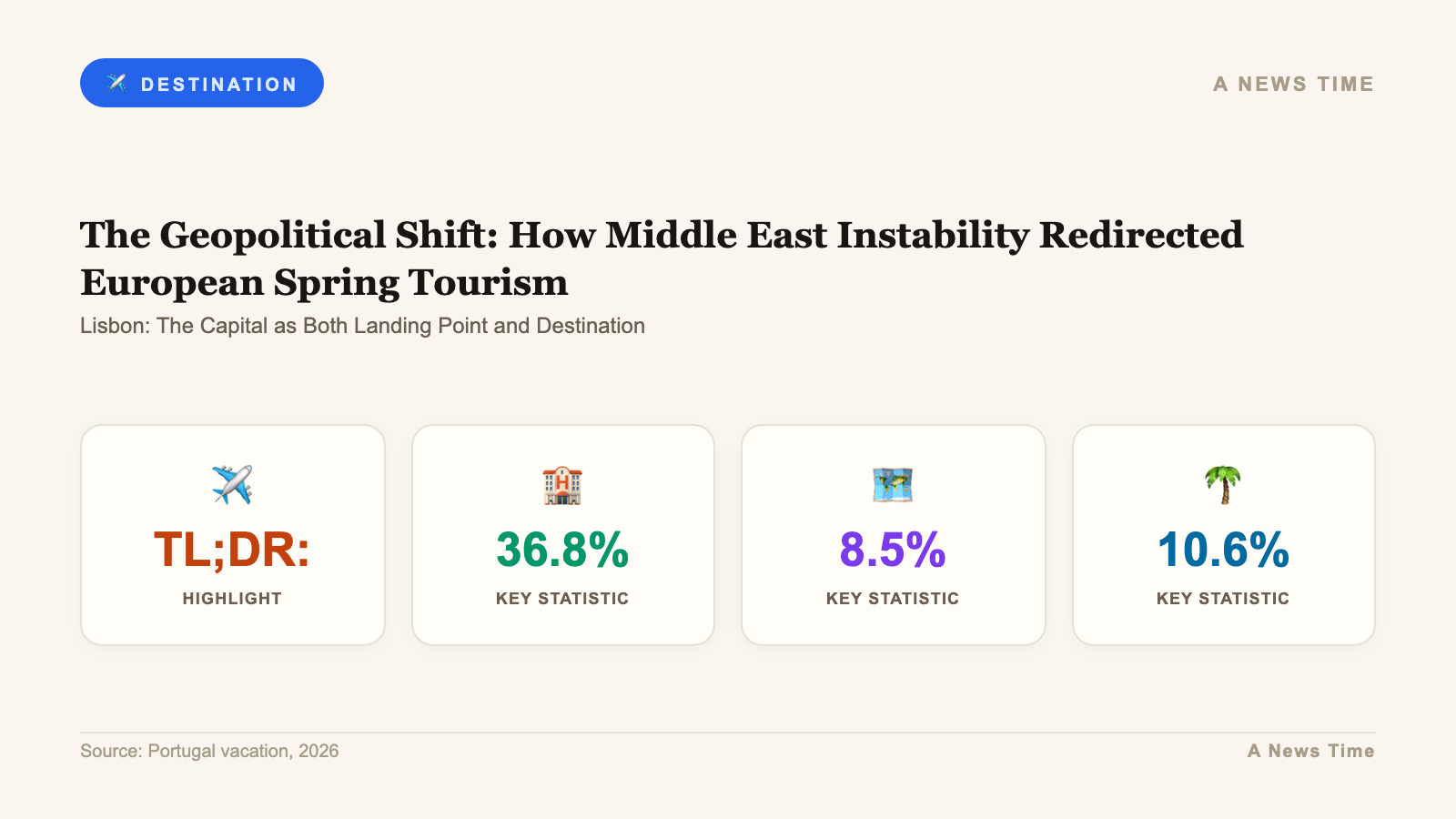

The numbers arrived in the booking platform dashboards before most of the industry was paying attention to them. A 36.8% spike in hotel searches from Italy. A 63.1% surge in international flight searches compared to the same window in 2025. Canadian travelers up 10.6%. American travelers, accustomed to treating the Iberian Peninsula as a secondary consideration behind France, Italy, and Spain's established tourism circuit, up 8.5% and accelerating.

