Tesla is scheduled to report its first-quarter 2026 earnings after the closing bell on Wednesday, April 22, 2026, and the setup heading into the print is the most hostile the company has faced in more than two years. Auto demand is sliding, the federal electric vehicle tax credit is gone, and California, the single largest EV market in the United States, just posted a quarter of registrations that can only be described as a collapse. The stock has shed roughly 20 percent since January, and the narrative that has kept Tesla's valuation afloat, the idea that it is no longer a car company but an artificial intelligence and robotics platform, is about to meet the same hard accounting reality it has avoided for a year.

The math is not complicated. Tesla registered 31,958 vehicles in California during Q1 2026, down from 42,211 in the same period a year earlier, according to data from the California New Car Dealers Association's Q1 2026 Auto Outlook report. That is a decline of 10,253 units, or 24.3 percent, in a quarter when the prior-year comparison was already depressed by the Model Y changeover. Tesla's California market share fell from 9.2 percent to 7.7 percent. On a state-by-state basis this matters enormously: California accounted for 29.6 percent of all US zero-emission vehicle registrations last year, so softness in Sacramento showrooms and San Jose parking lots reads through to the consolidated financials in a way that softness in most other regions does not.

Automotive Gross Margins Become the Make-or-Break Metric

When Tesla reports Wednesday, the single line item that will decide whether the stock opens up or down on Thursday morning is automotive gross margin excluding regulatory credits. Analysts have tightened their expectations around a range of 17 to 18 percent, down from the roughly 20 percent Tesla delivered in earlier quarters of 2024 and a far cry from the 30-plus percent margins the company posted at the height of 2022. Any print below 15 percent, particularly without a credible recovery roadmap, would represent a structural problem that the AI story cannot paper over.

That concern is why Zain Vawda, writing for MarketPulse by OANDA Group, flagged gross margin as "make or break" in his Q1 preview. "Automotive gross margins are pivotal," Vawda wrote in an April 21 note. "A drop toward 15 percent without recovery plans could pressure the stock, while margins above 17 to 18 percent would reassure growth investors." The pressure is coming from two directions at once. Average transaction prices across the Tesla lineup have come down as the company has used incentives and financing promotions to move inventory after the $7,500 federal tax credit expired on September 30, 2025. At the same time, tariff-affected battery pack costs have climbed back above $155 per kilowatt-hour after briefly touching $139 earlier in the decade, according to Bloomberg New Energy Finance estimates.

"The shift is unmistakable. Hybrids now exceed ZEVs in California's market share, and gas-powered vehicles have climbed back to 61.1 percent of registrations, up from 54 percent in 2025. That is what happens when you remove the single most effective policy tool for EV adoption."

Fred Lambert, Editor in Chief, Electrek

The combination squeezes Tesla from both sides of its income statement. Lower prices per car meet higher costs per car, and the automotive gross margin line is where the collision shows up. Elon Musk has argued publicly that volume and scale will absorb the impact, but the Q1 delivery numbers already released, which came in below most sell-side estimates, suggest volume is not cooperating.

The $20 Billion AI CapEx Question

The bigger story for investors, and the one Musk will be asked about repeatedly on the earnings call, is how Tesla plans to spend its capital in 2026. Internal guidance filed with the Securities and Exchange Commission and reiterated on prior earnings calls points to a capital expenditure program that will exceed $20 billion for the full year. That is more than double Tesla's CapEx in 2022 and roughly in line with what Meta Platforms and Alphabet are each spending on AI infrastructure.

The $20 billion is not going into new gigafactories for cars. It is going into three AI-related pillars that Tesla has tried to reposition as the real business. The first is Full Self-Driving software, including the compute clusters needed to train FSD v14 and beyond. The second is the Cybercab and the broader Robotaxi commercial network, which Tesla has promised will launch in limited form in Austin and expand from there. The third is Optimus, the humanoid robot program, together with the Dojo supercomputer Tesla uses to train it.

