U.S. stocks rallied and Brent crude fell more than 8% on , a day after Iran announced it was ending its weeks-long blockade of the Strait of Hormuz. The Dow Jones Industrial Average closed above 49,400 and the S&P 500 notched a record high as investors priced in lower inflation, a more dovish Federal Reserve path, and the return of roughly 12 million barrels per day of Middle East crude output to global markets.

The rally is real. The underlying supply chain recovery is not going to match it. A survey of energy analysts, shipping executives, and economists this weekend makes the gap between the two very clear, and investors leaning into cyclicals, emerging markets, and mega-cap tech on the news need to understand what they are actually buying.

What the market priced in on Friday

The immediate move was a textbook risk-on reversal. The Dow added 868 points, the Nasdaq gained 1.52%, and the S&P 500 closed at 7,126, a record. Nvidia, the bellwether for both the AI trade and semiconductor demand, rose 1.68% and pulled the broader chip complex with it. Small-caps led, as they typically do when investors decide the economy has more room to run.

Three bets sit underneath the rally. First, oil stays below $90 and probably drifts toward $80. Second, a softer energy backdrop clears the way for the Federal Reserve to resume rate cuts in the second half of 2026. Third, Asian manufacturing economies, which were hit hardest during the blockade because their refineries depend on Middle East crude, recover faster than U.S. or European exposure.

Charles Rinehart, chief investment officer at Johnson Investment Counsel, summed up the thesis to Business Insider.

With the Strait of Hormuz now reopening, there's renewed optimism that broader economic momentum can re-emerge.

Charles Rinehart, Chief Investment Officer at Johnson Investment Counsel

That is the story. The story is not wrong. It is just incomplete, and the gap is where the next few months of volatility live.

Why oil prices do not snap back

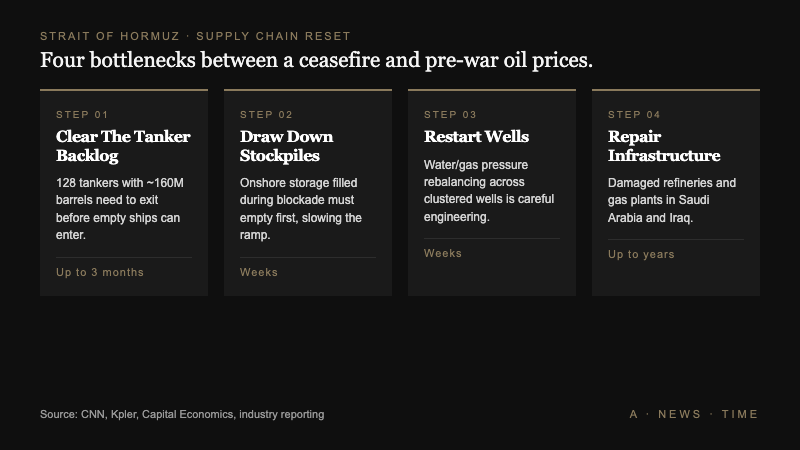

The short answer is physics. The longer answer, from CNN's detailed walkthrough with analysts at Capital Economics, Kpler, and RBC Capital Markets, involves four distinct bottlenecks that have to clear in sequence before the oil market fully normalizes.

- Tanker backlog. Roughly 128 tankers carrying around 160 million barrels are sitting in or near the strait. Those ships have to clear out before empty vessels can enter. Tankers move at the speed of a leisurely bicycle ride, which is not a joke, it is a spec. Victoria Grabenwoger, senior oil analyst at Kpler, estimates up to three months to restore full transit capacity.

- Stockpile drawdown. Producers filled storage during the blockade because they had nowhere else to put barrels. Empty ships draw from those warehouses first, which slows the ramp of fresh production.

- Restarting wells. Middle Eastern oil wells cannot be turned on like a light switch. Water and gas injection pressures need to be rebalanced across clustered wells to avoid reservoir damage. The engineering work takes weeks, not days.

- Infrastructure repair. Refineries, natural gas plants, and some oil producers were damaged during the war. Industry sources told CNN that some of those repairs will take years.

