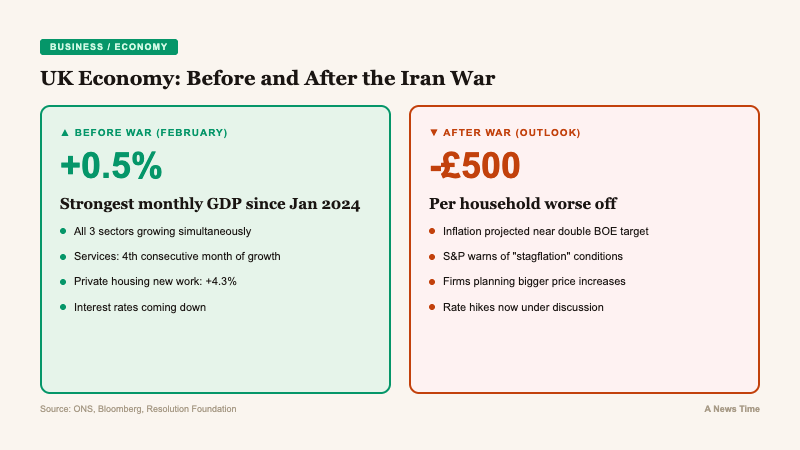

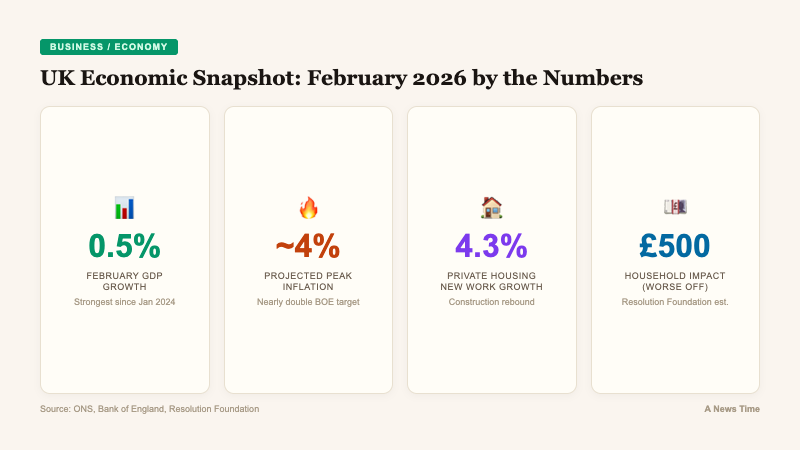

The United Kingdom's GDP expanded 0.5% in February, the Office for National Statistics reported on , delivering the strongest monthly growth reading since and comfortably beating the 0.1% consensus forecast among economists. January's figure was also revised upward to 0.1%. The data reveals an economy that was building genuine momentum in the weeks before the outbreak of war in Iran on , making the subsequent disruption all the more consequential.

Services, Production, and Construction All Expand

February marked the first time all three of the UK's major economic sectors posted simultaneous growth since . The services sector, which accounts for roughly 80% of the UK economy, expanded for a fourth consecutive month, with employment and administrative activities posting particularly large gains.

Industrial production also contributed, reversing a pattern of intermittent contraction that has plagued manufacturing since the post-pandemic normalization period. Construction output was boosted by private housing new work, which grew 4.3%, a sign that the residential building pipeline was active before the war shock hit.

The breadth of the expansion was notable. Most services sub-sectors reported output gains in February, suggesting the growth was not concentrated in a single area but reflected a broad-based pickup in economic activity across the economy.

"I have real frustration because we have busted a gut to get growth into our economy. We were finally showing signs of increased growth, not just increased growth, but sustainable growth."Peter Kyle, UK Business Secretary, speaking to Sky News

Iran War Threatens to Erase Momentum Entirely

The encouraging data arrives with a heavy caveat. The US-Israeli attack on Iran launched on upended global energy supply lines, roiled financial markets, and triggered what economists now describe as the most significant exogenous shock to the UK economy since the COVID-19 pandemic.

The war threatens to hit the UK harder than any other major advanced economy, according to multiple analyses. The OECD has identified Britain as particularly vulnerable due to its reliance on imported energy and the structure of its consumer economy. Inflation, which had been converging toward the Bank of England's 2% target, is now projected to surge to nearly double that level.

The Resolution Foundation estimates that typical households will be £500 ($673) worse off as energy costs feed through to consumer bills and broader price increases. Private-sector economists have slashed UK growth forecasts, and the mood has shifted dramatically from cautious optimism to defensive positioning.

Stagflation Warnings Emerge From Business Surveys

Post-war data already tells a different story from the February figures. S&P Global's private-sector PMI survey warned explicitly of "stagflation" conditions, with firms reporting strong wage growth alongside suppliers passing through higher raw material costs linked to the Middle East conflict.