The data was telling a story that the travel industry would spend several weeks catching up to. Portugal, specifically Lisbon, Porto, and the Algarve, had become the default Easter 2026 destination not because of a new airport or a viral marketing campaign but because the alternatives felt unsafe. The eastern Mediterranean was no longer the category it had been. The Middle East conflict's expansion through 2025 and into early 2026 had not just closed specific routes. It had fundamentally altered the risk calculus for the millions of European and North American travelers who plan spring holidays months in advance and adjust those plans in the final weeks based on news cycles they cannot quite articulate but viscerally process.

Portugal was positioned almost perfectly for the redirected demand. It sits at the westernmost edge of continental Europe, as physically distant from Middle East instability as a short-haul European destination can be. It has a well-developed tourism infrastructure from decades of investment in Lisbon, Porto, and Algarve hospitality. Its cuisine, wine, and cultural heritage offer genuine depth for travelers who arrive specifically because somewhere else felt impossible. And its price point, still meaningfully below comparable western European destinations despite a decade of tourism growth, made it accessible to the budget-conscious traveler choosing between Portugal and staying home.

The Geopolitical Shift: How Middle East Instability Redirected European Spring Tourism

Understanding Portugal's Easter 2026 surge requires mapping the travel patterns it displaced. Before the Middle East conflict intensified in late 2025, the spring holiday market for European and North American travelers distributed across a familiar set of destinations: Greece and its islands, Turkey's Aegean coast, Jordan and Egypt for cultural immersion, Israel for religious travel, Cyprus, Lebanon's recovering Beirut.

The US-Israel war on Iran that began in late 2025 did not simply close those routes. It created a zone of uncertainty that extended well beyond the direct conflict geography. Travel insurance providers escalated premiums for the eastern Mediterranean region broadly. Airlines operating through airspace near the conflict area began filing amended route plans, adding hours to flights that had previously been routine. The State Department's worldwide caution advisory issued in early 2026 created a liability environment that prompted corporate travel managers to restrict bookings to the region entirely.

For leisure travelers, the psychological dimension is arguably more significant than the practical one. An Italian family planning an Easter holiday in Greece might reasonably have calculated that Santorini was objectively safe in April 2026. But the news environment made the conversation about that trip exhausting in a way it had not been before. Every family dinner where the holiday came up required reassurances that the research supported but that the emotional register of the news cycle continuously undermined. Portugal required no reassurances. It was simply not part of the discussion that was making travel uncomfortable.

The data from Sojern's digital marketing tracking, which monitors travel search behavior across booking platforms, captured this shift in near real-time. The Swiss market saw flight searches to Portugal rise 15.3%. Germany was up 8.9%. Spain, paradoxically, saw a 1.9% increase in searches to neighboring Portugal, suggesting that even Spanish travelers were considering cross-border alternatives to their own domestic destinations or the eastern Mediterranean routes they might otherwise have taken.

Pedro Costa Ferreira, president of the Portuguese Association of Travel and Tourism Agencies (APAVT), characterized the demand as exhibiting "very low elasticity." Travelers who had decided Portugal was where they needed to be were not deterred by price increases. Hotels that had raised rates 15 to 25% above their 2025 spring comparables were still reaching full occupancy weeks ahead of Easter. The travelers coming were willing to pay the premium because the alternative was not a cheaper Portugal vacation. The alternative was uncertainty.

Lisbon: The Capital as Both Landing Point and Destination

Lisbon Humberto Delgado Airport processed approximately 25% more international arrivals in the two weeks preceding Easter 2026 compared to the same period in 2025. The airport's terminal capacity had been a persistent concern for Portuguese tourism authorities through the growth years of 2019 and 2022 through 2025, and the Easter surge pushed several operational metrics to their limits without quite breaking through them.

TAP Air Portugal added frequency on its London, Paris, Frankfurt, and Rome routes in the three weeks before Easter, responding to demand signals that were coming through too clearly to ignore. The Lisbon to New York nonstop, operated by both TAP and Delta, ran full aircraft for essentially the entire spring holiday window. Several charter operators pivoted capacity from suspended eastern Mediterranean routes to Lisbon, bringing German, Swiss, and Scandinavian travelers who would not have otherwise appeared in the Portuguese market.

