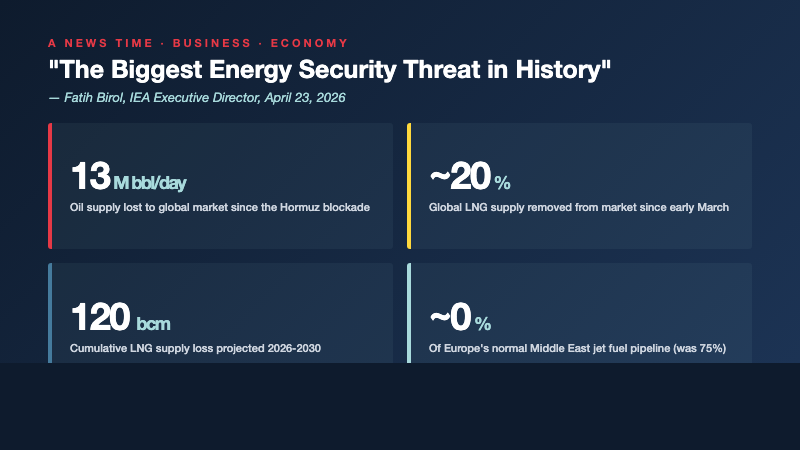

Fatih Birol, executive director of the International Energy Agency, used CNBC's CONVERGE LIVE stage in Singapore on to deliver one of the bluntest assessments of his tenure. The world, he said, is "facing the biggest energy security threat in history." Speaking virtually to anchor Steve Sedgwick, Birol put a number on what the disruption has already cost. As of Thursday, 13 million barrels per day of oil have been removed from global supply, alongside major disruptions in other vital commodities flowing through the Persian Gulf. The Strait of Hormuz, which previously carried roughly 20 million barrels per day of oil and petroleum products, sits under a de facto double blockade with neither Iran nor the United States permitting commercial transit.

The framing matters because Birol is the most institutionally cautious major voice on global energy policy. The 32-member IEA has spent 50 years calibrating language about supply shocks. When the agency moves from describing a disruption to using historical superlatives, it signals that the reference points it usually relies on, the 1973 oil embargo, the 1979 Iranian Revolution, the 1990 Gulf War, no longer fully describe what is unfolding.

The Numbers Behind the Headline

Birol's "biggest in history" claim rests on the combined effect of the oil disruption and a parallel collapse in liquefied natural gas flows that the IEA documented in its Q2 2026 Gas Market Report. The shipping disruption through Hormuz since early March has removed close to 20 percent of global LNG supply, according to the report. During the most volatile stretch of March, natural gas prices in Asia and Europe hit their highest levels since January 2023, and natural gas demand in key importing markets contracted sharply in response.

| Metric | Pre-crisis baseline | April 2026 status |

|---|---|---|

| Oil through Strait of Hormuz | ~20 million barrels/day | Effectively blockaded |

| Oil supply lost to global market | n/a | 13 million barrels/day |

| Share of global LNG removed | n/a | ~20% |

| Global LNG production (March, YoY) | +12% (Oct 2025-Feb 2026) | -8% |

| European gas demand (March, YoY) | n/a | -4% |

| Cumulative LNG loss, 2026-2030 | n/a | ~120 billion cubic metres |

| Europe jet fuel from Middle East refineries | ~75% of supply | ~Zero |

The numbers describe two distinct problems on different timelines. The oil disruption is acute and visible at the gasoline pump. The LNG disruption is structural and will reshape gas markets for at least the next four years. Damage to liquefaction infrastructure in Qatar, the world's largest LNG exporter, has reduced projected supply growth and pushed the long-anticipated wave of global LNG capacity expansion back by at least two years. The IEA estimates the combined effect of immediate supply losses and slower capacity growth could remove a cumulative 120 billion cubic metres of LNG supply between 2026 and 2030, an amount roughly equal to a full year of European gas imports at pre-crisis levels.

Europe's Jet Fuel Problem

Among the immediate practical effects, the European jet fuel supply chain is the one most likely to surface in news cycles over the next several weeks. Birol told CNBC that Europe normally sources about 75 percent of its jet fuel from Middle East refineries. That pipeline, he said, is "basically now zero." European airlines and fuel distributors are scrambling to source replacement supply from refineries in the United States and Nigeria.

"Europe gets about 75% of its jet fuel from refineries in the Middle East and this is basically now zero. Europe is now trying to get it from the U.S. and Nigeria. If we are not able to get, in Europe, additional imports from the countries now, we will be in difficulties."

Fatih Birol, Executive Director, International Energy Agency, CNBC CONVERGE LIVE, April 23, 2026

If the substitute supply does not materialize at sufficient scale, Birol said, Europe may need to take measures to reduce air travel directly. That is the kind of policy intervention that has not been seriously considered in modern European aviation history outside the Covid-19 pandemic. The IEA has separately warned of an imminent jet fuel crunch in Europe, with some countries facing shortages within weeks. The summer travel season, which begins in earnest in early June, sits directly in the impact zone.

