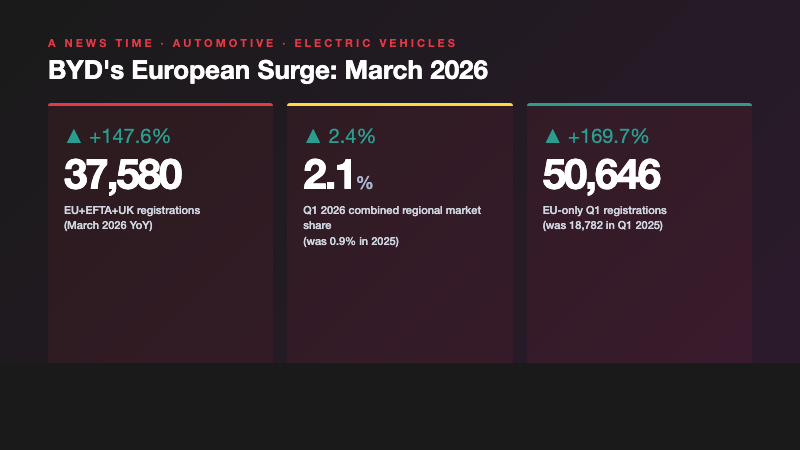

BYD nearly tripled its European sales in March, registering 37,580 new cars across the combined EU, EFTA, and United Kingdom market according to European Automobile Manufacturers' Association data published Thursday. The 147.6 percent year-over-year jump from March 2025 cemented the Shenzhen-headquartered company as one of the fastest-growing automakers of scale operating in Europe, and put it within striking distance of overtaking SAIC's MG brand as the largest single Chinese vehicle exporter in the region. BYD's market share across the combined region rose to 2.4 percent in March, more than double the 1.1 percent recorded a year earlier.

The first-quarter numbers tell an even sharper story. BYD registered 73,847 units across the combined EU, EFTA, and UK region between January and March 2026, lifting Q1 market share to 2.1 percent from 0.9 percent a year earlier. Within the EU specifically, the company's growth has been even more pronounced. March 2026 EU registrations reached 21,158 units, up 155.2 percent from 8,291 in the same month a year earlier. Q1 EU registrations totaled 50,646 units, up 169.7 percent from 18,782 in Q1 2025.

The Tariff Workaround Comes Online This Year

The single most important variable in BYD's European trajectory is the company's pending shift from imported product to locally assembled product. Local assembly is set to start in Hungary and Turkey later in 2026, which lets BYD bypass the additional tariffs imposed by the European Commission in October 2024 on China-made fully electric vehicles. Those tariffs added between 17 and 35 percent to landed costs for Chinese BEV imports depending on the manufacturer, with BYD specifically subject to a 17 percent counterveiling duty on top of the standard 10 percent EU import tariff.

The arithmetic of moving production into Europe is straightforward. The current 27 percent combined tariff burden on BYD's China-built EVs sold in the EU compresses gross margin by roughly the same amount, which the company has absorbed through aggressive pricing rather than passed through to consumers. Once Hungarian and Turkish production reaches scale, that 27 percent margin pressure largely disappears for the EU-bound product. The pricing flexibility that creates is significant. BYD can either hold prices and recapture margin, or cut prices further and accelerate share gains against European incumbents already struggling with EV transition economics.

| Region | March 2026 | March 2025 | YoY change | Market share |

|---|---|---|---|---|

| Combined EU + EFTA + UK | 37,580 units | ~15,180 units | +147.6% | 2.4% (vs. 1.1%) |

| EU only | 21,158 units | 8,291 units | +155.2% | 1.8% (vs. 0.8%) |

| Q1 combined region | 73,847 units | ~32,800 units | +125.1% | 2.1% (vs. 0.9%) |

| Q1 EU only | 50,646 units | 18,782 units | +169.7% | 1.8% (vs. 0.7%) |

The Dual-Powertrain Strategy That Made the Difference

The Q1 product mix is what separates BYD's European performance from the older Chinese-export playbook. The company's lineup spans both fully battery-electric and plug-in hybrid models across multiple price points, from the urban Dolphin Surf (sold as Seagull in China) up to the mid-size Seal U DM-i. That breadth has let BYD capture demand on both sides of a European EV market that has been moving in two directions at once.

Fully electric vehicles reached 19.4 percent of EU market share in Q1, up from 15.2 percent a year earlier, according to the ACEA figures. Plug-in hybrids climbed to 9.5 percent, up from 7.6 percent, with registrations growing 29.7 percent year-over-year. That plug-in hybrid acceleration outpaced BEV growth in the same period, driven by buyers in Italy, Spain, and Germany returning to PHEV models in response to revised tax incentive frameworks. Italian PHEV registrations more than doubled in Q1, up 110.1 percent. Spanish registrations rose 74.2 percent. German registrations climbed 19.3 percent.

BYD's Seal U DM-i and Seal 06 DM-i plug-in hybrid models sit directly in the price ranges where those policy tailwinds have translated into demand.

Cláudio Afonso, EV and CARBA founder, in his April 23, 2026 analysis

The European dealer footprint that supports those sales has been built out aggressively since 2023, with BYD partnering with established dealer groups in Germany, the United Kingdom, Spain, Italy, and France. The brand awareness that came with the dealer expansion is now translating into the conversion volume the registration data reflects.