Within Lisbon, the hotel market performed at levels that surprised even the more bullish operators. Properties in the Bairro Alto, Chiado, and Alfama neighborhoods, which represent the highest-demand leisure accommodation zones, reached 95 to 100% occupancy for the Easter weekend itself and the surrounding days. The Lisbon luxury segment, defined by properties above 250 euros per night for a standard room, saw the fastest rate growth: average daily rates in the five-star category tracked 28% above the same Easter period in 2025.

The boutique hotel sector benefited particularly from the surge. Properties in the 80 to 150 euro per night range, occupying converted Pombaline townhouses in Principe Real and Santos neighborhoods, reported that their typically slower April period had transformed into something resembling August. Operators who had budgeted conservatively for the spring season found themselves repricing remaining inventory upward through February and March as the booking curve steepened in ways their revenue management systems hadn't modeled.

Restaurant reservations in central Lisbon demonstrated a similar compression. Restaurants along the Rua das Flores and in the Time Out Market's surrounding neighborhood were fully booked through Easter week by mid-March. The city's natural advantage here, a dining culture that is genuinely excellent across a price range from affordable tascas to destination-level contemporary Portuguese cooking, meant that the influx of travelers with higher willingness to spend found a hospitality ecosystem capable of absorbing that spending meaningfully.

Porto: The Secondary City That Stopped Being Secondary

Porto's emergence as a co-equal Easter 2026 destination rather than an afterthought to Lisbon is one of the more interesting structural developments in Portuguese tourism over the past three years. The city's combination of UNESCO-listed riverfront architecture, world-class port wine culture, a genuinely excellent restaurant scene, and accommodation pricing that runs 20 to 35% below comparable Lisbon properties has produced a traveler profile shift that the data makes visible.

Flight searches to Francisco Sa Carneiro Airport from the key source markets, Italy, Germany, Switzerland, France, and the UK, were all up by double-digit percentages for the Easter window. Ryanair, easyJet, and Vueling, the low-cost carriers that drive a substantial portion of Porto's inbound volumes, were reporting load factors above 90% on the pre-Easter routes from Rome, Milan, Berlin, and Manchester. TAP's Porto routes from Lisbon's hub were fully booked, contributing to overflow demand in Lisbon as well.

The Ribeira district along the Douro riverfront, Porto's equivalent of Lisbon's Alfama in terms of tourist gravity, was attracting the kind of visitor volumes during Easter week that would have been unremarkable in August but were genuinely unusual for April. The visual draw of the Dom Luis I Bridge and the port wine lodges across the river in Vila Nova de Gaia is at least as powerful as Lisbon's Belem Tower circuit and benefits from being slightly less photographed, which retains a quality of discovery for the traveler who arrives knowing Porto less well than the capital.

The Douro Valley, accessible in a 90-minute drive from Porto and offering some of Europe's most dramatic wine country scenery, received overflow tourism from the Easter surge that its quintas and boutique hotel operators were not universally prepared to handle. Several valley properties that normally book out in September and October for harvest season were surprised to find their Easter availability exhausted by mid-March. The valley's combination of steeply terraced vineyards, river boat cruises, and atmospheric quinta dining is particularly well matched to the "cultural immersion and heritage" motivation that destination data suggested was driving a growing share of the Portugal bookings.

The Algarve: Resilience in the Beach Market Despite Changed Traveler Mix

The Algarve's Easter 2026 performance was the most complex of the three destination nodes. The region's traditional market, Northern European families seeking guaranteed sunshine, early season warmth, and beach access at Easter, showed up in expected volumes. But the traveler mix was notably different from 2025. The displaced eastern Mediterranean visitors, particularly the Italian and North American segments, arrived with different expectations and spending patterns than the Algarve's historical golf-and-beach clientele.

Hotel occupancy in the Algarve's premium western coast segment, centered on Lagos, Luz, and Sagres, reached 88 to 92% for the Easter weekend compared to approximately 78% in 2025. The central Algarve around Albufeira and Portimao, which draws a higher proportion of package holiday travelers, was at 82 to 86% occupancy, lower than the western premium segment but still significantly above the 2025 comparables.