What This Does to Energy Policy

Birol used the same CNBC interview to outline the energy mix shifts he expects the crisis to accelerate. Nuclear power gets a boost. Renewables, particularly solar and wind, grow strongly. Electric vehicles benefit. And, in a less comfortable observation for climate-focused policymakers, coal will likely see a push back upward, particularly in large Asian economies seeking near-term replacement for disrupted gas supply.

"I expect, first of all, nuclear power, will get a boost. Renewables will grow very strongly, solar, wind and others, and I expect electric cars will benefit from this. In some countries, I expect coal may also see a push and go back up, especially in some big countries in Asia."

Fatih Birol, IEA, CNBC CONVERGE LIVE, April 23, 2026

Each of those reallocations carries its own multi-year capital cycle. Nuclear projects do not come online quickly enough to relieve a 2026 supply shock. Solar and wind capacity additions are constrained by interconnection queue backlogs, particularly in the United States and Germany. Coal restarts can happen on a faster timeline, which is why Birol singled them out, but each restart locks in higher carbon emissions for the depreciation life of the unit. The Iran war, in other words, is forcing energy policy decisions on a timeline that does not match the timelines of climate policy commitments.

The Stockpile Math Is Buying Time, Not Solving the Problem

The IEA agreed in March to release 400 million barrels of oil from member emergency stockpiles, the largest coordinated release in the agency's history. Birol has indicated the agency would consider a second tranche if conditions warrant. He has been careful to frame the release as palliative rather than curative.

"This is only helping to reduce the pain, it will not be a cure. The cure is opening up the Strait of Hormuz. We are gaining some time, but I don't claim that this will be a solution, our stock release."

Fatih Birol, IEA, "In Good Company" podcast with Nicolai Tangen, April 2026

The math behind that framing is straightforward. At 13 million barrels per day of lost supply, 400 million barrels of stockpile release covers roughly 31 days of the gap. A second tranche of similar size buys another month. Beyond two months, the global oil system runs out of buffer absent reopening of the strait or finding sustained alternative supply. India and China are reorganizing their crude purchasing around Russian and West African flows, but those substitutions are constrained by tanker availability and refining configuration.

Market Implications: Winners, Losers, and Inflation

The market response to the IEA's framing has been muted relative to the severity of the underlying numbers, in part because oil prices have already absorbed much of the disruption since the conflict began. Brent crude has been trading in a $95 to $110 per barrel range, with WTI closely correlated, and equity markets have largely processed the energy supply story as a known unknown. Analysts at Goldman Sachs raised recession odds to 30 percent in the days following the Hormuz closure, and several sell-side desks have published 2026 forecasts assuming sustained energy-driven inflation.

For investors and corporate treasurers, the IEA report points to three durable themes. First, integrated energy majors with diverse production geography and downstream exposure are positioned to capture margin from the disruption while pure upstream Middle East exposure carries asymmetric downside. Second, LNG infrastructure operators outside Qatar and the UAE, particularly North American projects that were already in advanced construction, gain pricing power as the global supply expansion wave is delayed. Third, the inflation pass-through from sustained energy prices into core CPI creates a Federal Reserve policy environment that is harder to ease than the macro picture suggested even six months ago.

Those themes are now consensus rather than contrarian, which is itself a useful signal. The market has priced in disruption. What it has not yet priced in, and what Birol's "biggest in history" framing is implicitly arguing it should, is the possibility that the disruption proves structural rather than temporary.

What to Watch Next

Three near-term catalysts will determine whether Birol's assessment holds up over the next quarter. The first is whether any diplomatic channel produces a credible reopening timeline for the Strait of Hormuz. The IEA, Trudeau-era former officials, and the OECD have all called for negotiations, but no concrete proposal has yet emerged that would persuade either Tehran or Washington to lift the blockade. The second is the trajectory of European jet fuel supply through May and into the summer travel season. Concrete shortages would force policy interventions that have not been seen since the pandemic. The third is whether the IEA chooses to release a second tranche of emergency oil reserves, a decision that would signal the agency expects the disruption to persist past its initial planning horizon.

The bigger question is what energy security looks like as a category once a supply shock of this magnitude has been absorbed. Diversified long-term contracts, strategic stockpiles, alternative routes, and accelerated domestic production all return to the policy menu in ways that have not been politically accessible since the early 2000s. Birol's CNBC interview was one of those rare moments when an institutional voice tells policymakers, in plain language, that the assumptions underlying the previous 30 years are no longer reliable. The rest of 2026 will reveal which capitals were paying attention.