Russia's government will honor existing subsidy commitments to businesses but sharply reduce new support as the federal budget strains under war spending, depleted reserves, and the fiscal cost of keeping concessional credit cheap, Economic Development Minister Maxim Reshetnikov told a Russian entrepreneurship forum on . The comments, first reported by The Moscow Times, mark the clearest official signal yet that the state-driven growth model of the past three years is reaching its limits.

For anyone tracking the Russian economy from the outside, the numbers matter more than the rhetoric. Headline growth has already collapsed, the National Wealth Fund has shed more than half its value since the war began, and the subsidized-lending programs that kept small and mid-size businesses afloat are now costing the budget more than officials can sustain at current interest rates.

The numbers behind the pullback

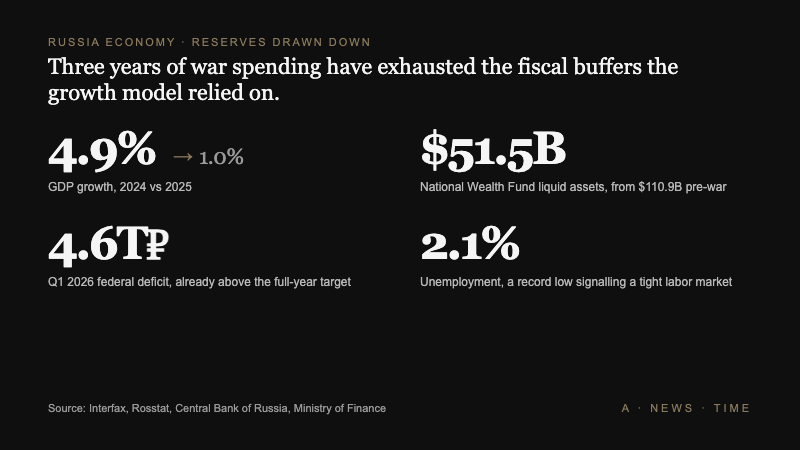

Russia's economy expanded 4.1% in 2023 and 4.9% in 2024, driven by mobilizing spare labor, industrial capacity, and fiscal reserves. Those buffers are now largely exhausted. Growth slowed to just 1% in 2025. GDP in January and February 2026 came in 1.8% below the year-earlier period, though fewer working days may have flattered the comparison.

The budget is where the strain shows up most sharply. The federal deficit hit 5.6 trillion rubles in 2024, equivalent to 2.6% of GDP. In the first quarter of 2026 alone, the deficit reached 4.6 trillion rubles (roughly $60.7 billion), or 1.9% of GDP, already exceeding the full-year target the Ministry of Finance had set. That is not a drift above target. It is a meaningful breach in the first three months of the fiscal year.

Reserve depletion is the second pressure point. Liquid assets in the National Wealth Fund have fallen to 3.9 trillion rubles ($51.5 billion), down from 8.4 trillion rubles ($110.9 billion) before the war. Central Bank Governor Elvira Nabiullina has pointed out that production capacity is near its limit, financial reserves are drawn down, and banks have less capital headroom for new lending. The labor market is tight: unemployment hit a record low of 2.1% in February.

Deputy Kremlin chief of staff Maxim Oreshkin and Nabiullina have both argued the mobilizable slack that drove the 2023-2024 expansion is gone. Reshetnikov's Friday comments are the operational acknowledgment of that assessment.

The subsidized-lending problem

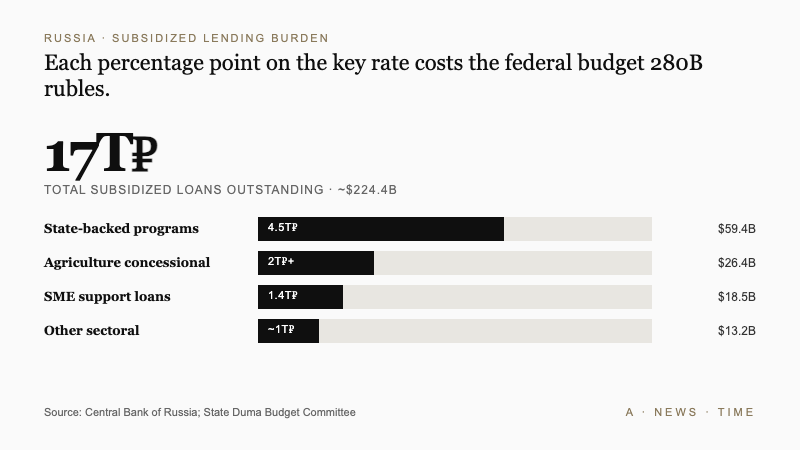

The specific binding constraint is the cost of keeping interest rates cheap for favored borrowers. The Central Bank estimates subsidized loans now total around 17 trillion rubles ($224.4 billion), including roughly 4.5 trillion rubles ($59.4 billion) in state-backed lending programs across small business, agriculture, and other sectors. Small and medium-sized enterprise programs account for about 1.4 trillion rubles, agriculture for more than 2 trillion, and miscellaneous borrowers for nearly 1 trillion.

| Program | Outstanding balance | Approx. USD |

|---|---|---|

| Total subsidized loans | 17T rubles | $224.4B |

| State-backed concessional lending | 4.5T rubles | $59.4B |

| SME support loans | 1.4T rubles | $18.5B |

| Agriculture concessional loans | 2T+ rubles | $26.4B+ |

| Other sectoral programs | ~1T rubles | $13.2B |

The problem with this structure is that it gets more expensive as the Central Bank keeps rates high to fight inflation. Each additional percentage point in the key rate costs the federal budget about 280 billion rubles ($3.7 billion), according to Andrei Makarov, head of the State Duma's Budget and Taxes Committee. With rates still elevated, the subsidy bill has grown into one of the largest non-defense line items in the budget.