The Italian visitor surge to the Algarve is worth noting specifically. The 36.8% increase in hotel searches from Italy tracked by Sojern appears to have translated into actual bookings that showed up disproportionately in the western Algarve's quality hotel segment rather than in budget package accommodation. Italian leisure travelers, particularly those who had been considering Greece or Turkey as their Easter destination, tend to prioritize hospitality quality and food when redirected. The western Algarve's combination of dramatic cliff scenery, excellent fresh seafood, and well-managed boutique hotel stock was well positioned for this segment.

The broader cultural tourism interest that destination research identified, with travelers choosing Portugal "to understand the culture and discover heritage" rather than purely for beach access, created some operational challenges for Algarve operators whose infrastructure is calibrated for beach and golf rather than cultural programming. Visitors asking about local history, regional cuisine beyond the standard seafood menu, and inland exploration were sometimes finding local operators underprepared for demand that their colleagues in Lisbon and Porto field routinely.

The Price Discovery: How Hotels and Airlines Responded to Demand

The revenue management response to Portugal's Easter 2026 surge illustrates how the hospitality industry prices genuine demand shocks. The acceleration in hotel rate increases was steeper in the final six weeks before Easter than in the comparable period of 2025, reflecting both the higher baseline demand and the earlier exhaustion of standard-rate inventory.

Lisbon's luxury segment saw the most dramatic dynamic pricing. Properties that had set their Easter rates in November 2025 at 15% above 2024 comparables found those rates selling out within weeks. Their revenue management systems, detecting near-full occupancy well outside the normal booking window, automatically triggered upward repricing of remaining inventory. The process iterated several times through January and February, each round revealing that demand remained inelastic to the price increase. The result was a genuine price discovery process that set the effective Easter market rate approximately 28% above 2025 actuals, with some premium properties reaching 35 to 40% premium over the prior year.

Airlines demonstrated a similar pattern but on a compressed timeline. The low-cost carriers that serve the bulk of intra-European Portugal routes work with dynamic pricing systems that respond to seat availability and booking pace in near-real-time. Ryanair and easyJet routes from Rome, Frankfurt, and Zurich to both Lisbon and Porto were reporting fares 30 to 50% above their standard April pricing by late February as seat availability narrowed. TAP Air Portugal's transatlantic routes from Newark and JFK held their published fares longer, partly due to corporate booking commitments that created a floor price discipline, but premium cabin availability on the Lisbon transatlantic routes was essentially exhausted by early March.

"What we saw was not a normal Easter demand pattern. This was structural redirection of spring travel spend that would have gone to Turkey, Greece, Egypt, or Jordan in a different geopolitical environment. Portugal absorbed it because it was ready and because it was safe."

Industry analyst, Portuguese hotel sector conference, March 2026

The resilience of demand against higher prices speaks to the nature of the displacement. Travelers who had specifically decided that eastern Mediterranean destinations were off-limits for 2026 were not price-shopping within Portugal against alternatives. Portugal had become the category. Within the category, price sensitivity was lower than in a normal competitive market.

Beyond the Beach: Heritage Tourism and the New Portuguese Traveler

One of the more consequential long-term developments embedded in the Easter 2026 data is the shift in traveler motivation toward cultural heritage and "authentic experiences" as primary travel drivers rather than sun and beach access.

Destination research cited in industry reports noted that many of the 2026 travelers who chose Portugal specifically articulated a desire to "understand the culture and discover heritage" as a primary motivation. This is a different traveler profile from the Algarve golf package market or the Lisbon weekend-break city-trip market that has dominated Portuguese tourism growth since 2016. It represents something closer to the deep-culture tourism that Italy and France have historically captured from North American and Asian markets.

The practical expression of this demand showed up in bookings for experiences that would not have appeared in volume in the 2022 to 2024 Portuguese tourism data. Fado performances in Lisbon's Alfama district sold out weeks ahead of Easter. Wine-focused tours of the Douro Valley, Alentejo, and the Dao region were booking at rates more typical of autumn harvest season. Cultural itineraries centered on Portuguese history, the Age of Discoveries monuments, and the Manueline architecture of the monasteries at Belem and Batalha were generating booking inquiry volumes that national heritage sites were not fully prepared to translate into managed experiences.

This heritage interest is particularly visible in the secondary cities and regions that appeared in the Visitor Sentiment Analysis study cited in industry reports. Viana do Castelo in the Minho region, a town of extraordinary Romanesque and Art Deco architecture with minimal tourist infrastructure, saw significant increases in accommodation searches from travelers who had specifically been researching Portuguese heritage beyond the Lisbon-Porto-Algarve triangle. The Alentejo coast, an area of wild Atlantic beaches, cork oak forests, and whitewashed hill towns, received similar attention from travelers seeking something that looked less like southern Europe's overrun tourist circuit and more like a place with its own logic and pace.

