The April 15 tax deadline has come and gone, and the consumer finance data that surrounds it tells a story worth reading carefully. Americans who filed on time are now sitting on either a refund check or a payment confirmation, both outcomes that trigger distinct financial decision points. Those who filed for an extension have six additional months of uncertainty. The savings and credit rate environment those decisions land in is one of the most consequential in years: high-yield savings accounts are paying above 4 percent at leading online banks, but credit card balances are carrying average APRs that have sat above 20 percent since the Federal Reserve's 2022-2023 rate hiking cycle and have not meaningfully declined despite two years of rate cuts. The gap between what savers earn and what borrowers pay has never been wider in the post-financial-crisis era.

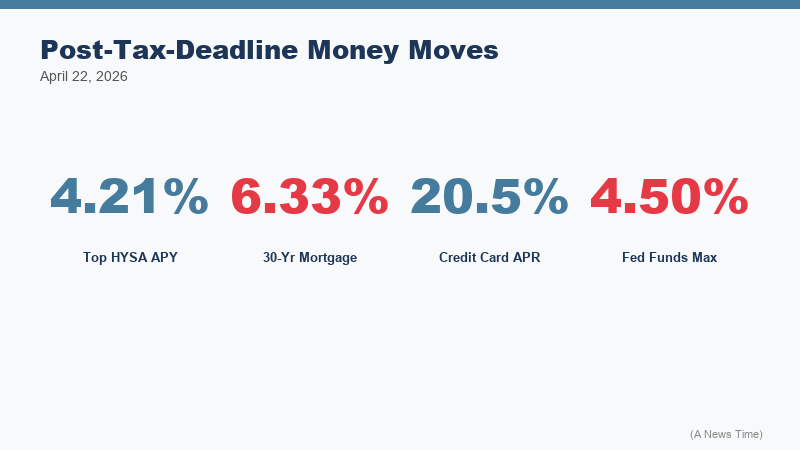

On , Bankrate published its updated ranking of the best high-yield savings accounts, placing the top rate at 4.21 percent APY. Fortune's rate tracker, which pulls from a broader universe of smaller online banks and credit unions, found rates up to 5.00 percent available for depositors willing to navigate minimum balance requirements and relationship conditions. The Federal Reserve, for its part, held the federal funds rate at its March meeting and the market is not pricing a meaningful probability of a cut before September. That rate hold is keeping savings rates elevated and borrowing costs high simultaneously, a condition that creates clear winners and losers depending on whether a household's primary financial need is to save or to borrow.

Where Savings Rates Stand: The Full Rate Map

The savings rate landscape in breaks into three tiers. The top tier consists of online-only institutions that compete aggressively for deposits through rate: Vio Bank is offering 4.03 percent APY with a $100 minimum, LendingClub at 4.00 percent with no minimum, and Bread Financial and similar institutions clustered in the 3.90 to 4.10 percent range. At the very top, according to Fortune's tracker, some institutions are offering promotional rates up to 5.00 percent, typically with balance thresholds and conditions that limit accessibility.

The middle tier consists of national online banks with established track records: names like Ally, Marcus by Goldman Sachs, and Synchrony, which have historically trailed the very top of the rate table but offer superior apps, insurance coverage, and service infrastructure. These institutions are currently paying in the 3.75 to 4.00 percent range. CIT's Platinum Savings account, for instance, offers 3.75 percent APY on balances of $5,000 or more, according to NerdWallet's April 2026 tracking.

The bottom tier is where most Americans still park their money: traditional brick-and-mortar banks paying 0.01 to 0.50 percent on standard savings accounts. The opportunity cost of not moving deposits from a traditional savings account to a competitive high-yield account at current rate levels is not trivial. A $50,000 balance earns approximately $5 per year at 0.01 percent and roughly $2,100 per year at 4.21 percent. That $2,095 differential is real money that requires no investment risk, no lock-up period, and no specialized knowledge to capture.

