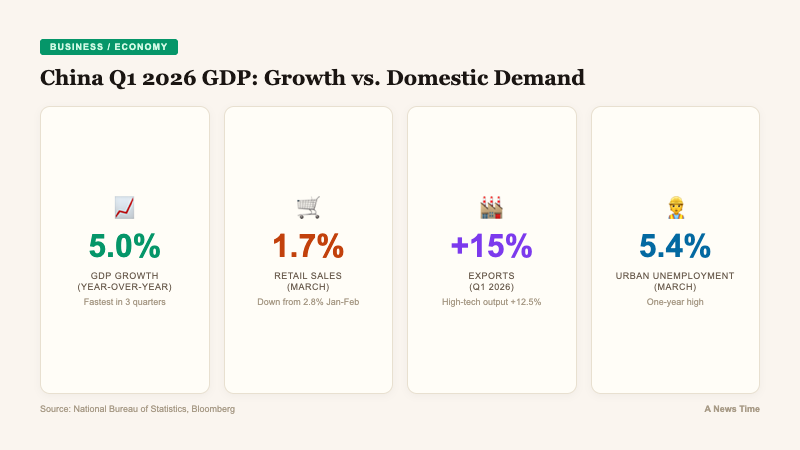

China's GDP expanded 5% year-over-year in the first quarter of 2026, the fastest pace in three quarters, according to data released by the National Bureau of Statistics on . Sequential growth reached 1.3% quarter-over-quarter on a seasonally adjusted basis, the strongest since the final three months of 2024. The results suggest limited economic spillover from the ongoing war in Iran, though they also revealed deepening fractures between China's export-driven manufacturing sector and a domestic consumer economy that continues to stall.

Manufacturing and Exports Drive the Headline Number

The GDP expansion was built almost entirely on the back of industrial production and overseas demand. Industrial output grew 5.7% in March from a year earlier, comfortably beating forecasts. Exports surged 15% in the first quarter, continuing a pattern of Chinese manufacturers capitalizing on global demand even as geopolitical uncertainty intensifies.

Manufacturing contributed roughly one-third of total economic growth in the quarter, according to NBS deputy commissioner Mao Shengyong, who described the result as "precious" given the "severe" external environment. The strength was particularly notable because the year-ago comparison period featured a rush of exports ahead of U.S. tariff deadlines, creating an unusually high base.

High-tech sectors led the charge. Output in high-technology manufacturing expanded 12.5% in the first quarter, more than double the 6.4% gain in manufacturing overall. Industrial robots surged 33%, and integrated circuits climbed 24%, underscoring China's continued push into advanced manufacturing as a strategic priority.

"The manufacturing side of the economy remains resilient and is still a key near-term growth anchor. Looking ahead, China's macro agenda is likely to center on two intertwined priorities: reflation and boosting domestic demand."Hao Zhou, Chief Economist, Guotai Junan International

Consumer Spending Weakens as Unemployment Rises

The contrast between factory floors and shopping malls could not be sharper. Retail sales grew just 1.7% in March, falling well short of expectations and decelerating from the 2.8% expansion recorded in the combined January-February period. The slowdown hit durable goods hardest: car purchases dropped 12%, furniture fell 9%, and home appliances declined 5%.

The weakness reflected the fading impact of government trade-in subsidies, a program that had temporarily boosted consumer electronics and vehicle sales before being scaled back for cars in 2026. Without that artificial tailwind, underlying demand remains tepid.

The labor market offered little reassurance. The surveyed urban jobless rate climbed unexpectedly to 5.4% in March, the highest reading in a year. Fixed-asset investment gained just 1.7% in the first three months, slightly weaker than the 1.8% increase in January-February. Property investment slumped 11.2%. Most alarming for policymakers: private investment declined in the period for the first time on record outside the pandemic year of 2020.

"It's too soon to call China out of the doldrums. Weakness in the private sector is feeding into rising unemployment, an increasingly sensitive political issue likely to prompt targeted stimulus, especially given the private sector's outsized role in job creation."Carlos Casanova, Senior Asia Economist, Union Bancaire Privee

Iran War Ripples Reach Chinese Refineries

While the broader GDP number suggests China has so far insulated itself from the Iran conflict, now in its seventh week, early signs of strain are visible in the energy sector. Refined oil output fell 2.2% in March, indicating that Chinese refiners cut run rates to conserve supplies snarled by disruptions in the Middle East.

China's years of effort to strengthen energy security, including diversifying import sources and building strategic reserves, have helped blunt the immediate shock. Additionally, years of deflationary pressure have limited the potential for higher oil costs to translate quickly into consumer price spikes.

Producer prices turned positive in March for the first time after three and a half years of deflation, a development driven partly by the energy cost pass-through from the war. The broader GDP deflator, a measure of price changes across the economy, fell 0.1% in the first quarter, marking the 12th consecutive quarter of decline. That persistent deflationary trend, even amid a global oil shock, highlights just how deeply weak demand is embedded in the Chinese economy.

The war's impact on global growth forecasts has been significant, with the OECD and other institutions revising projections downward. China's relative resilience so far stands in contrast to economies like the United Kingdom, which faces a much larger hit from energy disruptions.