| Metric | Bull Case | Bear Case | Consensus Range |

|---|---|---|---|

| Automotive gross margin (ex. credits) | >18% | <15% | 17-18% |

| Q1 deliveries (vs. est.) | Beat by 3%+ | Miss by 5%+ | Missed estimates |

| 2026 CapEx guidance | $20B confirmed, AI-focused | Raised to $25B+ | $20B+ |

| Robotaxi commercial roadmap | Paying rides in Austin | Timeline pushed to 2027 | Limited launch timeline |

| FSD v14 global expansion | EU/China approval dates | No new markets named | Netherlands approval in hand |

| Energy storage gross margin | >25% | Single digits | High teens to low 20s |

The credibility problem is that Musk has been promising a commercial robotaxi network since 2019, and the company has repeatedly pushed timelines. What makes Q1 2026 different is that Tesla has actually moved metal on its Cybercab production line in Austin, following the launch reported in early April, and has secured regulatory approval for FSD supervised use in the Netherlands, its first European market. Those are tangible milestones, not slides.

Whether they are enough to justify a valuation that trades like a software business while the underlying car business shrinks is a separate question. Gene Munster of Deepwater Asset Management has been among the more measured Tesla bulls, arguing that the market is giving the company a roughly two-year window to prove out robotaxi economics before it has to revert to being valued like an automaker. That window, by most bull-case math, effectively closes in 2027.

California as Canary: The Federal Tax Credit Aftermath

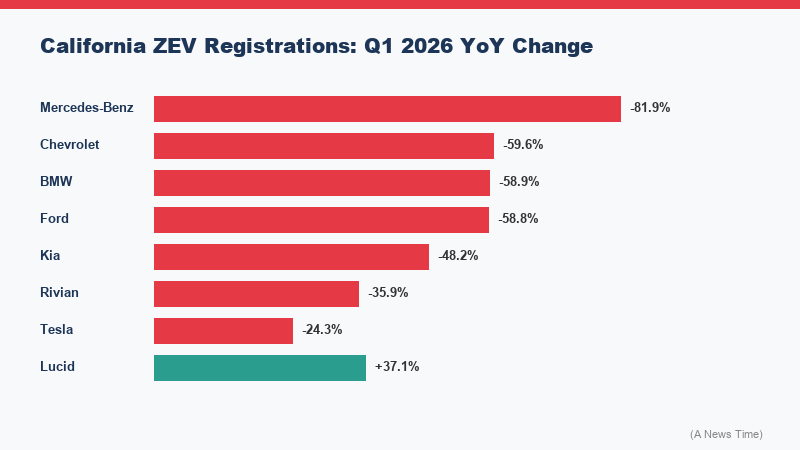

The California data released on April 21 is important for Tesla specifically, but it is more important as a leading indicator of what the national picture looks like after the $7,500 federal EV tax credit expired. Total zero-emission vehicle registrations in the state fell 40.2 percent year over year in Q1 2026, from 95,520 units to 57,111. That is not a soft quarter. That is a structural reset.

The brand-level carnage was unusually broad. Mercedes-Benz ZEV registrations in California collapsed 81.9 percent. Chevrolet, which had been building momentum with the Equinox EV, dropped 59.6 percent. BMW fell 58.9 percent, Ford 58.8 percent, Kia 48.2 percent, and Rivian 35.9 percent. Hyundai, which was arguably the most credible Tesla alternative through 2025, still posted a 30.4 percent decline in ZEV registrations. Meanwhile, hybrids surged to 20.9 percent of California's market, now outselling pure EVs in the state, and gas-powered vehicles climbed back to 61.1 percent of registrations from 54 percent the year prior.

Tesla's relative performance is the one silver lining, and it is a strange one. Tesla's share of the ZEV market in California actually rose from 44.2 percent to 56.0 percent, not because Tesla grew, but because every other EV brand shrank faster. That is the definition of gaining share of a shrinking pie. From an industry-structure perspective it validates Tesla's pricing power and brand moat. From a total-addressable-market perspective it is exactly the condition that makes the AI and robotaxi pivot necessary in the first place.

The federal policy reversal was not the only factor. A recent analysis by Cox Automotive estimated that national new EV sales dropped 28 percent in Q1 2026, with the decline concentrated in higher-priced segments. Used EV sales, by contrast, are up sharply, as consumers who still want to go electric are gravitating toward two and three year old inventory that has absorbed the depreciation shock. That is a reasonable market response, but it does not help Tesla's new-vehicle margin mix.