The futures curve is already pricing this in. Brent is trading around $90 on Friday's close, roughly $20 above pre-war levels. The futures market now projects Brent at $77 by year-end and no return to pre-war prices until 2029. Michael Green, chief strategist at Simplify Asset Management, has pointed out that historically Brent needs to be in the $60s for gasoline to settle near $3 a gallon. The futures market does not expect that until 2030.

What a Friday-high Dow gets you, and what it does not

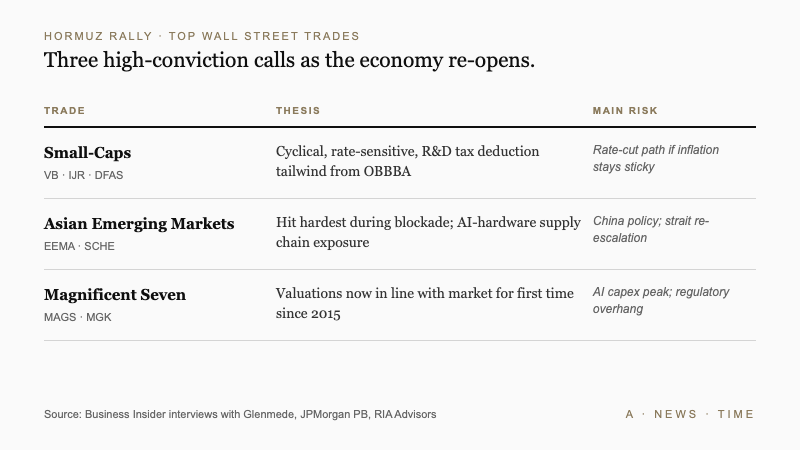

The numbers Wall Street pros are watching fall into three buckets, and each has a different shape of risk.

| Trade | Thesis | Main risk |

|---|---|---|

| Small-caps (VB, IJR, DFAS) | Cyclical, rate-sensitive, benefits from R&D tax deduction in the One Big Beautiful Bill Act | Rate cut path if inflation stays sticky |

| Asian emerging markets (EEMA, SCHE) | Hit hardest during blockade, cheapest valuations, AI-hardware supply chain exposure | China policy risk, re-escalation in the Gulf |

| Magnificent Seven (MAGS, MGK) | Valuations now in line with the broader market for the first time since 2015 | AI capex cycle peaking, regulatory overhang |

Mike Reynolds, vice president of investment strategy at Glenmede, argued to Business Insider that smaller stocks are positioned for "a really banner year in 2026" because they benefit on three axes at once: cyclical recovery, Fed rate sensitivity, and immediate deduction of research spending under current tax law.

Stephen Parker, co-head of global investment strategy at JPMorgan Private Bank, pointed to Korea, Taiwan, and Chinese tech as the cleanest bounce-back trade, describing the AI hardware supply chain there as "thrown out with the bathwater during the recent sell-off." Lance Roberts at RIA Advisors argued that the Magnificent Seven are the cheapest they have been versus the rest of the market since 2015, a reset worth buying.

All three trades assume the strait stays open. All three ignore the fact that the strait actually closed again briefly on April 18, with two ships reporting attacks, per reporting from the Washington Post. Insurance markets have not absorbed this yet. Marine coverage prices have surged by thousands of percentage points during the conflict, and underwriters are unlikely to offer affordable coverage while Iran retains the right to approve each vessel's passage.

The insurance problem

If you want to understand why shipping companies will not simply flood the strait next week, look at the insurance market. Hapag-Lloyd, the German container shipping major, called the reopening "good news" and said it would prefer to resume transit once insurance and clearance questions resolve. Maersk went further and said it has made no changes to its guidance to vessels since the reopening announcement.

Helima Croft, global head of commodity strategy at RBC Capital Markets and a former CIA analyst, put it bluntly to CNN: "The fine print of the agreement will matter. If Iran continues to have the final say on passage, some insurers and shippers may be reluctant to rush back in."