Key Economic Indicators at a Glance

| Indicator | Q1 / March 2026 | Prior Period | Direction |

|---|---|---|---|

| GDP (YoY) | 5.0% | 4.6% (Q4 2025) | Accelerating |

| Industrial Output (Mar) | +5.7% | Forecast: lower | Above expectations |

| Retail Sales (Mar) | +1.7% | +2.8% (Jan-Feb) | Decelerating |

| Exports (Q1) | +15.0% | Strong | Surging |

| Urban Unemployment | 5.4% | Lower | Rising (1-year high) |

| Property Investment | -11.2% | Declining | Deep contraction |

| High-Tech Output (Q1) | +12.5% | Outperforming | Accelerating |

| Producer Prices (Mar) | Positive | 3.5 years deflation | Turning |

A Lopsided Recovery Complicates the Policy Outlook

The divergence between strong supply-side metrics and weak demand-side indicators presents a complicated picture for Beijing's policymakers. The GDP target was already lowered to a range of 4.5% to 5% for 2026, the lowest since 1991, signaling that the leadership adopted a more flexible approach toward growth. The better-than-expected Q1 print will likely reduce the urgency for sweeping new stimulus measures.

NBS deputy commissioner Mao acknowledged the tension directly. "Overall, the main macro indicators rebounded in the first quarter, and new drivers are growing rapidly," he said at a press briefing in Beijing. "But we also need to see that the external situation is more complex and volatile, and the imbalance between strong domestic supply and weak demand is still stark."

The Communist Party's ruling Politburo is set to hold a meeting focused on the economy at the end of April, where it will provide direction on future policies. Most economists expect targeted rather than broad-based intervention.

"We expect the policymakers to focus on implementing existing policy easing measures. They will likely introduce targeted fiscal support and relief measures to manage the energy price shocks and alleviate cost pressures."Xiaojia Zhi, Economist, Credit Agricole CIB

Zhi also noted that the Iran conflict will reinforce China's determination to strengthen national security, which could accelerate public spending on strategic investment projects while cushioning near-term growth pressures if external demand deteriorates.

Central Bank Holds Fire as Inflation Expectations Shift

A rising number of economists now forecasts that the PBOC will not cut interest rates in 2026, as the oil shock has pushed up inflation expectations. That represents a significant shift from earlier in the year, when rate cuts were widely anticipated as part of Beijing's effort to stimulate the economy.

Bloomberg Economics still predicts the PBOC will loosen policy this quarter, but through the reserve requirement ratio rather than benchmark rates. The firm expects a 25-basis-point RRR cut, followed by additional fiscal stimulus from the government later in the year, in an effort to maintain China's easing stance without stoking inflation further.

The policy options under discussion include:

- RRR cuts to inject liquidity without lowering headline rates

- Targeted fiscal support for energy-affected sectors and small businesses

- Accelerated infrastructure spending on national security and strategic projects

- Extended trade-in subsidies for consumer durables (though the car program has already been scaled back)

- Property market stabilization measures to arrest the ongoing investment decline

"Weak labor demand is weighing on consumption. The momentum remains manufacturing-driven. Given the Middle East conflict and potential disruption to energy supply, we see the downside risk to growth."Raymond Yeung, Chief Economist for Greater China, ANZ

Global Context: China's Divergence From Western Economies

China's Q1 performance stands out against a global backdrop of economic uncertainty driven by the Iran war. While Goldman Sachs has raised recession odds for Western economies and the OECD has slashed growth forecasts across advanced nations, China's export-driven model has proved more resistant to the initial energy shock.

That resilience, however, comes with significant caveats. The economy's dependence on manufacturing exports makes it vulnerable to any deterioration in global demand, which could materialize if the war continues and oil prices remain elevated. The International Monetary Fund, speaking at the same spring meetings where ECB officials discussed their own challenges, has warned that prolonged supply disruptions from the Strait of Hormuz could trigger a synchronized global slowdown.

For global markets, the China data provided a positive signal on . Asian equities rallied, with the Nikkei 225 jumping 2.4% and the Kospi climbing 2%, partly on the back of China's stronger-than-expected GDP print and renewed hopes for an extended ceasefire between the U.S. and Iran.

What to Watch in Q2 and Beyond

The critical question is whether China can sustain this pace while rebalancing toward domestic consumption. The Politburo meeting at the end of April will offer the first real indication of how leadership plans to address the supply-demand imbalance. Key data points to watch in the coming months include:

- April retail sales and consumer confidence surveys for signs of stabilization

- The scope and scale of any new fiscal measures announced after the Politburo meeting

- Oil import volumes and refinery utilization rates as Iran war dynamics evolve

- Private investment trends, which will signal whether business confidence is recovering

- The PBOC's next move on the reserve requirement ratio

The 5% headline is a number Beijing will welcome. But inside the NBS briefing room, the phrase Mao Shengyong kept returning to was "imbalance." Until consumer spending and private investment show genuine signs of life, China's recovery will remain a one-engine airplane, flying fast but structurally fragile. Whether that engine holds through the turbulence of the Iran war and elevated energy costs will define the economic story of 2026.