The Leonardo Hotels group's announcement of expanded Portuguese hotel portfolio development reflects the industry's reading of this trend as durable rather than crisis-driven. If the cultural heritage demand persists beyond the geopolitical emergency that partially created it, the investment case for boutique heritage hotels in secondary Portuguese cities looks considerably stronger in 2026 than it did in 2022.

Sustainability Pressures: The Other Side of Portugal's Tourism Boom

The Easter 2026 surge did not arrive without generating concerns within the Portuguese tourism sector that the volume was creating the same pressures that have produced protests and regulatory responses in Barcelona and Amsterdam.

Lisbon's housing market has been under significant pressure from the intersection of short-term rental growth, digital nomad relocation, and general investment demand since 2019. The Easter 2026 surge amplified that pressure in a specific context: the visible economic benefit of tourism to property owners and hospitality operators reinforces incentives to convert residential housing to tourist use, which reduces housing supply for permanent residents and contributes to the rent inflation that has been among the most politically sensitive issues in Portuguese domestic politics.

The Portuguese government has been implementing a series of measures to address this tension, including limitations on new tourist apartment licenses in Lisbon and Porto's historic centers, and a "Mais Habitacao" housing policy package that includes provisions to incentivize the return of short-term rental properties to long-term residential use. The Easter 2026 surge provided new urgency to the implementation of these measures while simultaneously generating the tourism revenue that funds the political willingness to contemplate regulation.

Pedro Costa Ferreira's observation that the "elasticity of demand" remains very low despite higher prices and sustainability-focused policy discussions is the key insight for the medium-term Portuguese tourism outlook. The destinations that have managed rapid growth most successfully are those that used the revenue generated during high-demand periods to invest in infrastructure, housing supply, and quality-of-life improvements for residents. Portugal has the revenue. The question is whether the institutional capacity to direct it toward those investments develops fast enough to prevent the social backlash that Barcelona and Amsterdam are now managing.

For travelers, this tension resolves practically into the advice that applies across Europe's successful but stressed tourism destinations in 2026: go off-peak, spend in locally owned businesses, leave the famous neighborhoods to themselves for significant portions of your visit, and accept that the tourist taxes and fees you encounter exist because they need to. Portugal is still, even after years of growth and despite Easter 2026's surge, a country where the relationship between visitors and the visited remains more in balance than in many of its European neighbors. That balance is worth protecting by the way you travel within it.

What Easter 2026 Tells Travelers About Portugal in 2027 and Beyond

The safe-haven narrative that drove Portugal's Easter 2026 numbers will evolve as geopolitical conditions change. If Middle East tensions ease and eastern Mediterranean routes return to full normalcy, some of the redirected demand will flow back. But the evidence from destination research suggests that a meaningful share of the travelers who discovered Portugal's depth in 2026 will return on its own merits.

The travelers who came expecting a substitute for Turkey or Greece and found a genuinely distinct travel culture, the wine, the seafood, the fado, the Manueline architecture, the quality-to-price ratio of the hospitality outside Lisbon's premium center, are not likely to reallocate those preferences back to the destinations they replaced. They may add Portugal to a travel repertoire rather than treating it as a permanent substitute, but that addition creates a durable demand increment that will outlast the geopolitical conditions that first produced it.

The practical implications for 2027 travelers to Portugal are clear. Book accommodation earlier than you would have in 2024. The Easter window and the summer peak have both tightened booking timelines significantly. Consider the secondary destinations, Viana do Castelo, Evora, Obidos, Alcobaca, the Alentejo villages, that represent Portugal's cultural depth without its crowd density. And accept that Portugal in 2026 and 2027 is a country in the middle of a tourism growth arc that will continue to produce both higher prices and richer experiences, in the destinations that are investing the revenue in maintaining what makes them worth visiting.

For perspective on how Portugal compares to European destinations that are further into the overtourism curve, see our analysis of Barcelona, Venice, and Amsterdam's visitor management challenges and our profile of Japan's approach to managing tourism growth through the 2026 bilateral tourism push with the United States.