That is the structural reason oil does not snap back to pre-war levels even in a best-case scenario. Risk premia priced into marine insurance feed directly into shipping costs, which feed into delivered crude prices, which feed into refined product prices. Each layer takes weeks to adjust. Each layer can re-widen on a single incident. For investors anchoring the Friday rally to a clean transition back to normal, the insurance market is the cleanest early-warning indicator of whether that rally was earned.

What the Fed is actually watching

Federal Reserve rate-cut odds have swung violently with each headline out of the Gulf. The case for cuts runs through the oil price, which runs through headline inflation. Futures markets had been pricing rate-hike risk at over 50% during the worst of the blockade. After Friday, those odds collapsed and cut odds for the second half of 2026 moved materially higher.

The complication is stagflation risk. Seven weeks of war, global supply disruptions, and a currency-sensitive energy shock have pushed the global inflation-growth mix in exactly the direction the Fed least wants to see. Data this coming week will test whether that stagflation scenario is firming up, and the central bank's response function depends heavily on whether the April CPI print confirms the hopeful story the bond market is telling.

Thierry Wizman, global FX and rates strategist at Macquarie Group, offered the clearest framing of the risk: "Trust in the market's rally, at this junction, requires trust in Trump alone." That is not a partisan statement. It is an analytical one. The agreement that reopened the strait remains verbal, unsigned, and subject to re-interpretation, and Friday's rally was effectively a market vote of confidence in its durability.

What to watch next

Three indicators will tell investors whether the Friday rally holds. First, marine insurance rates for Strait of Hormuz transits. If Lloyd's of London and its peers start cutting premiums materially next week, shipping volumes will follow and the oil price move to $80 becomes credible. If premiums stay elevated, the rally was front-running a supply normalization that is not coming.

Second, Iran's behavior on charging tolls for strait passage. Iran used transit fees during the blockade as leverage. Whether those fees disappear in the post-ceasefire regime, or whether they persist as a de facto tax on global shipping, tells you how much of the strait's use Iran actually ceded.

Third, the April CPI print. If energy-driven disinflation shows up cleanly in the data, the Fed's rate-cut path opens back up and the small-cap thesis strengthens. If services inflation stays sticky despite falling gasoline prices, the bond market's optimism looks premature and equity leadership rotates again.

The equity market priced a return to normal on Friday. The oil market priced a slow, contingent, still-risky recovery. Those two stories cannot both be right for long. The next six weeks decide which one the data actually supports.

Frequently Asked Questions

When will gas prices return to pre-war levels?

The futures market projects Brent crude at around $77 by year-end 2026 and does not expect a return to pre-war prices until 2029. Historically, gasoline near $3 per gallon requires Brent in the low $60s, which markets do not anticipate until 2030.

Why did the stock market rally so hard on the news?

Investors priced in three things at once: lower energy-driven inflation, a clearer Federal Reserve path toward rate cuts, and a recovery in emerging-market economies that depend on Middle East crude. All three assumptions hinge on the strait staying open.

Is the Strait of Hormuz actually reopened?

Iran announced the reopening on April 17, 2026, but the strait briefly closed again on April 18 with two ships reporting attacks. Insurance markets and major shipping firms like Maersk have not yet normalized their guidance to vessels.

Which trades are Wall Street pros recommending?

Small-cap ETFs (VB, IJR, DFAS), Asian emerging-market ETFs (EEMA, SCHE), and Magnificent Seven vehicles (MAGS, MGK) are the three highest-conviction picks circulating this weekend, each with distinct risk profiles tied to rate policy, Chinese demand, and AI capex.

How long until Middle East oil production fully recovers?

Kpler analysts estimate up to three months to restore full tanker transit capacity. Restarting damaged refineries and natural gas infrastructure could take years. Roughly 12 million barrels per day of crude and 3 million barrels per day of refined products were offline at peak, mostly in Saudi Arabia and Iraq.

Sources

- If the war's over, when does everything go back to normal? - CNN Business

- Market pros share 3 investments to load up on after the Strait of Hormuz reopening - Business Insider

- Here's what the stock market might have gotten wrong about the Iran war - The Washington Post

- Seven weeks of war: Is the global economy sliding into stagflation? - Moneycontrol