The Bank of England's own poll of business leaders revealed that firms were planning bigger price increases in March to cope with energy shocks. The combination of rising input costs, elevated wage demands, and weakening confidence creates precisely the policy dilemma that central bankers most dread: inflationary pressure arriving alongside slowing growth.

| Indicator | Pre-War (February) | Post-War Signal |

|---|---|---|

| GDP Growth (Monthly) | +0.5% | Expected to slow sharply |

| Services Sector | 4th consecutive month of growth | PMI warns of stagflation |

| Inflation Trajectory | Converging toward 2% target | Projected near double target |

| Household Impact | Stable | £500 worse off (Resolution Foundation) |

| Business Price Plans | Moderate | Bigger increases planned (BOE survey) |

| Interest Rate Outlook | Cuts expected | Hikes now under discussion |

Bank of England Faces an Impossible Balancing Act

BOE policymakers now face the unenviable task of weighing inflation risks against recession risks ahead of their next meeting on . Before the war, the trajectory was clear: inflation was falling, and gradual rate cuts were the consensus expectation. That calculus has been upended.

Interest rates currently sit in what the BOE considers neutral territory, but the energy shock has introduced a potential inflation spiral that could force rate increases even as the economy weakens. The Middle East conflict, and its repercussions for global energy supply, shows little sign of easing. The current US-Iran ceasefire remains fragile and could unravel at any point.

The parallels to the early 1970s oil shock, when the UK experienced severe stagflation following Middle East conflict, are uncomfortable. While the economy is structurally different today, the core dynamic of an energy-importing nation facing a sudden supply disruption while already dealing with elevated costs is strikingly similar.

"The Iran shock is already showing up in data. S&P's private sector survey warned of stagflation, with firms reporting strong wage growth and suppliers passing through higher raw material costs linked to the war."Bloomberg Economics Analysis

Q1 Growth Expected to Be Strongest in a Year

Despite the war's late-February onset, private-sector economists on average still expect 0.3% growth in the first quarter of 2026, which would represent the fastest quarterly expansion since the first quarter of 2025. That earlier period was also distorted by external factors, as manufacturers rushed to ship goods ahead of US President Donald Trump's tariff deadlines.

The Q1 figure, when it arrives, will represent a snapshot of an economy that was accelerating before being hit by a sudden external shock. The question for policymakers is whether the pre-war momentum was strong enough to provide a buffer against the oil price shock, or whether the February data will mark a high-water point from which the economy retreats.

The Labour government's promise to build 1.5 million homes, which appeared ambitious before the war, now looks even more challenging. Construction costs are rising with energy prices, and the tightening financial conditions driven by rate hike expectations will weigh on mortgage availability and housing demand.

Global Context: UK Vulnerability Compared to Peers

The UK's exposure to the Iran war stands in contrast to economies with different energy profiles. China's GDP data, released the same day, showed 5% growth with limited spillover from the conflict, in part because of years of strategic energy diversification. The eurozone faces its own challenges, with the OECD warning of broad growth downgrades, but the UK's position as a net energy importer with a services-heavy economy makes it uniquely exposed to supply shocks.

The Bank of England entered this crisis from a stronger position than during the 2022 energy shock, with rates already at a level that provides some room for maneuver. But that advantage is limited: the central bank cannot simultaneously fight inflation and support growth, and the war is forcing it toward a choice that has no good outcome.

Kyle, the business secretary, emphasized on that the government had been building momentum before the external shock. He noted that interest rates had been coming down and that there were genuine signs of sustainable recovery. The implicit message was clear: the war, not domestic policy, is responsible for the deterioration in outlook.

What the BOE Meeting on April 30 Will Signal

The BOE meeting will be the most closely watched monetary policy decision in Britain since the emergency sessions of the pandemic era. Markets are pricing in the possibility of a rate increase, a scenario that would have been almost unthinkable when the February GDP data was being collected.

Key factors the Monetary Policy Committee will be weighing include:

- Energy price trajectory: Whether the Iran ceasefire holds or collapses will directly affect UK inflation forecasts

- Wage growth data: Persistent wage increases would strengthen the case for a rate hike

- Business survey signals: Further stagflation warnings could push the committee toward a hold

- Global coordination: The ECB is facing similar dilemmas, and coordinated or divergent responses will affect the pound

- Housing market sensitivity: Any rate increase will immediately affect mortgage affordability and housing construction

The February GDP number is a reminder of what could have been. For a brief window, the UK economy was doing what policymakers had spent years trying to achieve: growing across all sectors, building housing, and creating jobs. That the momentum was interrupted by a war 3,000 miles away underscores how deeply interconnected the global economy remains, and how quickly domestic progress can be undone by external shocks. The next data releases will show whether any of that momentum survived the impact.