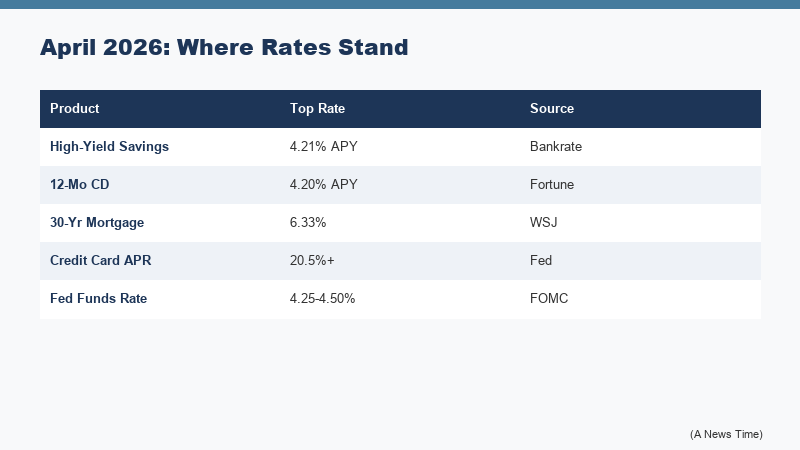

| Product | Best Available Rate | National Average | One-Year Ago |

|---|---|---|---|

| High-yield savings (HYSA) | 4.21% APY | ~0.60% APY | 4.85% APY (peak) |

| 12-month CD | 4.20% APY | ~1.80% APY | 5.10% APY (peak) |

| 30-year fixed mortgage | 6.33% | 6.33% | 6.80% |

| Credit card APR (average) | N/A | ~20.5% | ~20.7% |

| Auto loan, 60-month new | ~6.50% | ~7.10% | ~7.60% |

| Personal loan (online lender) | ~8.50% | ~12.40% | ~13.20% |

CD Yields: The Case for Locking In Rates Now

Certificate of deposit rates follow a different logic than savings accounts. Where savings rates move in real time with the federal funds rate, CD yields lock in a rate for the chosen term, creating an asymmetric opportunity in an environment where the rate trajectory is uncertain. According to rate data published on April 21, the best available 12-month CD rate stands at 4.20 percent, essentially matching the top savings rate but with the added protection of a rate guarantee for the full year.

The argument for CDs over savings accounts right now depends on one's forecast for the Federal Reserve. If the next Fed move is a rate cut, a 12-month CD at 4.20 percent locks in today's elevated yield for a full year. If the Fed surprises and raises rates, the savings account holder benefits in real time while the CD holder is temporarily at a disadvantage. The Fed's own communications through have consistently emphasized patience and data dependence, and the CME FedWatch tool shows the market pricing less than a 30 percent probability of a cut before September.

The Kevin Warsh confirmation hearing context matters here. Warsh, nominated by President Trump to chair the Federal Reserve, is broadly considered more hawkish than the current leadership. His confirmation, if it proceeds, would signal a policy disposition toward fighting inflation more aggressively and cutting rates more slowly than markets currently expect. The Fox Business report published on noted that "how the Federal Reserve shapes your wallet" is directly tied to the outcome of Warsh's Senate hearing, particularly for the 63 million Americans who carry a credit card balance month to month.

For those Americans, the credit card math is brutal and has not improved despite two years of rate cuts. The average credit card APR remains above 20.5 percent nationally, according to Federal Reserve data. A $10,000 credit card balance at 20.5 percent generates roughly $2,050 in annual interest charges at minimum payment rates, a figure that makes even the best savings account rate irrelevant if the borrowing side of the household balance sheet is not addressed first.

Tax Refunds and the Behavioral Finance Moment

The post-tax deadline period is one of the few times per year when a significant share of the population has a discrete cash event that creates a genuine decision window. The IRS typically issues more than 100 million refunds each filing season, with the average refund in 2025 running approximately $3,100 per return. For households that received a refund in , the question of where to put that money is not abstract: a $3,100 lump sum deposited in a 4.21 percent HYSA versus a 0.01 percent traditional savings account generates roughly $130 versus $0.31 over the next 12 months.

Behavioral finance research consistently shows that tax refunds are among the most likely cash windfalls to be saved rather than spent, because they feel like "found money" rather than earned income. That behavioral dynamic makes the post-April 15 window one of the highest-value moments in the personal finance calendar for actually moving money from low-yield to high-yield accounts.

The other post-deadline action item is the Roth IRA contribution window. Taxpayers have until the April 15 deadline to make prior-year Roth or traditional IRA contributions, but those who filed for an extension or missed the deadline for prior-year contributions should know that the 2026 contribution year itself runs until April 15, 2027. The 2026 Roth IRA contribution limit remains $7,000 for those under 50 and $8,000 for those 50 and older, with income phase-out thresholds that have adjusted modestly for inflation. This is documented in our earlier breakdown of the Gen X retirement gap and the catch-up contribution mechanics available in 2026.

Consumer Debt Trends and the Credit Card Problem

The Federal Reserve's most recent consumer credit data, released for February 2026, showed total revolving credit outstanding at an annualized growth rate that has moderated from the sharp post-pandemic surge but remains elevated relative to pre-2020 norms. Credit card delinquency rates at major banks have ticked higher over the past four quarters, with the 90-plus day delinquency rate at several large issuers now running above the levels seen in 2019, pre-pandemic. That trend has not yet reached crisis levels, but it represents a meaningful deterioration in the credit quality of the average borrower carrying a balance.