What a Good Night Looks Like for Tesla

For the stock to work on Thursday, Tesla needs to accomplish four things on the Wednesday call. First, automotive gross margin excluding regulatory credits needs to print at or above 17 percent, with management offering a credible path to margin stability rather than further compression. Second, Musk needs to confirm, not just reiterate, the $20 billion CapEx envelope and explain what fraction flows into FSD compute versus Cybercab infrastructure versus Optimus. Third, the company needs to give a concrete date for commercial paying robotaxi rides in Austin and the next two expansion markets, with revenue guidance investors can actually model. Fourth, energy storage gross margin, which has been Tesla's quiet high-margin business, needs to remain in the high teens or low 20s at minimum.

Anything materially weaker than that and the $490 to $500 technical resistance level the stock has been flirting with since March becomes a ceiling rather than a target. Anything stronger, particularly a hard date for commercial robotaxi monetization, and the AI narrative gets another six months of runway. Wall Street consensus, pulled from the sell-side previews circulated ahead of the print, is cautious but not catastrophic. The downside skew in options pricing suggests traders are positioned for volatility either way.

For related coverage on the automotive downturn, see our reporting on the $70 billion in EV program writedowns that have hit the industry and our analysis of how rising gas prices have reshaped Tesla's Q1 demand picture. On the AI side, our recent look at how banks are deploying agentic AI offers a useful contrast to Tesla's all-in bet on autonomy as the next revenue engine.

What to Watch After the Bell

The Tesla earnings call starts shortly after the SEC 8-K filing drops, typically around 4:30 pm Eastern. The most closely watched exchanges will come during the Q&A, particularly when sell-side analysts push Musk for specifics on Cybercab commercialization and when 2026 delivery guidance gets revised, if it does at all. Tesla has a history of declining to reaffirm or walk back prior full-year forecasts on Q1 calls, which itself becomes a signal. Silence on 2026 deliveries would likely be read as a concession that the current run rate cannot hit prior targets.

Investors looking for the raw data before the call should watch the California Q1 report directly from the California New Car Dealers Association, as well as the Q1 10-Q when Tesla files it in the days following the earnings release. The 10-Q will include regional revenue breakdowns, capital expenditure by category, and cash flow detail that the press release and slides will gloss over. That is where the real story, or the real absence of one, will show up.

Frequently Asked Questions

When does Tesla report Q1 2026 earnings?

Tesla is scheduled to report first-quarter 2026 earnings after the closing bell on Wednesday, April 22, 2026. The company's earnings call typically begins about 30 minutes after the press release and 8-K filing.

What is the most important metric in Tesla's Q1 2026 report?

Automotive gross margin excluding regulatory credits. Consensus estimates cluster around 17 to 18 percent. A print below 15 percent without a recovery plan would likely pressure the stock, while a result above 18 percent would reassure bulls that pricing power is holding.

Why did Tesla's California sales fall 24 percent?

Tesla registered 31,958 vehicles in California in Q1 2026, down from 42,211 in Q1 2025. The primary cause was the expiration of the $7,500 federal EV tax credit on September 30, 2025, which removed the most effective subsidy for EV adoption. Tesla's decline was smaller than most other EV brands, which saw 30 to 80 percent drops.

What is Tesla's projected 2026 capital expenditure?

Tesla has guided to capital expenditure exceeding $20 billion in 2026, flowing into three pillars: Full Self-Driving compute infrastructure, the Cybercab and Robotaxi commercial network, and the Optimus humanoid robot program along with the Dojo supercomputer.

Is Tesla still primarily a car company?

Financially, yes. The vast majority of Tesla's revenue still comes from vehicle sales and related services. The valuation, however, prices Tesla as a future software and AI platform company, which is why the Q1 call will hinge on whether management can provide a concrete monetization timeline for robotaxi and FSD.

Sources

- Tesla Q1 Earnings Preview: Is AI Powerhouse Narrative Enough To Offset Waning Auto Demand, Seeking Alpha

- Tesla's California sales crash 24 percent as state's EV market plunges to lowest since 2021, Electrek

- California New Car Dealers Association Q1 2026 Auto Outlook Report

- Should You Buy This Electric Vehicle Stock Before April 22?, The Motley Fool