due to Qatari exports.

Can oil bypass the Strait of Hormuz?

Partially. The Saudi East-West pipeline to the Red Sea and the UAE Fujairah pipeline network provide combined capacity of roughly 6.5 million barrels per day, well below the daily volume that normally transits the strait. A sustained closure still leaves the majority of usual flow stranded or forced through premium-priced shipping routes.

How did oil and stocks react the last time Iran closed the strait?

During the first declared closure earlier in the conflict, Brent crude spiked above $110 per barrel intra-session. Equities fell sharply, with the S&P 500 entering correction territory. The reopening in April produced a 12% single-session decline in Brent and a significant equity relief rally, a move that is now being reversed by the new closure.

What happens if Iran-US talks don't restart?

An extended diplomatic gap raises the probability of a structural repricing in oil. Historically, Gulf conflict episodes that lasted beyond 30 days without negotiation embedded a $10 to $20 per barrel persistent risk premium, with downstream effects on gasoline, diesel, airline fuel, and global inflation expectations.

What Comes Next

The immediate question is whether Iran's retaliation arrives this week or is delayed into the talks window. The medium-term question is whether the Touska seizure gets folded into a broader diplomatic package or becomes the precipitating incident that hardens positions on both sides. The economic stakes are straightforward. A contained incident prices as one week of volatility. A structural shift prices as a full reset of the 2026 oil and inflation outlook.

Sources

- Iran Says It Didn't Act On Seized Ship To Protect Crew's Families - Radio Free Europe/Radio Liberty

- Distress call captures tanker under fire as Iran shuts Strait of Hormuz - Fox News

- Trump says US Navy fired on and seized an Iranian cargo vessel - Q2 News KTVQ

- World Oil Transit Chokepoints: Strait of Hormuz - US Energy Information Administration