ECB policymaker Alexander Demarco said on that the euro zone economy may be moving toward the central bank's adverse scenario, but stressed that policymakers must resist the urge to rush into rate changes despite mounting inflation pressure from the Iran war energy shock. Speaking on the sidelines of the IMF spring meeting in Washington, the Malta central bank chief became the latest ECB governing council member to signal that patience, not haste, should guide the bank's next move.

Three Scenarios and a Difficult Choice for the ECB

The ECB outlined three scenarios for inflation and growth at its meeting, ranging from a benign outcome in which energy disruptions prove temporary to an adverse scenario in which the Iran war triggers a self-reinforcing price spiral. Policymakers have spent the subsequent weeks debating which scenario is materializing and whether interest rate increases are needed to prevent inflation from becoming entrenched.

Demarco's assessment landed squarely in uncertain territory. "My impression is that at this juncture we could be veering towards the adverse scenario," he told Reuters. The statement carried weight because it came from a governing council member who simultaneously argued against acting on that assessment too quickly.

"If the adverse scenario would materialise, then two rate hikes anticipated by the market would be a reasonable expectation," Demarco added, validating the market's pricing while cautioning against preemptive action.

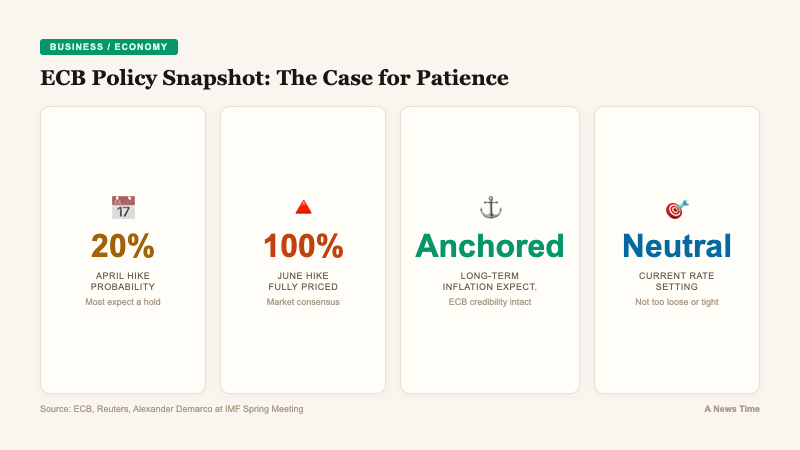

"So far, inflation expectations are quite well anchored. We need to be patient, not rush any decision and see what the data tells us."Alexander Demarco, Governor, Central Bank of Malta and ECB Governing Council Member

Market Pricing and the April 30 Decision

Financial markets have moved aggressively to price in ECB tightening since the Iran war disrupted global energy flows. The current market pricing tells a clear story of escalating expectations:

| ECB Meeting Date | Market-Implied Probability of Hike | Cumulative Hikes Priced |

|---|---|---|

| 20% | 0.2 hikes | |

| 100% (fully priced) | 1 hike | |

| Anticipated | 2 hikes |

Policymakers speaking both on and off the record to Reuters have played down the chance of a move at the meeting, arguing that even if price growth is at risk of becoming embedded, there is no hard evidence of it happening yet. The consensus among governing council members appears to favor gathering more data before committing to a rate change.

Why the ECB Can Afford to Wait

Demarco outlined several structural reasons for patience, each of which distinguishes the current situation from past inflation crises that demanded urgent central bank intervention:

- Anchored expectations: Longer-term inflation expectations remain well anchored, suggesting businesses and consumers have not lost confidence in the ECB's ability to maintain price stability

- High credibility: The ECB's inflation-fighting track record gives it room to observe before acting, unlike central banks that enter crises with damaged reputations

- Neutral starting point: Interest rates are currently at a neutral setting, meaning the bank entered this crisis neither too loose nor too tight

- Target-level inflation pre-crisis: Price growth was at the 2% target before the war, reducing the risk that underlying inflation dynamics were already problematic

These factors collectively argue that the energy shock is an external supply disruption rather than evidence of overheating demand, and that the appropriate response may be to "look through" the temporary price spike rather than tighten into a potential economic downturn.