The structural problem is the rate asymmetry built into the consumer finance system. When the Federal Reserve raised rates aggressively in 2022 and 2023, credit card issuers passed through the increase almost entirely, pushing average APRs from roughly 16 percent to above 20 percent. When the Fed began cutting in late 2024, credit card rates barely moved. The CFPB has documented this asymmetry in published research, noting that credit card issuers treat rate hike pass-through as a near-automatic function while treating rate cut pass-through as discretionary. The result is a system that systematically disadvantages borrowers relative to depositors, and that disadvantage has compounded since 2022.

"As borrowing costs stay high, the outcomes for households diverge sharply based on whether their primary exposure is to savings rates or credit costs. The Federal Reserve's hold stance is good news for savers and essentially neutral for borrowers who have been carrying high-rate balances for two or more years."

Fox Business, reporting on the Federal Reserve's April 2026 policy stance, April 21, 2026

For the household trying to navigate this environment, the priority stack is relatively clear from a pure finance perspective: high-interest credit card debt above roughly 15 percent should be the first priority for any tax refund or savings windfall, because the guaranteed return from eliminating a 20 percent APR obligation exceeds what any HYSA can offer after tax. Once high-rate debt is eliminated or managed, moving to competitive savings products becomes the next logical step. For those navigating a job loss or income disruption, the CNBC Select analysis published on April 21 noted that credit cards, used strategically, remain a legitimate bridge mechanism in the absence of other liquidity. The key distinction is between balance-carrying and transacting: carrying a balance at 20-plus percent is a wealth destruction event; paying in full each cycle on a rewards card is a different activity entirely.

The mortgage rate environment, which touches a different segment of the consumer finance picture, is worth tracking alongside savings and credit card data. The WSJ reported on April 21 that the 30-year fixed mortgage rate sits at 6.33 percent, down from the 7 percent-plus levels seen in late 2023 but still elevated enough to keep the housing market frozen for many would-be buyers. For the full housing market picture, see the companion analysis in our housing market and mortgage rate report for the week of April 21-22.

The Forward Outlook: What Moves Rates Next

Three variables will determine where consumer finance rates sit by year-end. The first is the Federal Reserve's rate path, which the market currently sees as on hold through mid-2026 at minimum. The second is the Kevin Warsh confirmation hearing and its implications for Fed leadership's policy preferences. The third is the trajectory of inflation data: if April and May CPI readings show renewed upside pressure from tariffs or energy costs, the small probability of a rate hike that some Fed watchers assign would increase, and the window for rate-cut-driven savings rate compression would push further out.

For savers, the near-term read is constructive: rates above 4 percent in federally insured accounts are likely to be available through at least Q3 2026. For borrowers, particularly those carrying high-rate credit card balances, the structural relief that would come from a Fed easing cycle appears further away than it did six months ago. The behavioral opportunity created by the post-tax deadline window is real and time-limited. The financial difference between acting on it and not is measurable in hundreds of dollars per year for the typical household, with no additional risk required.

Frequently Asked Questions

What is the best high-yield savings account rate in April 2026?

According to Bankrate's April 2026 tracking, the best high-yield savings account rate is 4.21 percent APY, offered at Vio Bank with a $100 minimum deposit. Fortune's broader tracker found rates up to 5.00 percent available at select smaller institutions with specific balance requirements. NerdWallet tracks CIT Bank's Platinum Savings at 3.75 percent APY for balances of $5,000 or more.

Should I put my tax refund in a high-yield savings account or pay off credit card debt?

From a pure finance perspective, eliminating credit card balances charging more than 15 percent APR generates a guaranteed return that exceeds what any HYSA can offer on an after-tax basis. If credit card balances are already zero, a high-yield savings account at 4.21 percent APY is the highest-yield, lowest-risk place to park a tax refund in the current environment.

Are CD rates still worth locking in during April 2026?

The best 12-month CD rate is 4.20 percent APY, essentially matching top savings rates but with a guaranteed term. The case for a CD depends on one's forecast for Fed rate moves. If the next Fed action is a cut, locking in today's rate for 12 months via a CD protects against that downside. Markets currently price less than a 30 percent probability of a rate cut before September 2026.

Why haven't credit card APRs come down even as the Fed cut rates?

The CFPB has documented that credit card issuers pass through Fed rate hikes almost automatically but treat rate-cut pass-through as discretionary. This asymmetry means the 2022-2023 hiking cycle pushed average credit card APRs from roughly 16 percent to above 20 percent, and the modest cuts in 2024-2025 produced minimal relief for card holders. Average APRs remain above 20.5 percent nationally as of April 2026.

What is the 2026 Roth IRA contribution limit?

The 2026 Roth IRA contribution limit is $7,000 for individuals under age 50 and $8,000 for those age 50 and older. Income phase-out thresholds apply for high earners. Contributions for the 2026 tax year can be made until April 15, 2027.