BYD vs. SAIC, and What Comes Next

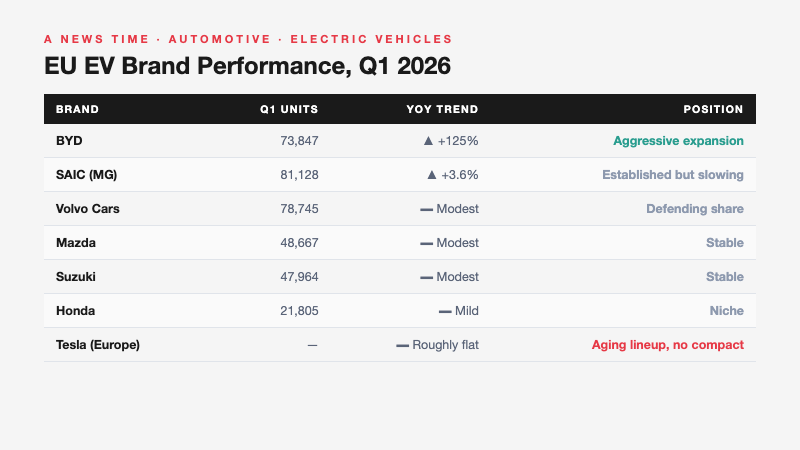

BYD is not the only Chinese automaker expanding in Europe, but it is the one expanding fastest. SAIC Motor, parent of the longer-established MG brand, registered 81,128 units in the combined region in Q1, up 3.6 percent year-over-year. SAIC retained the larger total share base at 2.3 percent, but its growth has stalled to roughly the rate of overall European market expansion.

The two Chinese groups now sit within 7,281 units of each other for the quarter. At BYD's current acceleration rate, that gap closes by the second quarter of 2026 and BYD becomes the largest single Chinese vehicle exporter to Europe by volume. BYD already ranked ahead of several established European and Japanese brands in Q1, outpacing Volvo Cars (78,745 units), Honda (21,805), Mazda (48,667), and Suzuki (47,964). The company sits in the second tier of European-market presence that includes Renault, Toyota, and Hyundai.

The competitive implication for European incumbents is uncomfortable. Rivian's R2 launch in the United States is an analogous test of whether a startup can break the dominance of legacy automakers, but in Europe the test is between Chinese scale and European legacy. BYD is winning. Volkswagen, Stellantis, and Renault have all been forced to accelerate their EV roadmaps and cut costs aggressively in response, with mixed results so far.

The Labor Question That Has Not Gone Away

BYD's growth is not happening in a clean reputational environment. The company has been facing multiple accusations of labor rights violations at its overseas factories, including prosecution in Brazil for human trafficking at a factory site and reported labor concerns at its Hungarian operations. The Hungarian production launch later this year will put those questions directly into the European political conversation, where labor standards and supply-chain due-diligence rules are tighter than in the markets BYD has previously operated in.

How European regulators handle the friction between attractive consumer pricing on Chinese EVs and the labor standards questions surrounding their production is one of the most consequential automotive policy debates of 2026. The European Commission's Corporate Sustainability Due Diligence Directive, which took partial effect last year, will be a real-world test of whether the legal framework can constrain the most aggressive low-cost competitors without simply pushing the market back toward more expensive incumbents.

What to Watch Through Q2 and Q3

The next data points that will define BYD's European story are predictable in shape if not in magnitude. April and May ACEA registrations will show whether the March surge was a sustainable trajectory or a single-month anomaly tied to inventory clearing. The Hungarian production launch, currently targeted for the second half of 2026, will determine when the tariff benefit actually flows through the income statement. The labor standards conversation will define how much political headwind the company faces as its share grows past 3 percent in major EU markets.

The broader European new automotive market grew 4 percent overall in Q1 2026, with March delivering the strongest monthly performance as registrations rose 12.5 percent year-over-year across the EU. The combined EU, EFTA, and UK market reached 3.52 million units in Q1. BYD captured a disproportionate share of that growth, which is precisely the dynamic European policymakers were trying to prevent when they wrote the 2024 tariffs. The next 12 months will reveal whether the policy framework is enough to slow the trajectory, or whether BYD's local production move neutralizes it entirely.

What This Means for Tesla, Volkswagen, and the Legacy EU Brands

The competitive consequence of BYD's European acceleration is most visible in the share data of the legacy European EV producers. Volkswagen's ID series, Renault's Megane E-Tech, and Stellantis's Peugeot e-3008 and Fiat 600e have all faced price pressure in the segments where BYD's Atto 3, Dolphin, and Seal models compete directly. The European response so far has been a mix of price reductions, accelerated next-generation product launches, and political lobbying for tariff enforcement. None of those tools alone is sufficient to slow BYD's trajectory if the company achieves its planned 5 percent regional market share by the end of 2027.

Tesla's position in the European market is also worth tracking against the BYD numbers. Tesla European registrations have been broadly flat through Q1 2026, with the Model Y holding the top single-model EV sales position in several European markets but the brand's overall growth trajectory below the segment average. The aging Model Y, the limited Model 3 refresh, and the absence of a competitively priced compact European-market product have all contributed. BYD's Dolphin and Seal models are taking share that, in a different competitive environment, would have flowed to a Tesla compact entry that has not yet materialized.

| Brand | Q1 2026 trend | Strategic position |

|---|---|---|

| BYD | +125% combined region YoY | Aggressive expansion, Hungary production imminent |

| SAIC (MG) | +3.6% YoY | Established but slowing |

| Tesla | Roughly flat | Aging lineup, no compact entry yet |

| Volkswagen Group | Modest growth | Pricing pressure, accelerating ID refresh |

| Renault Group | Modest growth | Megane E-Tech holding, R5 ramp continuing |

| Stellantis | Mixed by brand | Peugeot performing, Fiat slower |

The Q1 data shows the European EV market is no longer a Tesla-versus-legacy story. It is increasingly a three-way contest between Chinese exporters expanding aggressively into Europe, the established European brands defending mid-market share, and Tesla maintaining a premium position that depends heavily on the Model Y's continued appeal. Whichever of those three approaches captures the most share through 2027 will define the structure of the European EV market for the rest of the decade.