Reshetnikov was direct about the implication.

We continue to implement all existing support measures. But the current situation, including the budget, does not mean we will subsidize lending programs or distribute grants at the same scale as during Covid.

Maxim Reshetnikov, Russia's Economic Development Minister, at an April 17 entrepreneurship forum

The shift toward capital markets

The official new direction is to push businesses toward equity financing instead of debt. Reshetnikov said the vector was moving away from subsidized interest rates and toward supporting capital in various forms, including helping more mature businesses access IPOs. Nabiullina has long argued the same thing. Her point is that widespread subsidized lending dulls the effectiveness of monetary policy because cheap credit is still available to large parts of the economy regardless of what the key rate does.

The numbers say that shift will be hard. Russian market capitalization has fallen by roughly a third since the war began. President Vladimir Putin set a target in 2024 of doubling stock market capitalization to 66% of GDP by 2030, up from 33% at the time. Hitting that target would require annual IPO volume of at least 1 trillion rubles for multiple years, according to Central Bank First Deputy Governor Vladimir Chistyukhin, a pace roughly equal to the entire IPO volume in Russia over the past decade combined.

Equity financing is also harder to engineer quickly. Debt subsidies can be structured and dispersed through existing state-owned banks in a matter of months. Developing a domestic capital market that can absorb 1 trillion rubles a year in new listings requires institutional investor depth, foreign capital access, and corporate governance standards that Russian firms broadly do not yet have. The pivot is real. The timeline is long.

What this means for businesses on the ground

Russian firms that built their plans around continuing access to subsidized credit now have to recalibrate. Reshetnikov's framing, that companies will need to "rely on their own resources" in a labor market and capacity environment significantly tougher than during the Covid-era supports, is a warning shot.

The sectors most exposed are the ones that used concessional lending most aggressively: small and medium-sized enterprises, agriculture, and specific manufacturing subsectors. Several of those industries were already under stress before the Friday announcement. Russia's largest automaker AvtoVAZ moved to a four-day workweek with wage cuts last summer. KamAZ, the heavy truck maker, reintroduced its own four-day week in March as demand collapsed. Steelmakers have been pushing for tax breaks that the government has already declined to provide.

What Friday's announcement confirms is that those earlier signals were not isolated. They were the early edge of a broader fiscal tightening that the government is now framing publicly.

What to watch from outside Russia

For global investors and analysts tracking emerging market exposure, three signals will tell you whether Reshetnikov's pullback is orderly or disruptive. First, whether the Central Bank holds its key rate at current levels or is forced to cut in the second half of 2026 to relieve fiscal pressure. A cut under duress would be a sign that the subsidy math broke before the inflation fight was won.

Second, the trajectory of the federal deficit through Q2 and Q3. The 4.6 trillion ruble Q1 number is already a red flag. If the Q2 print comes in above 3 trillion, the full-year deficit will far overshoot the target and spill into 2027 fiscal planning.

Third, IPO issuance. Chistyukhin's 1 trillion ruble per year target is a useful benchmark. If Russian IPOs land anywhere close to that in 2026, the capital-markets pivot is real. If issuance stays flat, the equity-financing strategy will remain rhetorical.

Russia built its post-invasion economic model on three resources: idle labor, cheap credit, and sovereign reserves. All three are now meaningfully diminished. The Friday announcement is the government telling its own business community that the era of using fiscal capacity to paper over real economic adjustment is ending. What replaces it is less clear, and probably less comfortable.

Frequently Asked Questions

How fast is Russia's economy slowing?

GDP growth fell from 4.9% in 2024 to 1% in 2025. January and February 2026 data showed the economy 1.8% smaller than a year earlier, though fewer working days may have distorted the comparison. The Economic Development Ministry has signaled further slowing ahead.

How large is Russia's federal budget deficit?

The 2024 deficit reached 5.6 trillion rubles, or 2.6% of GDP. In the first quarter of 2026 alone, the deficit hit 4.6 trillion rubles, already exceeding the government's full-year target and raising questions about fiscal sustainability.

What is the National Wealth Fund at now?

Liquid assets in the National Wealth Fund have fallen to 3.9 trillion rubles ($51.5 billion), down from 8.4 trillion rubles ($110.9 billion) before Russia's 2022 invasion of Ukraine. More than half of the reserve has been drawn down.

How much do subsidized loans cost the budget?

Subsidized loans total roughly 17 trillion rubles ($224.4 billion), of which about 4.5 trillion rubles is state-backed. Each additional percentage point in the Central Bank's key rate adds roughly 280 billion rubles ($3.7 billion) to the cost of maintaining those programs.

What is Russia's IPO capitalization target?

President Putin set a goal of doubling stock market capitalization to 66% of GDP by 2030 from 33% in 2024. Central Bank officials estimate that would require roughly 1 trillion rubles ($13.2 billion) in annual IPOs, about equal to the total IPO volume of the past decade combined.

Sources

- Russia Signals Pullback in Business Support as Budget Strains Mount - The Moscow Times

- Russia's KamAZ to Reintroduce 4-Day Workweek as Truck Market Slumps - The Moscow Times

- Russia Rejects Steelmakers' Calls for Tax Breaks as Sector Slump Deepens - The Moscow Times

- Reshetnikov remarks on scaling back business support - Interfax