Business Surveys Hold the Key to the June Decision

Demarco identified the ECB's own survey of business executives, due for the meeting, as a crucial data point. Corporate pricing behavior will likely determine whether the governing council moves in June or holds longer.

"If expectations remain well anchored, the conflict proves temporary, and business signals do not suggest a big adjustment in selling prices, then there is a case for looking through this episode. There are of course limits to how much businesses can absorb. They need to make a profit. This is why I think signals from corporations will be crucial."Alexander Demarco, ECB Governing Council Member

The logic is straightforward. If businesses are absorbing higher energy costs through margin compression rather than passing them to consumers through price increases, the inflation spike is more likely to prove temporary. If, however, companies are broadly repricing their goods and services to protect margins, the risk of a wage-price spiral increases significantly, and the case for rate hikes strengthens.

The distinction matters because it determines whether the ECB is dealing with a one-time price level adjustment or a self-sustaining inflation dynamic. The former can be tolerated; the latter demands a policy response.

Parallels and Divergences With the Federal Reserve

The ECB's dilemma mirrors, but does not replicate, the challenge facing the U.S. Federal Reserve, which is confronting its own inflation-versus-growth tradeoff driven by the same energy shock. Both central banks entered the crisis with rates near neutral and inflation near target, and both face pressure to tighten into what could be a recessionary environment.

The differences are significant, however. The euro zone is more directly exposed to Middle East energy disruptions through its natural gas import dependency, while the U.S. benefits from greater domestic energy production. The ECB also faces a more fragmented fiscal landscape, with individual member states responding differently to the crisis and limited capacity for coordinated fiscal stimulus compared to the U.S. Treasury.

The Fed's own policy trajectory has shifted dramatically since the Iran war began, with rate cut expectations evaporating and rate hike probabilities rising. The two central banks' decisions will interact through currency markets: if the ECB hikes while the Fed holds (or vice versa), the resulting euro-dollar shift will have significant implications for trade flows and imported inflation.

The Adverse Scenario: What Would Two Hikes Mean?

If the adverse scenario does materialize, the two rate hikes that Demarco described as "a reasonable expectation" would represent a significant shift in the ECB's policy stance. Rates would move from neutral to restrictive territory, deliberately slowing economic activity to contain inflation.

The implications would ripple across the euro zone economy:

- Mortgage markets: Higher rates would increase borrowing costs for homebuyers across the 20 member states, with outsized impacts in countries with high variable-rate mortgage exposure

- Corporate investment: Businesses already hesitating due to war uncertainty would face higher financing costs, potentially deepening the investment slowdown

- Government debt: Highly indebted member states like Italy and Greece would see their borrowing costs rise, reviving concerns about fiscal sustainability

- Currency effects: Rate hikes would likely strengthen the euro, partially offsetting imported energy inflation but hurting export competitiveness

The IMF's own spring meeting analysis has warned that coordinated tightening by major central banks in response to the energy shock could trigger a synchronized global slowdown. The Fund has urged central banks to distinguish between supply-driven and demand-driven inflation before acting, a message that aligns with Demarco's call for patience.

What to Watch Before the ECB Decides

The next six weeks will determine the ECB's course. Between now and the June meeting, several data points will either validate Demarco's patient approach or force the governing council's hand:

- The ECB business executive survey (available for the April 30 meeting)

- April flash inflation estimates for the euro zone

- Progress (or lack thereof) in Iran ceasefire negotiations and Strait of Hormuz transit

- Wage negotiation outcomes in major euro zone economies, particularly Germany

- The ECB staff's updated macroeconomic projections

Demarco's message from Washington was carefully calibrated: acknowledge the risk without triggering panic, validate market expectations without committing to action, and preserve the governing council's flexibility to respond as data arrives. Whether that flexibility survives the next round of inflation prints remains the open question. The ECB has the credibility to wait. The question is whether the data will give it the luxury of doing so.